The IT infrastructure market is undergoing its own kind of climate change thanks to the overheating of the market due to the GenAI boom. Just like real climate change makes it difficult for the existing models to accurately predict the weather, and constant model tweaks and limited relatively current data makes it hard to regain accuracy, it is getting increasingly difficult to predict what server, storage, and networking spending will be from here to the end of the decade.

Not even an AI model can do it with any accuracy, if that is any consolation.

But businesses run because people try to predict the future and then take inputs – data, wood, steel, plastic, whatever – to make outputs – information, furniture and flooring, cars and beams, containers and car parts, whatever – there is no escaping the fact that someone, everywhere, has to take a stab at predicting all of these little futures. Usually, what most people do is gather up a bunch of different opinions about a microeconomic or macroeconomic phenomenon, throw out the crazy ones, take a weighted average of what is left, hope for the best, and take action. And our collective actions collapse all those possibilities down to a very hard-seeming reality.

It is a very quantum thing, if you think about it. Our individual action (and inaction), impelled by our sentiments, which themselves come from collective scatter-gather data analysis operations, makes an economy real.

In the lead up to Nvidia’s GPU Technical Conference 2025 extravaganza next week, the augurs at IDC have put out an AI infrastructure spending forecast, which gives us some food for thought. The data comes from the Worldwide Semiannual Artificial Intelligence Infrastructure Tracker, which is put out twice a year, not quarterly. (At least for now.)

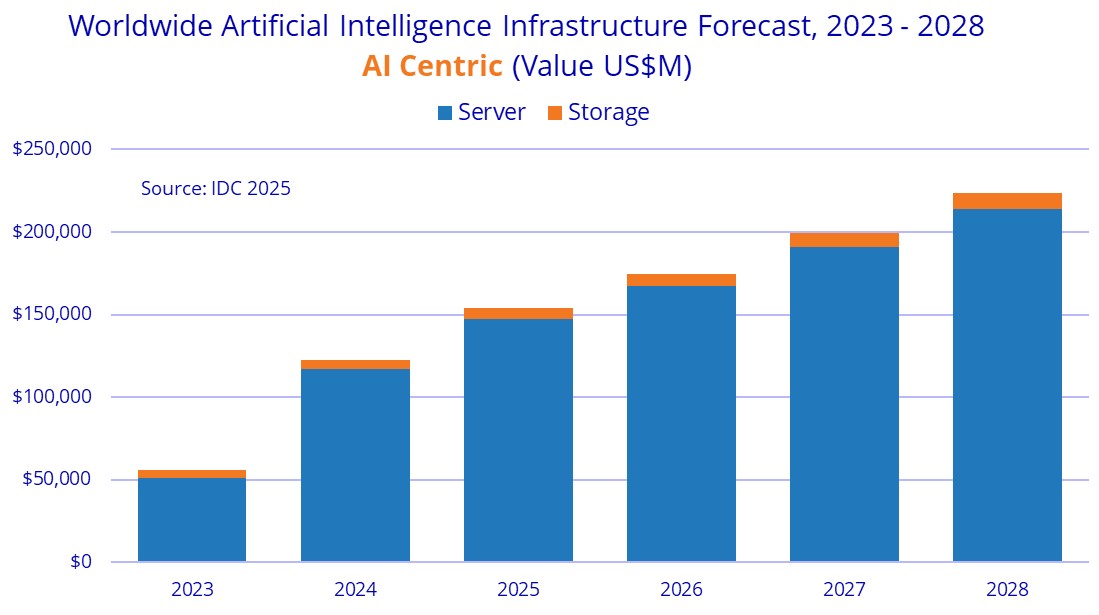

IDC does not put out tabular data for server and storage spending anymore, and in fact stopped giving out this data publicly, as it did for nearly three decades, a few years back. So did Gartner. And so, we have to make do with the information that they do put out.

