Sign up for a free subscription at larrykotlikoff.substack.com. I’ll immediately make it a free lifetime subscription. Also, pls sign up kids, parents, sibs, friends, colleagues, students, … !

Paid subscriptions come with a one-hour, free financial consultation with me. Email me a time at kotlikoff@gmail.com. After our session, unsubscribe and resubscribe for free.

Teaching Financial Literacy/Economics in High School, College, or Grad School? Contact me at kotlikoff@gmail.com for free MaxiFi licenses for your students and a PRO license for you.

If you’ve been watching/listening to my podcasts, you’re familiar with Fred Lane, Founder, CEO, and CIO of Lane Generational. Fred’s a storied investor and frequent Economics Matters podcast guest. His last appearance was in October.

Fred’s brilliant partner, Jack Schibli is the COO and Director of Investment Strategy & Research at Lane Generational and a terrific economist. Jack just posted a long newsletter, entitled Q1’26: The Illiquid Jenga Tower. I provide a summary below.

Full disclosure: I invest with Fred and Jack. But I’m not a financial advisor and I don’t recommend any investments of any kind, including Lane Generational, to anyone. Nor do I have any commercial relationship with Lane Generational apart from being an investor. Lane Generational is an SEC Registered Investment Advisor. The firm manages money on an active basis for investors seeking to grow and protect purchasing power through market cycles. Click here for their terrific free blog.

Jack’s blog involves the highly opaque and, increasingly troubled, private equity and private credit sectors. Jack, as you’ll read, is concerned with the life insurance industry’s heavy investment in these securities and the potential for losses in these sectors to bankrupt some/many/most life companies.

Why should you care? Your life insurance company may be one of those that fail. If so, the problems in the private equity and private credit sectors will land in your lap. To be concrete, suppose you have, say, a $3 million life insurance policy to protect your spouse and kids and you drop dead at the same time your insurance company drops dead. Your heirs will likely end up with just $250K to $500K, assuming state insurance commissions, which have de minimis reserves, come across to their pledged extent.

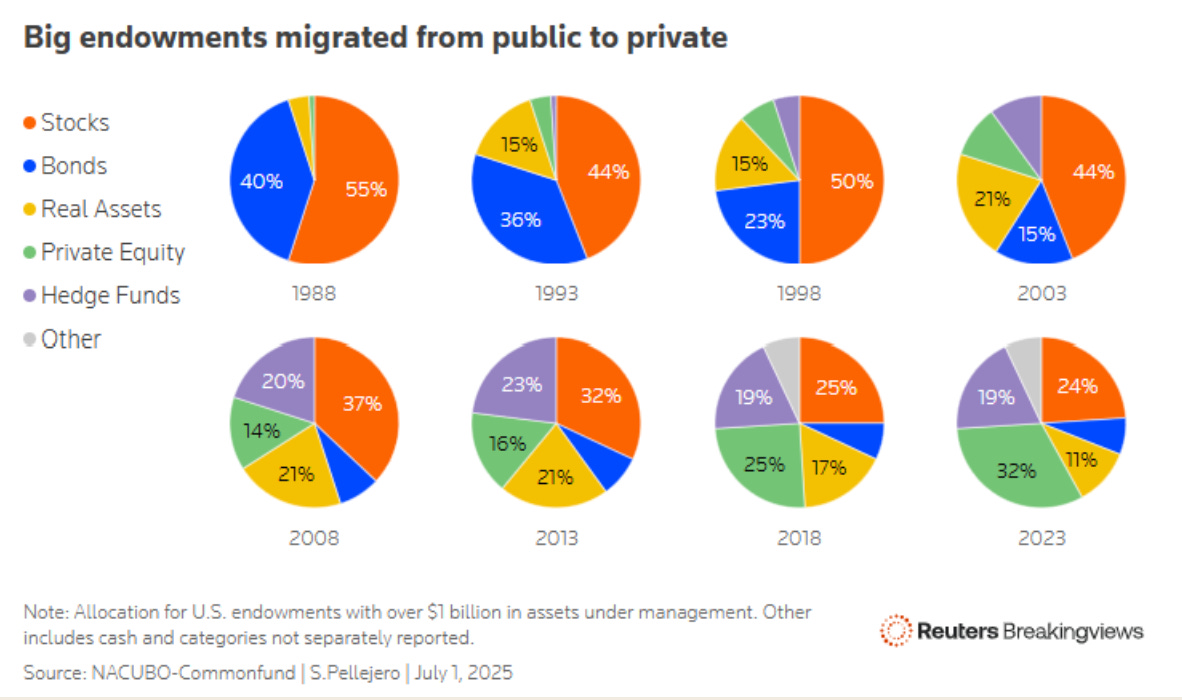

Jack starts with the multi‑decade shift of pension funds, university and other non-profit endowments, and, recently, life insurers into non-traditional investments — private equity, hedge funds, real estate, and, of late, private credit. Take endowments. An astonishing three-fifths of their investments now comprise holdings of opaque private equity, real assets, and hedge funds. In 1988, this share was less than 5 percent, with 95 percent invested in publicly traded stocks and bonds — securities subject to second-by-second market valuation and public, if far from perfect, disclosure.

