The two flawed assumptions that stood out to WGC analysts were: 1) the tendency to use data from the Gold Standard period to analyze gold’s performance, and 2) viewing long-term price dynamics exclusively through the lens of demand from financial markets and ignoring other sources of demand.

Based on such assumptions, many of the studies have landed on an expected long-run real return ranging between 0% and 1%. Alternative approaches using risk premia estimations or bond-like structures with embedded options also produced similar results.

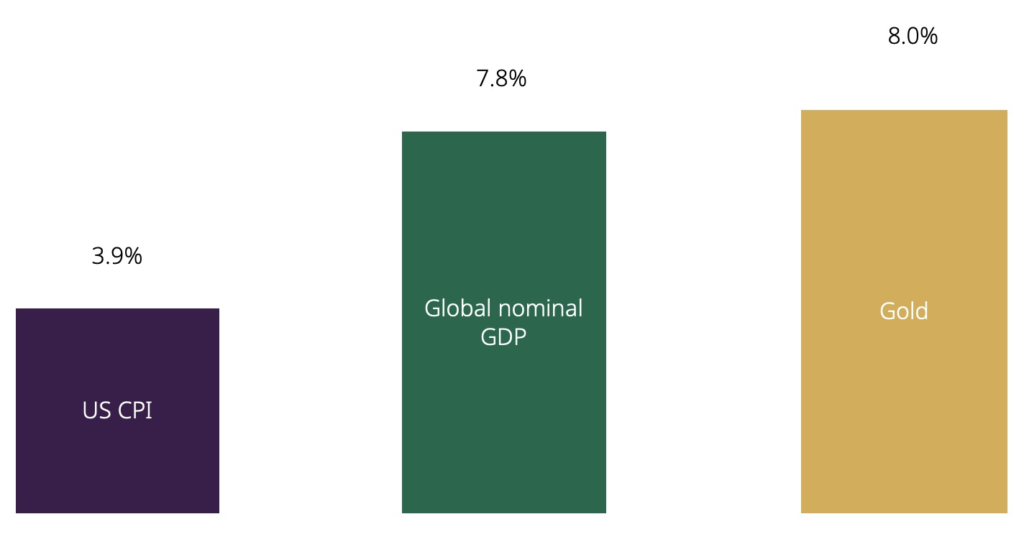

But, as the WGC analysis illustrates (see graph on the right), gold’s long-run return has been well above inflation for over 50 years, more closely mirroring global gross domestic product (GDP).

According to the WGC, the existing frameworks for estimating gold’s long-term returns lack a robust approach that aligns with the capital market assumptions for other asset classes. Specifically, they fail to consider an economic component on top of the financial component that previous models focused on.

Instead, the Council introduces a new model — Gold Long-Term Expected Returns, or GLTER — that combines an economic component, proxied by global nominal GDP, and a financial component, proxied by the capitalisation of global stock and bond markets, and assesses the influence of each of these variables using regression analysis.

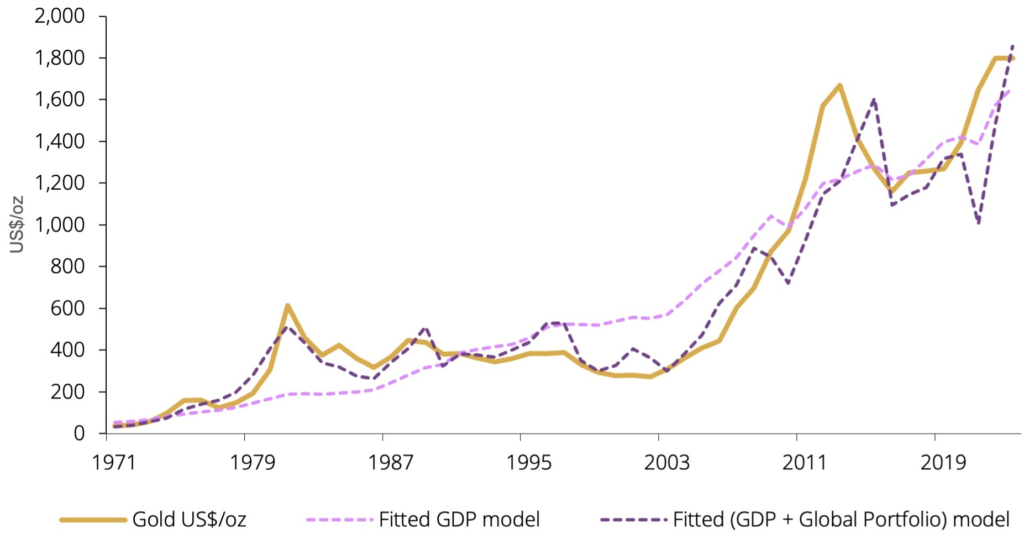

Analysis of regression results for two specifications, one of gold and GDP only, and one of gold and both components, reveals that gold’s long-term expected returns are explained by three parts global nominal GDP growth less one-part global portfolio growth — meaning GDP is the primary driver of the gold price in the long run.