In the report that IDC released ahead of GTC 2025, the text talks about the first half of 2024 but the chart accompanying the speech shows annual spending from 2023 through 2028, inclusive. It takes a long time to sort out the double counting in server and storage data and looking through the financial reports of public companies to make this model, which is why there is a six month lag. Both server and storage spending are included in the historical data for 2023 and 2024 and for the forecasts of spending beyond that.

In the first half of 2024, according to IDC, AI infrastructure spending rose by 97 percent to $47.4 billion. Of that revenue to OEMs and ODMs for servers and storage, 95 percent of that was for servers and only 5 percent was for storage. Server spending grew at 105 percent, says IDC. If you do the math on that, AI storage spending only grew by 13.1 percent to reach $2.4 billion in the first half of 2024.

IDC says further that AI servers in the cloud (including hosted iron) drove 72 percent of AI server revenues, which works out to $32.4 billion in the first half of last year, which left $12.6 billion in on premises machinery. The prognosticators at IDC also said accelerated machines – those with GPUs and other XPUs – drove 70 percent of AI server sales in 1H 2024, and by 2028 that share will rise to 75 percent. (Which means 30 percent of the AI server revenue today and 25 percent four years hence will be for CPU-only machinery with their own accelerators. CPUs do not go to zero when it comes to AI processing.)

Of that $2.4 billion in AI storage sales in 1H 2024, about $950 million of that was for storage capacity on a cloud and the remaining $1.42 billion was for on premises storage. We are very surprised that storage is such a small portion of the AI infrastructure budget, and we think that this will change over time as companies realize they need to have a unified storage approach so they can pull data out of object, file, and database stores to inject into AI training and inference models on the fly.

We are equally surprised that networking is not part of this model, which would probably be somewhere on the order of 15 percent of a larger AI infrastructure pie.

Here is the IDC forecast for AI infrastructure spending running from 2023 through 2028:

Given how much money Nvidia has made selling raw components and some finished systems already, and what we think it could reasonably do in calendar 2025 through 2028, we made an overlay to this IDC chart:

We took Nvidia’s actual datacenter revenues, which are one month out of phase with the annual calendar and “calendarized” it for each quarter. (This is not hard. Yiou divide all the quarters into three, and in each quarter, you take off one third of the fiscal quarter and add one third of the prior fiscal quarter and that is the calendar quarter.) Then we slapped together a reasonable projection of Nvidia’s annual calendar revenues for its Datacenter division, and calendarized that, too. The asterisk in each note above is about where we expect Nvidia’s datacenter revenue to be each year.

Our projection may look like it is linear, but it is not. In fiscal 2024, Nvidia’s Datacenter division grew by 216.7 percent to $47.53 billion, and in fiscal 2025 it grew by 142.4 percent to $115.2 billion. We think Nvidia will grow datacenter product sales by 59.4 percent in fiscal 2026 to $183.6 billion, by 41.7 percent to $260.1 billion in fiscal 2027, and by 29.7 percent to $337.4 billion in fiscal 2028, and by 21.7 percent to $410.7 billion in fiscal 2029. Which correspond to calendar 2025 through 2028 years.

And as you can see, we think if current trends persist and that GenAI is effective at replacing people or enhancing them in their work, then Nvidia’s sales will be larger than the entire market IDC is predicting. If you want to be conservative, then you can put the Nvidia revenue on the chart below the storage layer in the bar chart and call it a day.

Reality is very likely to be somewhere between these two levels of spending, and while no one is saying this, there can be shocks to the economy or changes to AI models that mean they need less iron and therefore the revenue for the market overall will shrink – exactly the fear the DeepSeek model from China stoked a few weeks ago – unless models need much more capacity even still.

This inevitable and insatiable appetite for AI processing is something that Jensen Huang, Nvidia co-founder and chief executive officer, believes strongly in, and what he thinks will propel Nvidia to new heights. And possibly higher than anything any of us have ever seen.

As we say so often here at The Next Platform, we shall see. The only way to accurately predict the future is to live it – and even that is more uncertain than you might think.