VioletaStoimenova

The pay-out metrics of commercial real estate investment trust Starwood Property Trust Inc. (NYSE:STWD) weakened in the second quarter, but the trust still managed to cover its $0.48 per share per quarter dividend with distributable earnings in 2Q24.

Starwood Property Trust is well-diversified and has relatively low exposure to U.S. offices, which are two key strengths that I see for the company that its peers don’t have.

Furthermore, the central bank is poised to lower interest rates, which could take pressure off of the challenged U.S. office sector in the latter half of the year.

I think that Starwood Property Trust continues to make a strong value proposition for passive income investors, and I consider the 9% yield to still be worth buying.

My Rating History

Starwood Property Trust’s diversified investment platform and well-covered 9% dividend yielded a stock classification of Buy in the second quarter.

With the central bank seemingly on the brink of cutting short-term interest rates in September for the first time this interest rate cycle, I think the commercial real estate market could see less duress and potentially stronger originations, particularly if a U.S. recession is avoided.

Though Starwood Property Trust’s dividend pay-out ratio rose in 2Q24, I think the dividend will ultimately prove to be sustainable.

Portfolio Review And Core Segments

Only 12% of Starwood Property Trust’s total assets were invested in the office segment as of June 30, 2024. The trust is operating primarily in Lending (commercial, residential and infrastructure), but its portfolio includes other commercial real estate investments as well, mainly owned properties.

Lending assets accounted for 77% of the trust’s investments in 2Q24, and Starwood Property Trust owned a total of $26 billion in real estate investments.

Total Assets (Starwood Property Trust Inc.)

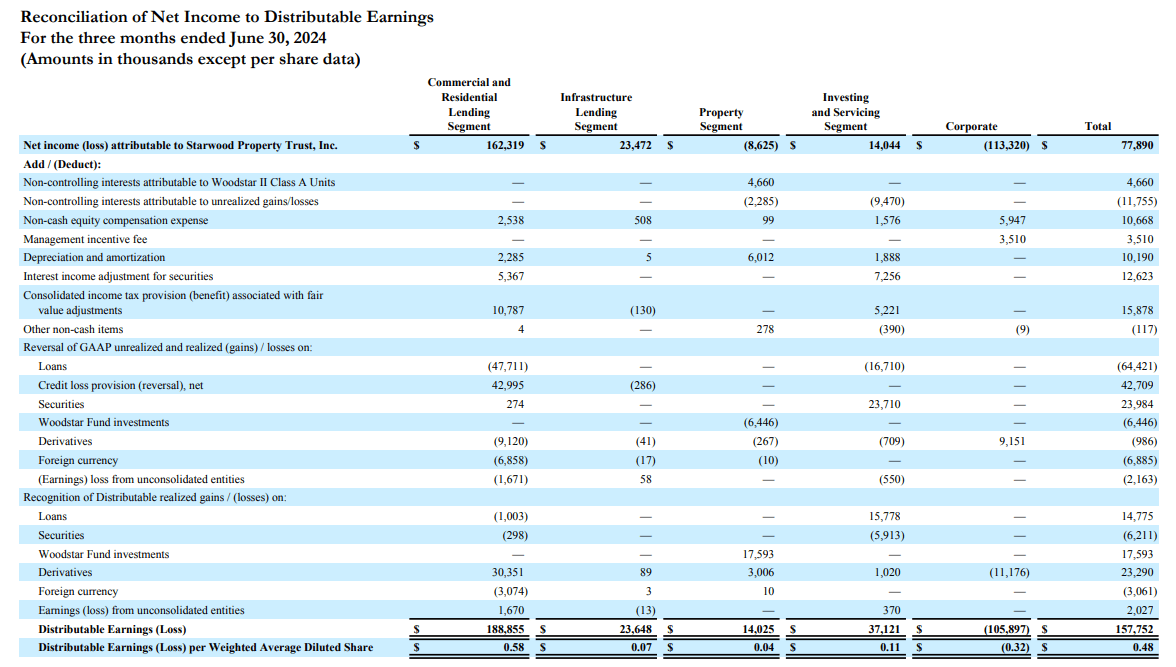

Starwood Property Trust produced lower distributable earnings in the second quarter as the commercial real estate investment trust reported higher credit loss provisions.

