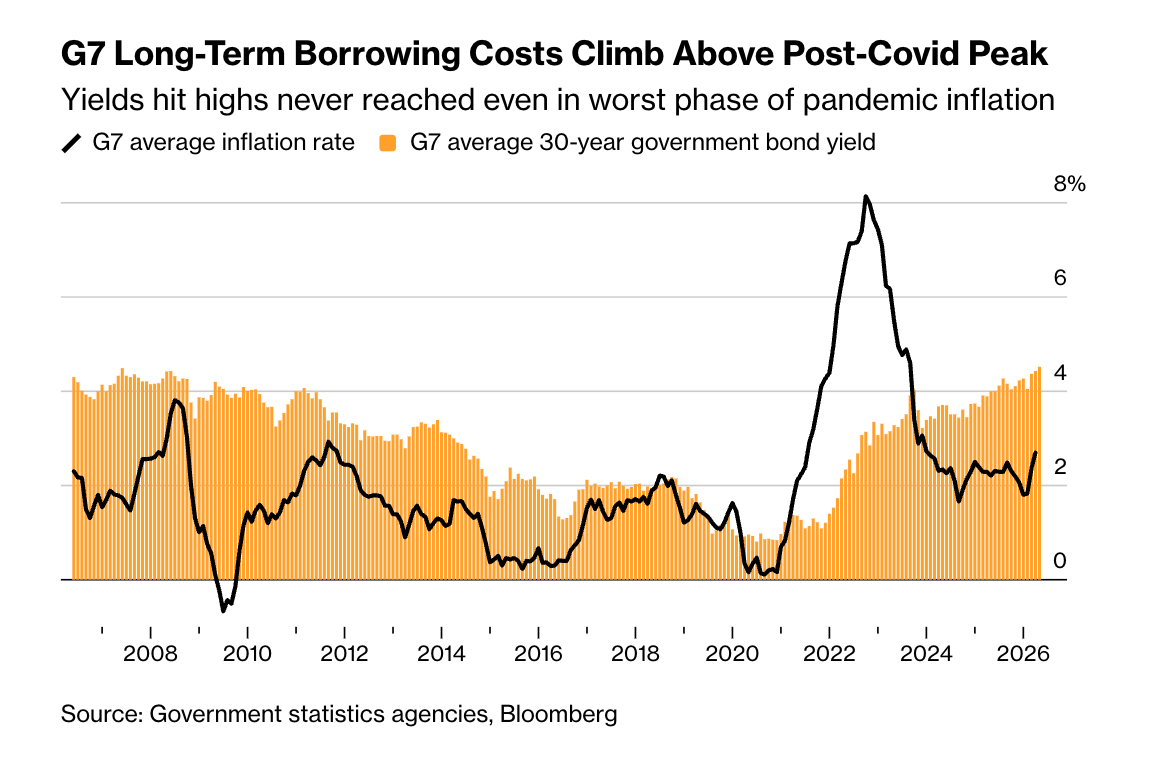

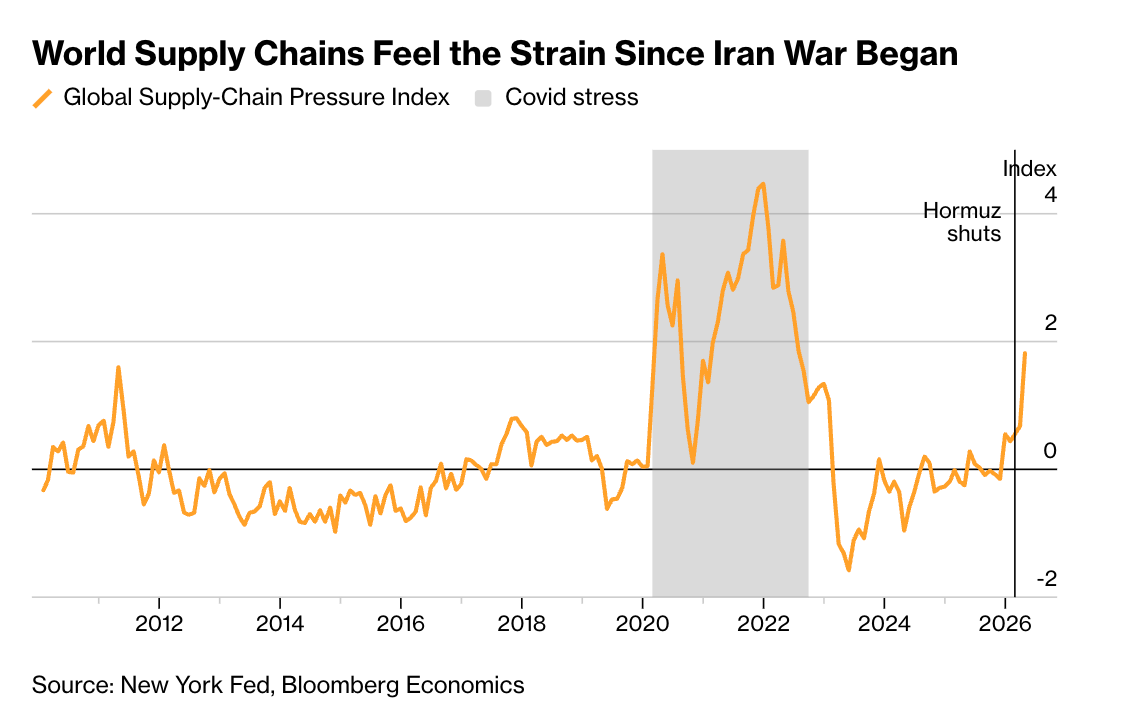

One inflation spike in the 2020s might be an accident, the world’s biggest bond markets seem to have decided, but two looks like an alarming new trend. The US war on Iran is inflicting another wave of price hikes on a global economy that’s barely recovered from the last one. A material chunk of the world’s fuel and fertilizers is trapped inside the Strait of Hormuz, and the pain is spreading. European airlines canceled flights, Americans have spent an extra $20 billion at the gas pump, and Asian rice farmers wondered if they should skip planting. Pretty much every pundit reckons things will get worse before they get better. As all this damage mounts, it’s starting to rattle the safest haven in world finance: the $50 trillion-plus market for Group of Seven sovereign bonds, where long-term yields hit a two-decade high this week. Put simply, investors are starting to worry, like they never quite did even at the post-Covid peak, that higher inflation is here to stay. They want compensation for that risk, and expect central banks will have to raise interest rates to contain it.

Despite the worries, so far, inflation expectations seem to have remained anchored.

But this kind of measure of inflation expectations is anything but fool proof. See Stuart Kirk, also in the FT:

Using implied yields or the swap market will not give you a pure reading for inflation expectations because these are traded asset prices — with all that entails. So into the mix goes supply and demand, technicals, liquidity conditions, and other distortions such as quantitative easing. It’s the same reason why oil futures aren’t an indication of future oil prices. Thus five-year, five-year data has limited predictive power over such long time horizons, a European Central