Asia private M&A in 2026

Buyout activity slowed further in early 2026

Asia saw low levels of M&A activity in Q1 2026, and this was also seen in the buyout space. The level of buyout activity was well below both the value and volume seen in Q1 over the last few years, with values falling below Q1 2024, which was a particularly slow-starting year. This continues the stop-start approach to deal making that we have seen in private capital markets in recent quarters. Given the magnitude of the drop in both deal value and volume in early 2026, there appears to be a broad-based slowdown rather than a shift towards smaller or more opportunistic transactions.

While Q1 is typically characterised by early year softness, the extent of the decline indicates that the current geopolitical uncertainty, valuation gaps and financing considerations continue to constrain transaction execution.

The impact of the war in the Middle East is affecting market sentiment and will continue to do so as people reassess their global allocations. We spoke last year of the decline of allocations to the US, and we are now hearing an increasingly positive sentiment to greater allocations to north Asia – it being seen as more stable in the short-medium term with bright spots such as the Hong Kong IPO market continuing to drive growth.

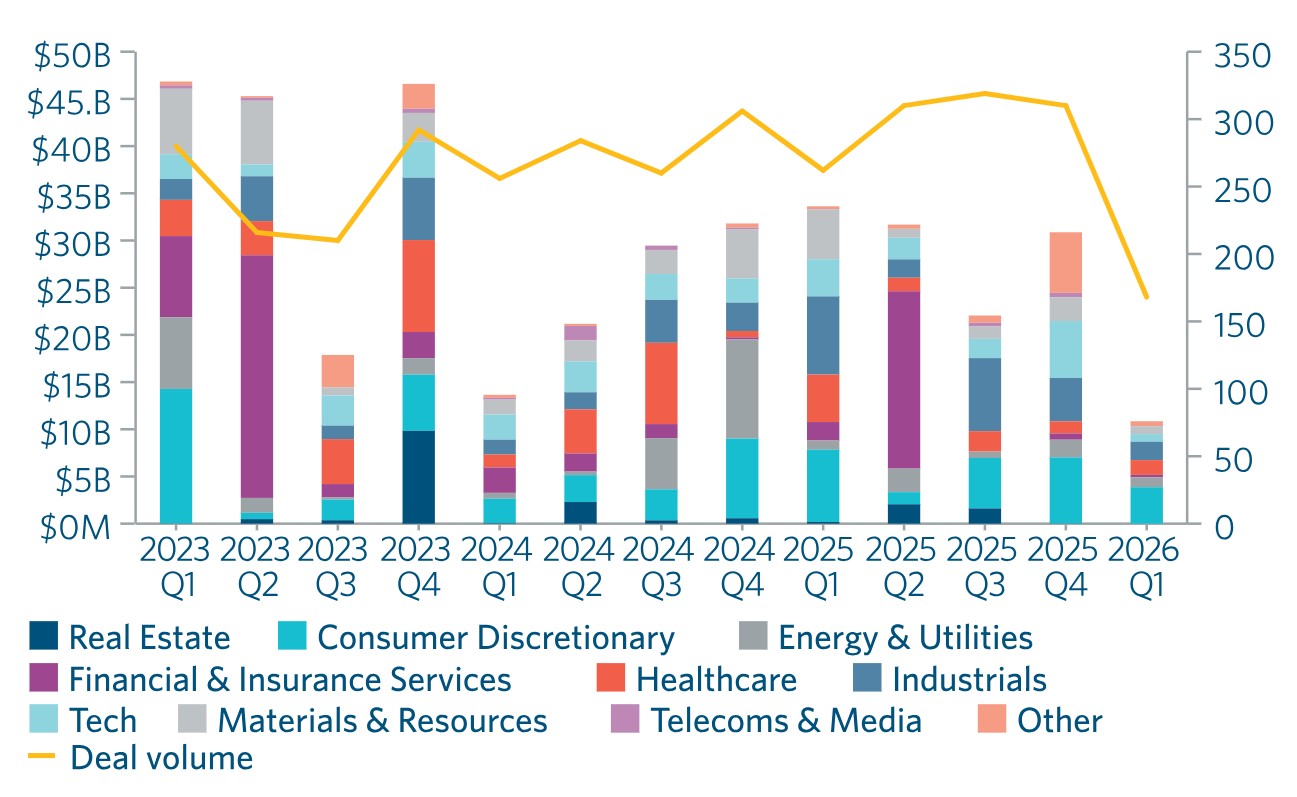

Consumer and industrials lead Q1 buyout activity

Source: Preqin, data as of 2nd Apirl 2026

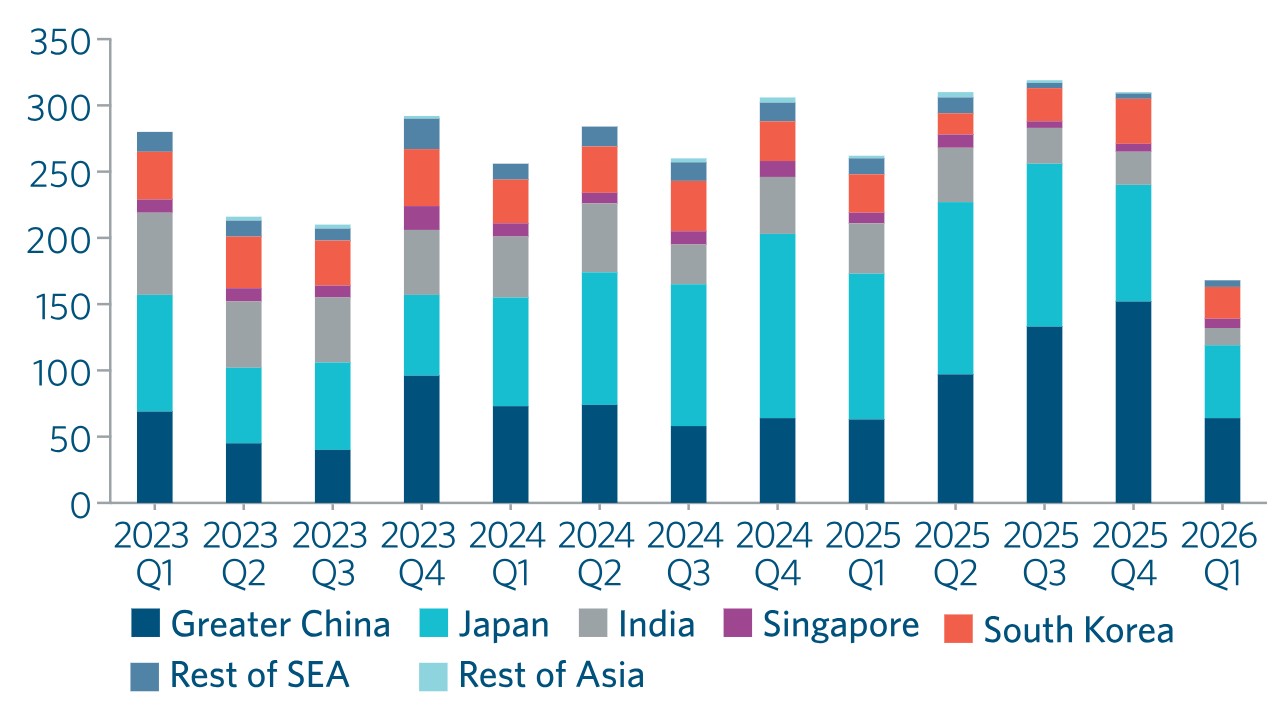

Established markets continue to account for the majority of activity