The trust’s credit provisions in 2Q24 totaled $43.0 million, compared to $35.0 million in 1Q24. This led to lower distributable earnings in 2Q24, yet Starwood Property Trust managed to fully cover its dividend with distributable earnings.

Reconcilitation Of Net Income To Distributable Earnings (Starwood Property Trust Inc.)

Though distributable earnings dropped to $0.48 per share in 2Q24, the commercial real estate portfolio is performing quite well, which is why I don’t anticipate a dividend cut.

The trust’s main Lending assets are First Mortgages, of which Starwood Property had $13.9 billion of as of June 30, 2024 and 97% were performing as they should.

Commercial Lending Metrics (Starwood Property Trust Inc.)

Dividend Metrics

Even though Starwood Property Trust’s dividend metrics deteriorated QoQ, the commercial mortgage real estate investment trust did not under-earn its dividend.

The trust paid out 100% of its distributable earnings in the second quarter, which was about 10 percentage points higher than on an LTM basis.

Though the dividend pay-out ratio has risen substantially in the last quarter, the trust declared two $0.48 per share per quarter dividends, probably in response to Blackstone Mortgage Trust Inc. (BXMT) adjusting its pay-out lately.

Dividend (Author Created Table Using Company Supplements)

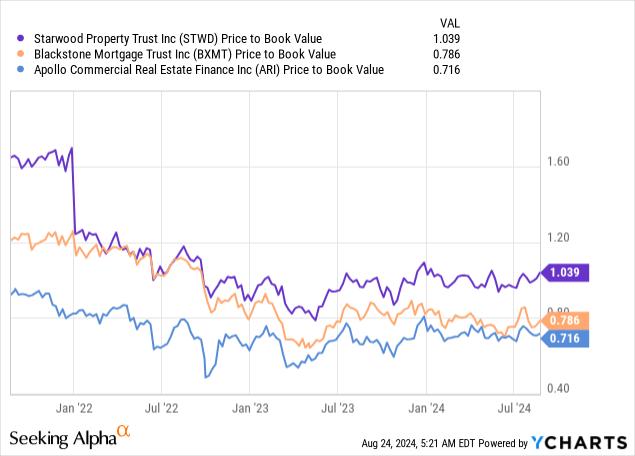

Premium Valuation

Passive income investors that desire to add Starwood Property Trust’s 9% yield to their portfolios have to pay 1.03x book value which sets the trust apart from its peers, some of whom are perceived to have weaker portfolios, less diversification or, in the case of Blackstone Mortgage Trust, just slashed their dividends.

Blackstone Mortgage Trust is selling for a 21% discount to book value after the trust reported a substantial increase in its dividend pay-out ratio and BXMT remains overweight offices (a total of 36% of collateral referred to offices, 26% of which to US offices).

Apollo Commercial Real Estate Finance Inc. (ARI) is selling for a 28% discount to book value and the trust just had its second straight quarter of a 100% pay-out ratio.

My intrinsic value estimate relates to the trust’s net book value which as of June 30, 2024 was $19.64 per share and which equaled the company’s book value minus accumulated depreciation.

Why Passive Income Investors Need To Be Careful

There have been a number of commercial mortgage real estate investment trusts that have slashed their dividends lately, with Blackstone Mortgage Trust particularly standing out. In this context, the rise in Starwood Property Trust’s dividend pay-out ratio is a potential concern, and it is not unreasonable to suspect that the trust could under-earn its dividend in the short-term.

With that being said, though, Starwood Property Trust has paid a $0.48 per share per quarter dividend since 2013 and the trust is more diversified than its peers in the commercial real estate market.

A dividend cut, should it happen, would drastically change the risk/reward relationship for Starwood Property Trust, in my view.

My Conclusion

There is still a lot to appreciate about Starwood Property Trust, including its relatively low exposure to U.S. offices and the trust’s strong position in commercial mortgages (leading to a high percentage of performing First Mortgages in the Lending segment).

The dividend pay-out ratio unfortunately rose to 100% in the second quarter, which means the trust’s margin of safety took a hit. Still, Starwood Property Trust covered its dividend fully with distributable earnings and the stock is only selling at a 3% premium to book value, which suggests that the market also doesn’t anticipate a dividend cut.

That STWD announced dividends until the end of the year was likely a response to prevent speculation about a short-term dividend cut after Blackstone Mortgage Trust slashed its pay-out by 24% last month.

I think the commercial real estate investment trust will do whatever it can to preserve its dividend record. Buy.