Bank paper concluded. And even over one and two years, surveys are just as accurate. At best the metric hints at how good a job policymakers are doing in anchoring expectations. Nothing more. … The long list of complex factors that influence bond prices is also why inflation-linked bonds are not a substitute for measuring real yields. Conflating the two is the fifth misconception that drives me potty. This one is particularly harmful as real yields are the one true economy-wide indicator of the cost of borrowing and lending. They have nothing to do with pension fund demand, liability matching, liquidity and inflation-risk premia and all other stuff that goes into the pricing of Treasury Inflation-Protected Securities or Linkers.

“You just have this series of never-ending supply shocks, and these big structural changes in the global economy, and that’s going to create a lot of inflation volatility,” says Dario Perkins, managing director at TS Lombard. With 2% targets starting to look more floor than ceiling, “my guess is we’re entering a different phase of the monetary cycle,” he says. “It’ll be rate hikes everywhere.” … “I expect the next decade or so to be structurally more inflation-prone and to raise the toughest challenges for central banks in decades,” says Claudio Borio, former head of the monetary and economic department at the Bank for International Settlements.

THANK YOU for opening the Chartbook email. I hope it brightens your day.

I enjoy putting out the newsletter, but tbh, what keeps this flow going is the generosity of those readers who clicked the subscription button.

If you are persuaded to click, please consider the annual subscription of $50. It is both better value for you and a much better deal for me, as it involves only one credit card charge. Why feed the payments companies if we don’t have to.