This shift was inspired by the strategy of fabled Yale University investor David Swensen. Swensen focused on capturing the illiquidity premium from investing in illiquid assets. He earned a roughly 3 percentage-point above-market return between 1985 and 2001. Swensen might just have been lucky, but his strongly-titled book, “Pioneering Portfolio Management,” convinced his peers to follow en masse.

From the perspective of finance, finding new assets that aren’t, like Crypto, arguably dominated, is a bonanza — a path to higher returns with the same risk. But that presumes one knows the risk of the “newly” discovered assets. Jack stresses that the risk of these equity-like-return-producing assets has been artificially under-measured. Their performance is revalued on a quarterly, not a continuous, trading-market basis, and security values are rarely properly marked down (declared to have fallen) in real time. This produces seemingly smooth returns when such “smoothness” is the product of accounting, not actual market purchases and sales. The “accountants” here are investment managers and for-hire “independent” appraisers who use highly manipulable performance measures, specifically adjusted‑EBITDA, as well as net asset value (NAV) appraisals based on cherry-picked price-to-earnings multiples — multiples that have exploded over the past decade.

Jack references S&P research showing that the private equity sector’s EBITDA add‑backs (special adjustments that raise EBITDA) account for more than half of reported EBITDA. This lowers reported leverage ratios and raises reported, i.e., estimated enterprise values. When underlying public market multiples fall—particularly in software and other growth sectors—private equity managers face a stark choice: crystallize much lower values through genuine exits or maintain inflated marks (valuations of their private equity fund assets) using devices like continuation funds, which mostly move assets from one pool of limited partners to another at or near stated net asset value.

To understand continuation funds, suppose persons A and B hold assets worth X that they report are worth Y, where Y is far higher than X. A can sell his/her assets to B and B can sell his/her assets to A — both at price Y. This allows A and B to report, indeed prove, based on market transactions, that their assets are worth Y when they are only worth X.

Jack calls the industry’s valuation practices a “Jenga tower,” built to collapse based on specious modeling assumptions and intra‑industry transactions.

How did private, as in undisclosed and arbitrarily valued, IOUs grow to today’s $2 trillion market total? Here’s Jack’s description:

The typical leveraged buyout (LBO) model deployed by private equity is to purchase a company using a significant portion of debt, often 50-70%, backed by the target company’s assets, then cut costs, increase cash flow to pay down debt, and attempt to sell at a higher multiple. Arguably, the largest driver of success in this model is a declining interest rate environment, as debt used can be financed at cheaper rates, and lower rates also push up exit multiples. The era of declining interest rates ended in 2022, and since then, private equity has struggled, uncovering many fundamental issues masked by low rates.

Historically, private equity would source the debt used in an LBO from a traditional bank, but post-2008 reforms like Dodd-Frank and Basel III regulated banks into maintaining higher capital ratios, making it less profitable to hold these types of leveraged loans on their books. Financing activity then shifted to non-banks, including broadly syndicated loans (BSL – investment banks underwrite and sell to institutions), collateralized loan obligations (CLOs – bundling hundreds of individual loans into a single vehicle), and early direct lending funds (e.g. Ares, Blue Owl).

However, with the immense scale of capital flowing into private equity, lending grew commensurately, to the point that large private equity firms (e.g., Apollo, KKR, Blackstone) decided to open their own private credit arms to fund their investments. The same companies are now managing the debt and the equity, collecting fees on both, and heavily influencing valuation marks.

Let’s pause on the above paragraph. If I’m running a private equity fund and realize its assets aren’t what I claim, borrowing to stay afloat by issuing an IOU that’s backed by those self-same overvalued assets is engaging in fraud squared. And if my lenders realize my assets aren’t worth what I’m claiming, they will pull their loans forcing me to sell my assets in a rush, leading to very low market valuation.

There are now huge PE funds serving as both the borrower and the lender in many of the same deals. According to Jack, “81% of private credit managers also manage private equity funds.” Of course, traditional banks borrow money, including in the form of demand deposits, which they invest in assets, including equities. The difference here is that the banks are regulated and restricted with respect to the extent of private equity investment. Thus a far higher share of their equity investments are publicly traded.

As Jack relates, to keep private equity deals flowing, borrowers are using payment‑in‑kind (PIK) features, letting them pay interest by issuing more debt rather than paying what’s owed. This is the equivalent of not paying off your credit card bill. The interest you don’t pay increases your credit card balance. These PIK loans now comprise over 6 percent of private credit borrowing. This, in Jack’s (and my) view, is evidence of the private credit sector having a 6 percent higher-than-reported default rate.