China remained the largest M&A market by deal value in Q1 2026, although activity moderated following the rebound during 2025. Japan continued to rank second, supported by domestic consolidation and sponsor involvement, but also experienced a noticeable deceleration at the start of the year. These two markets will be key drivers of private capital activity in the coming year. In China, reforms to boost domestic consumption and a sense that the property market has stabilised have given a greater sense of optimism. Japan is also on private capital’s radar for carve outs driven by corporate governance reforms and the weak yen is also providing value.

India remained among the more active markets, driven by ongoing consolidation and sponsor led transactions, although volumes were below levels observed in earlier peak periods. Korea and Singapore also recorded lower activity levels, reflecting a generally cautious regional environment rather than market specific factors.

Japan continues to show signs of slowing

Source: Preqin, data as of 2nd April 2026

Sector trends: familiar leaders, lower volumes

Industrials, financial services and technology continued to account for the largest share of Asia M&A deal value – although no sector was immune to the general slowdown in activity. These sectors have consistently underpinned regional activity, supported by long-term themes such as digitalisation, infrastructure investment and financial sector restructuring. It will be interesting to see how the nervousness in the markets around private credit’s exposure to technology and the disruption caused by AI will affect these sectors in Asia, but, for the moment at least, we are still seeing strong interest, particularly in digital infrastructure.