America’s ‘simultaneity’ nightmare Patrick Foulis

Is there any coherent explanation for the Trump administration’s embrace of Xi Jinping, decapitation of Venezuela’s regime, indulgence of Vladimir Putin, ceasefire with the Houthis and half-finished war with Iran? Surprisingly, there is: America’s simultaneity problem. This is the threat of concurrent attacks by multiple adversaries that overwhelm the superpower. It is not a Trumpian concoction. Until 2012, the Pentagon maintained a “two war” standard of being able to win two major wars at the same time. Team Biden feared that the abandonment of this, and the rise of an axis of autocracies, had created a generational crisis for US security. If they exploded concurrently, another Middle East emergency, a Chinese escalation in the Taiwan Strait and a Kremlin incursion into Nato would push the US military to breaking point. The autocracies could also collude over nuclear threats, destabilising 80 years of deterrence. By 2035 China, Russia and North Korea are together expected to have twice as many deployed warheads as the US. All have missiles that can reach America.

The Biden administration’s response was to try to rally weak allies into an anti-autocratic coalition. The Trump team believes this was luxury thinking and there is a better answer: pre-emptive attacks to sequence inevitable wars or to degrade enemies, and diplomacy to split up the other axis powers. That buys time for the US to re-arm. While this is a traumatic break with the ideals of a liberal, globalised world, the playbook is not new. America has fought precautionary or pre-emptive wars before, including the invasions of Panama in 1989 and Iraq in 2003. Nixon embraced Mao Zedong in 1972 to try to deepen the Sino-Soviet divide. Now US secretary of state Marco Rubio says the post-1945 security order is obsolete, and hails the use of pre-emption against Iran. Elbridge Colby, the Pentagon’s strategist, argues policy is “designed precisely” to avoid concurrent wars.

For eighteenth century America to build its economy, it needed skilled workers able to assemble machines acquired overseas (by whatever means). The young United States began as a “pirate nation,” getting hold illicitly of European technology to fuel its Industrial Revolution. Lacking a manufacturing base, America relied on theft. The nation’s first Treasury Secretary Alexander Hamilton aimed at jump-starting industrialization and advocated a system that would reward those who brought “secrets of extraordinary value” into the country. The acquisition of technology was essential for transforming the United States from an agrarian economy into a manufacturing power. In 1791, he set out his strategy to Congress in the seminal “Report on Manufactures.” Hamilton argued that procuring European machinery was vital to the American economy. With Britain as a prime target, he and his assistant Tench Coxe encouraged state-sponsored theft of trade secrets, blueprints, and industrial tools, as well as recruiting mechanics. They supported individuals who engaged in these actions.

Marylander Thomas Digges was an illicit agent encouraging English and Irish textile workers to emigrate to the United States. George Washington praised him for his efforts to send “artisans and machines of public utility” to America. Federal patents were granted to individuals for technological inventions pirated from abroad. The upstart country was a den of piracy, a rogue nation.

The British government introduced restrictions on the export of technology and limit the migration of innovators or skilled workers. Foreign head-hunters were threatened with a year in prison for every Brit they recruited to work overseas, but the authorities proved unable to stop the flow of skills. The brain drain had started long before invention of the term. The creative mind is not and will never be state-owned. The most telling case of a British entrepreneurial exodus was that of Samuel Slater (1768-1835), the “Father of the American Industrial Revolution.”

Slater the Traitor: Although cotton was grown in the United States, the country had no domestic textile manufacturing industry. The technology was British and remained closely guarded. In 1733, Lancashire-born John Kay had patented the “flying shuttle,” allowing a single weaver to work at much higher speeds. Half a century later (1785), Nottinghamshire-born Edmund Cartwright invented the mechanical “power loom,” moving production from homes to factories. Skilled workers and tool makers stood in the vanguard of the Industrial Revolution. They were forbidden to leave the country.

Samuel Slater was born on June 9, 1768, in Belper, Derbyshire, into a farming family. Aged ten, he began work at a local cotton mill recently opened by Jedediah Strutt, using the water frame pioneered by Richard Arkwright. By the age of twenty-one, he had gained a thorough knowledge of the cotton spinning process. He embodied skills the British government wanted to hold onto, but Slater learned of American interest in developing similar machines and was tempted by the generous financial rewards on offer. He was also aware of the legal ban on exporting designs and blueprints. He memorized all vital details of Arkwright’s operation, before leaving for the city of New York in 1789. Having secured the backing of Rhode Island merchant Moses Brown, he constructed America’s first water-powered cotton spinning mill in 1790. Three years later, Slater and Brown opened their first textile factory at Pawtucket, Providence County.

