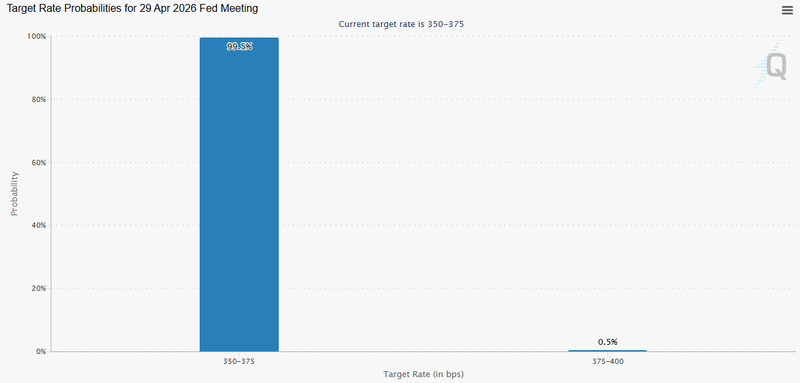

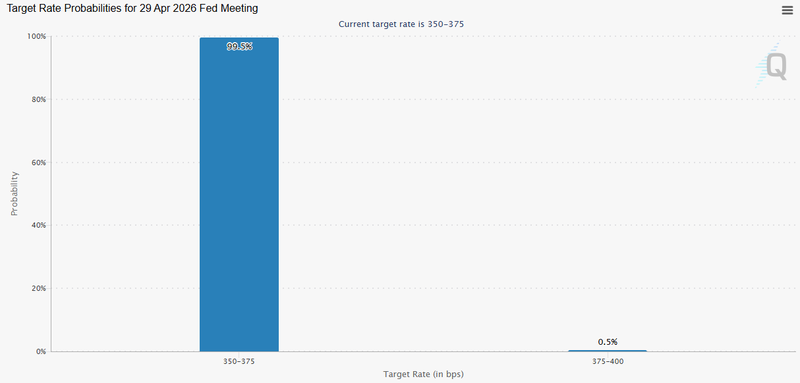

Fed pricing is now the main pressure

The biggest problem for gold is the change in rate expectations.

Gold does not pay income. That becomes a real disadvantage when investors believe interest rates may move higher again. If the market sees a possible Fed hike in September, Treasury yields become more attractive and the dollar usually strengthens. For gold, that creates pressure from both sides.

This is not only about the headline interest rate

The real issue is real yields. When inflation-adjusted yields rise, investors are paid more to hold government bonds instead of a metal that pays nothing. That changes the calculation for portfolio managers. They may still believe in gold as protection, but they now have to justify holding it against cash and bonds that offer better income.

Market pricing has already shifted, with traders assigning roughly a 34% chance of a July hike and around a 50% chance of a September move. Those probabilities can move quickly, especially with today’s PCE inflation data in focus.

That matters because Kevin Warsh has made this Fed cycle more data-dependent. He has not given markets clear guidance on the next decision. Instead, he has left the policy path tied to incoming numbers. So traders are not only listening to Fed speeches. They are using each inflation report to decide how much tightening risk should be priced.

A soft PCE reading could ease some of the pressure on gold by pulling rate-hike expectations lower. A hot reading would do the opposite. It would strengthen the case for another Fed move, keep real yields supported and leave gold struggling to attract fresh buying.

Source: CME Group

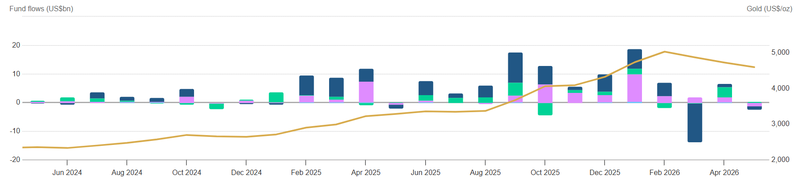

ETF outflows show confidence has weakened

The ETF flow picture confirms that investors are becoming more cautious.

Gold-backed ETFs have seen around $1.1 billion in outflows, with North America leading the selling. That matters because ETFs are often the easiest way for institutional and long-only investors to adjust gold exposure. They do not need to move physical metal. They can cut exposure quickly through liquid listed products.

This is an important signal

The selling is not only coming from futures traders or short-term speculators. Some investors who normally use gold as a portfolio hedge are also stepping back. They are not necessarily abandoning the asset, but they are less willing to add exposure while real yields are rising and the dollar is firm. ETF outflows do not break the gold story on their own.

But they show that the support from investment demand is weaker at the exact moment when macro pressure is stronger. That combination makes the market more fragile.

Source: World Gold Council

Equity losses are turning gold into cash

The second pressure is not about gold itself. It is about balance-sheet stress.

The sell-off in AI and semiconductor shares has hit some of the most crowded positions in the market. These were trades built on strong momentum, heavy institutional exposure and high confidence in the earnings story. When those positions start falling quickly, the problem is no longer only the loss. The problem is what those losses do to leverage, margin requirements and portfolio risk limits.

That is where gold comes in. Institutional desks do not always sell what they dislike. In a liquidity squeeze, they sell what can be turned into cash quickly and efficiently. Gold futures and other liquid gold contracts sit near the top of that list. They are deep enough, liquid enough and widely held enough to be used as a funding valve when losses elsewhere need to be covered.

So the current gold selling should not be read only as a negative view on bullion.

Part of it is forced balance-sheet management. If equity books are under pressure, gold can be sold to reduce leverage, meet margin calls or avoid deeper cuts in less liquid positions. That kind of selling is different from normal profit-taking because it is not always price-sensitive. The desk does not wait for the perfect level. It sells because cash is needed.

This is what makes the current move more dangerous than a simple correction.

The macro story is already working against gold through higher real yields and a stronger dollar. Then the equity sell-off adds a second layer by turning gold into a source of liquidity. Once that happens, gold stops trading only on its own fundamentals and starts reacting to stress in another part of the portfolio.

Why the sell-off can overshoot

When macro pressure and forced selling happen together, gold can fall faster than fundamentals alone would suggest.

A stronger dollar reduces international demand. Higher real yields reduce the appeal of non-yielding assets. ETF outflows remove one source of investment support. Margin-driven selling adds another layer of pressure because it is not always price-sensitive. Desks that need liquidity do not wait for a perfect level.

They sell what they can. That is how a market can move from orderly profit-taking to aggressive liquidation.

The danger is that technical breaks can then accelerate the move. Once gold falls through key levels, systematic funds and momentum traders may add to the pressure, even if central banks and long-term buyers remain supportive underneath.