When added to the historical annual default rate of ~2.5%, PIK pressure could signal default rates in the 9% range ahead. Investing in credit differs significantly from investing in equity. While the equity model is predicated on picking winners, which typically more than offset losers, the credit model is based on avoiding losers due to the fixed nature of returns. Let’s say private credit annual returns are in the 10% range – this is directly tied to the interest rates lenders are receiving on loans. If the annual default rate is 6%, there goes 60% of the annual return. You might as well buy the 10-year note at ~4.25%.

AI is the back story to much of the private credit sector’s current woes. Private credit funds have disproportionately lent to software companies, some/many/most? face existential threats from AI. Almost one in five dollars of private credit assets are loans to software companies. And many/most of those software companies are both private and heavily leveraged.

Recent high‑profile bankruptcies, particularly First Brands and Tricolor, as well as BlackRock’s overnight markdown of a private credit from full to zero value suggest that “model‑based” NAVs can be wildly out of sync with underlying market realities. Layer on private credit fund leverage and quarterly redemption gates, and you have Jack’s forecast — slow, but steady investor withdrawals from private credit funds. This will lead private credit funds to sell, over time, their best assets (IOUs) first, steadily degrading the portfolio quality of their remaining assets (IOUs). Recent data show record-breaking redemption requests by private credit investors. And publicly traded private credit companies have, of late, lost almost three-quarters of their market cap.

The most troubling link in the chain, according to Jack, is the life insurance sector. Leading private equity firms explicitly moved into life insurance to secure “permanent capital,” acquiring or launching carriers, such as Apollo’s Athene, and steering their general accounts — the reserves available to, for example, make good on your life insurance policy — toward private credit and other alternatives. Moody’s estimates that roughly one‑third of US life insurers’ $6 trillion in assets are now parked in private credit, including over $200 billion in loans collateralized by inflated private equity holdings.

To boost reported capital ratios, many PE‑owned insurers rely on offshore reinsurance in lightly regulated jurisdictions like Bermuda and the Cayman Islands. Jack’s blog notes that 60 percent of nearly $1 trillion in reinsurance purchased in 2024 came from offshore entities, many of them captives ultimately controlled by the same insurer, meaning little real risk transfer. Ratings agencies have often gone along, assigning rating grades several notches higher than those of the National Association of Insurance Commissioners. This overrating limits the amount of required capital (low-return but safe assets) private credit investing insurance companies need to hold, i.e., it lets them engage in great risk taking.

PHL Variable Insurance Co.’s collapse offers a concrete case study: an initially reported $135 million capital deficit was later revised to a more than $2 billion shortfall once captive reinsurance and overly optimistic asset valuations were scrutinized. Because state guaranty funds typically cap protection between $250,000 and $500,000 per policyholder, many retirees face the prospect of substantial uncompensated losses in such failures. Grant’s reporting on KKR‑controlled First Allmerica, cited in the memo, shows an insurer with surplus so thin that a less than 1 percent loss on assets would wipe out its capital, even as it reinsures tens of billions for other household‑name carriers. That interlinked reinsurance web is precisely the sort of hidden network that can turn a single failure into cascading insolvencies.

The life insurance industry issues both term and permanent (whole life, universal life, indexed UL, variable life) policies. The latter combine saving and term insurance, i.e., your premium partly goes to protecting your heirs if you kick prematurely and partly to saving money. But unlike saving money in a bank or mutual fund, your savings inside your permanent life insurance policy, called your cash value, isn’t FDIC-insured and can’t necessarily be withdrawn quickly without a penalty. Jack’s example is losing 10 percent as the price of cashing out your policy.

Here’s Jack’s question:

Would you rather pay a 10 percent early withdrawal fee on a $5 million policy and receive $4.5 million, or receive $250,000 to $500,000 if your insurer goes under? If PHL* is the canary in the coal mine, then this is the math policyholders will be considering if a panic ensues. A wave of early redemptions would force insurers to liquidate assets and likely put on full display many of the issues we’ve discussed, from the overstatement of private fund NAVs to captive offshore reinsurance. This is a box of tinder awaiting a match, and a “run on the bank” in a $6 trillion industry is certainly of the size and scale to be systemic.

*PHL references private-equity-owned insurer PHL Variable Insurance Co. It posted a $135 million capital deficit in 2023, but Connecticut regulators found it was really short over $2 billion. It failed and left its policyholders with a $120 million loss of cash value and a $300K limit on payouts to those of its policyholders who died or will die.

A cash value run associated with a rising number of publicly announced life insurance company failures could be our next Great Financial Crisis, if not Great Recession. If a third of the life insurance industry’s $6 trillion in assets are in private credit and private credit continues to tank, how will it cover its estimated, up to $5 trillion, in outstanding cash value if there is a run on the life insurance industry’s shadowy banking system?

All this said, your particular insurance company may not invest or may invest very little in either private credit or private equity. But if you are holding permanent insurance with substantial cash value, check out how your insurer has invested your money. If it’s in private credit/equity, maybe it’s time to cash out, invest on your own, and purchase term insurance from a company that will be there when you won’t.