Domestic textile manufacture grew rapidly, becoming America’s most important pre-Civil War industry. Cotton production became a central part of the nation’s early economy. It marked the beginning of a manufacturing boom for New England. Slater eventually owned thirteen spinning mills, developing settlements of working families around them (child labor at the mills was a standard practice). One of these towns was Slatersville, Rhode Island. In Derbyshire people named him “Slater the Traitor,” as textile workers considered his move a betrayal that threatened their mills and livelihoods. Slater’s extraordinary power of recollection was equaled by the Massachusetts industrialist Francis Cabot Lowell who, in 1812, toured England and Scotland. Visiting various textile mills, he closely observed their design and operations. On his return journey, Lowell’s ship was searched by British customs officers on suspicion that he was in possession of industrial designs. They found nothing as Lowell had memorized the blueprints of Cartwright’s power loom. He built the first integrated textile mill in Massachusetts.

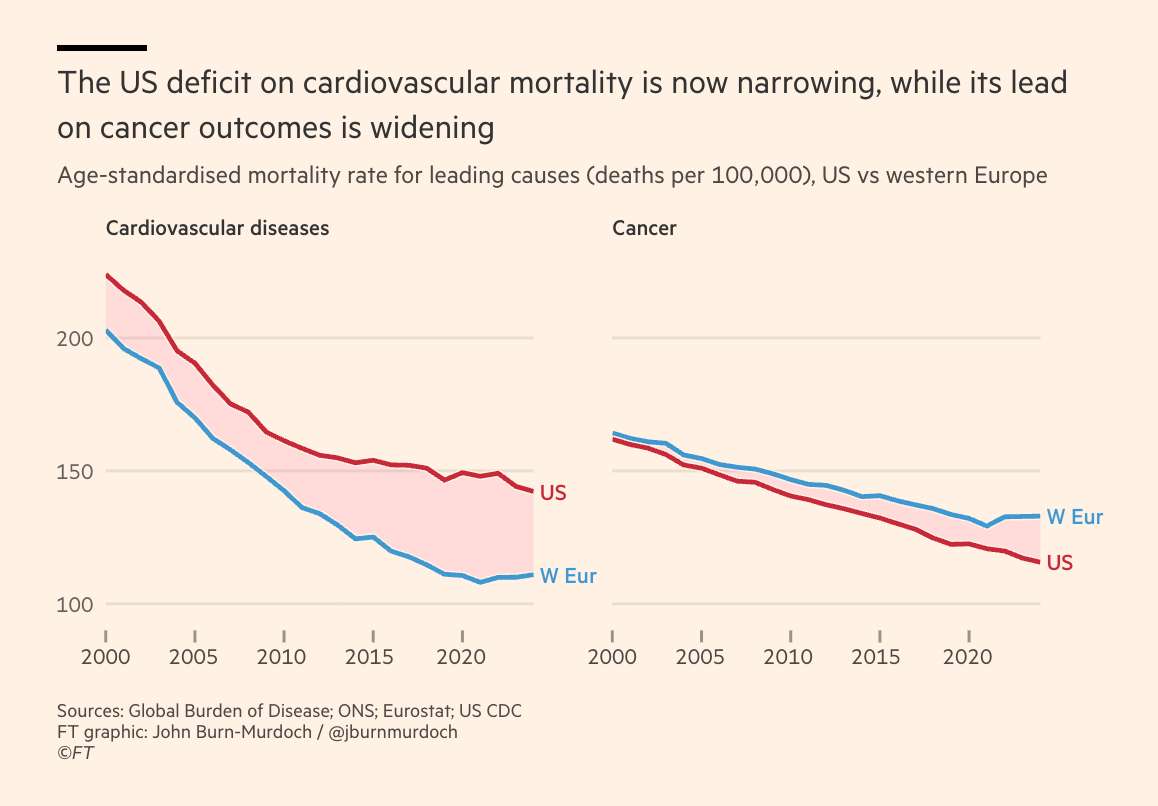

Why America’s health stats ARE improving. (John Burn-Murdoch)

On health, a big part of the story is cancer, where US mortality rates are lower than those in western Europe and also falling faster. Discussions about the merits and performance of US and European healthcare systems often gloss over the fact that poor American outcomes are concentrated in the conditions most related to unhealthy lifestyles such as cardiovascular disease and diabetes.

But diseases like cancer afflict a wide range of people regardless of behaviour, making death rates a more direct reflection of outcomes in the healthcare system. On this score Americans’ above-average healthcare spending comes with above-average success. What is more, as high US uptake of GLP-1 weight-loss drugs begins to reduce obesity-related disease, it’s possible the US will see further catch-up.

This training film about the JU88’s machine guns is fascinating. Shows how in the Junkers design light machine guns were effectively “added” to the aircraft.

")