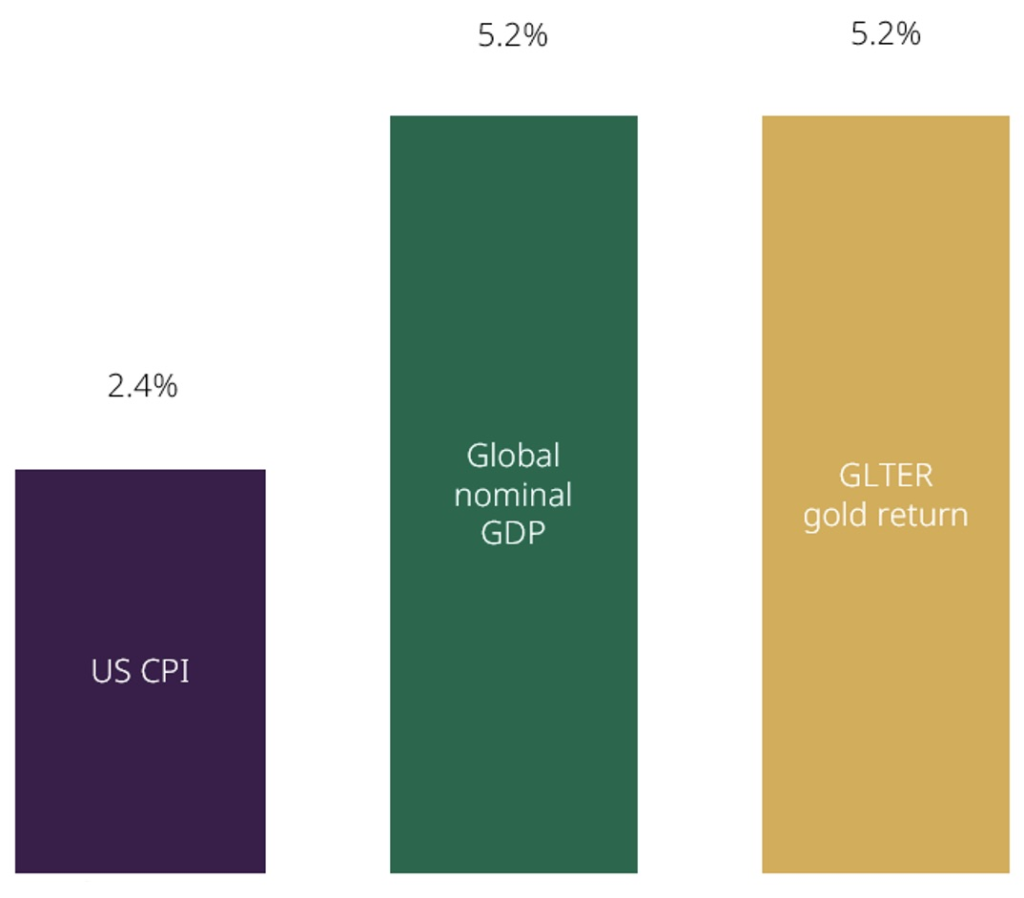

The results show that the estimated average gold return over the 2025-2040 period will exceed 5% per year which is well above that produced by most other models. Specifically, the estimate exceeds common long-term return assumptions such as a zero real return (2.4% nominal in line with expected CPI inflation) over the next 15 years, or a gold return equivalent to the risk-free rate (2.9% for short-term US Treasury bills).

While this return is lower than the historical return observed from 1971 to 2023, this is largely down to a lower expected growth in global GDP, the WGC says, adding that the impact is likely to be similar for the expected returns of all assets.

“In our view, any model that fails to account for economic growth alongside financial factors will prove insufficient in establishing gold’s long-term expected return,” the WGC authors noted.

Compared to the Council’s other pricing models, GRAM and Qaurum, the GLTER places greater emphasis on economic expansion, which it finds to be the primary driver of gold in the long run.

This model also helps to explain why gold’s long-term return has been, and will likely remain, well above inflation, the WGC says.