Asia M&A activity 2019-YTD 2026: Target industry by deal value (USD)

Source: LSEG, Asia target company, announced deals between Jan 2019 – YTD 2026. Deal status: completed or pending

Heightened uncertainty

While Asia M&A activity was subdued at the start of 2026, engagement levels and deal pipelines still remained reasonably robust. EQT’s closing of Asia Pacific’s largest ever private equity fund at US$15.6 billion shows that there is strong investor appetite for the region (albeit with the announced closing coming shortly after the end of Q1 so not quite early enough to be in the data). Interestingly, the fund attracted 75 new investors with a globally diversified investor base – supporting the view that Asia could see an uptick in allocations as investors rebalance geographical weightings.

We expect activity to recover gradually as the year progresses, supported by increasing pressure to deploy capital, create exit opportunities and pursue strategic consolidation. As we discuss below, secondaries could be coming of age in Asia to support increased exit opportunities. Although any recovery is likely to be uneven, with geopolitical and regulatory considerations continuing to act as constraints on execution.

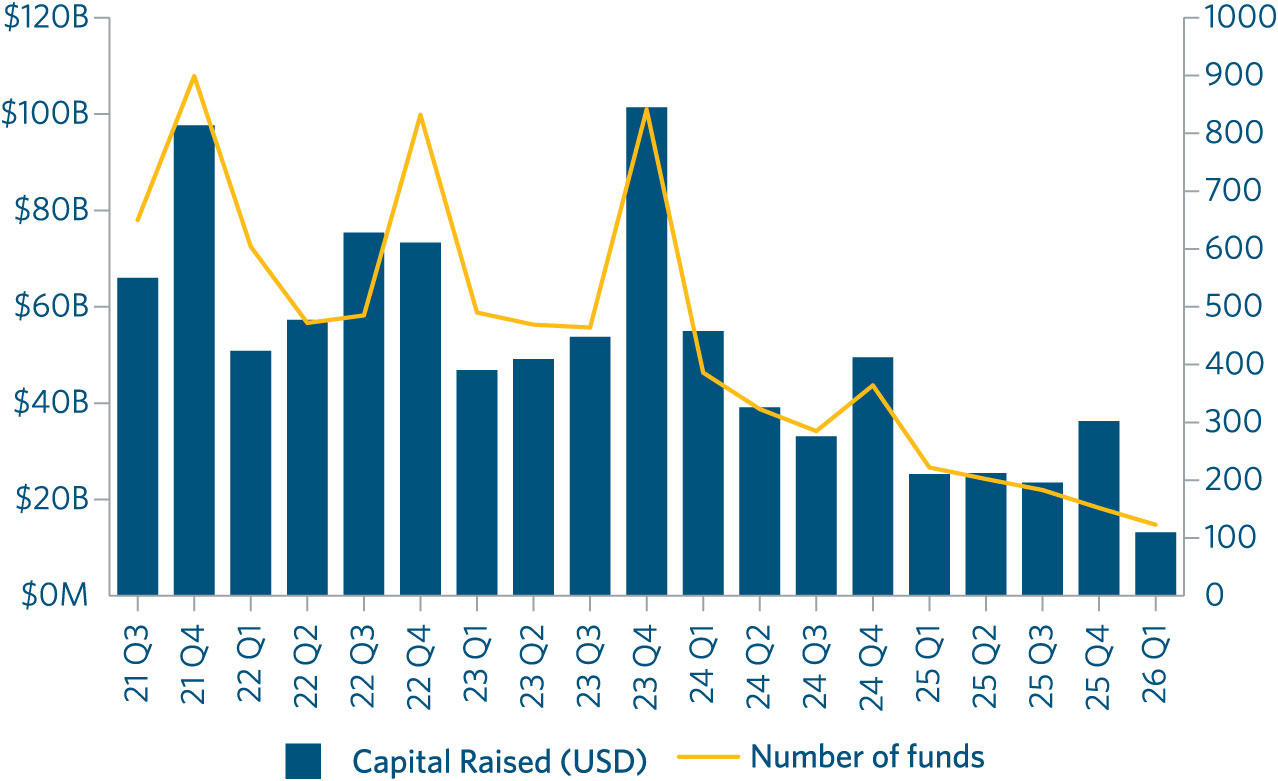

Asia fundraising drops further, all eyes on secondaries

Continued pressure on Asia fundraising amid geopolitical uncertainty

Fundraising in Asia dropped to another low in Q1 2026. While Q4 2025 saw the usual uptick in capital raised due to several closings late in the year, the size of that uptick was well below the Q4 upticks in previous years – and even this small momentum did not carry forward into Q1.

Quarterly Asia private capital fundraising

Source: Pitchbook, based on capital raised by closed funds

Interestingly, while in previous years the number of funds holding a closing jumped in Q4 alongside volume raised, this was not the case in 2025. This reflects the extremely difficult fundraising conditions for many GPs.

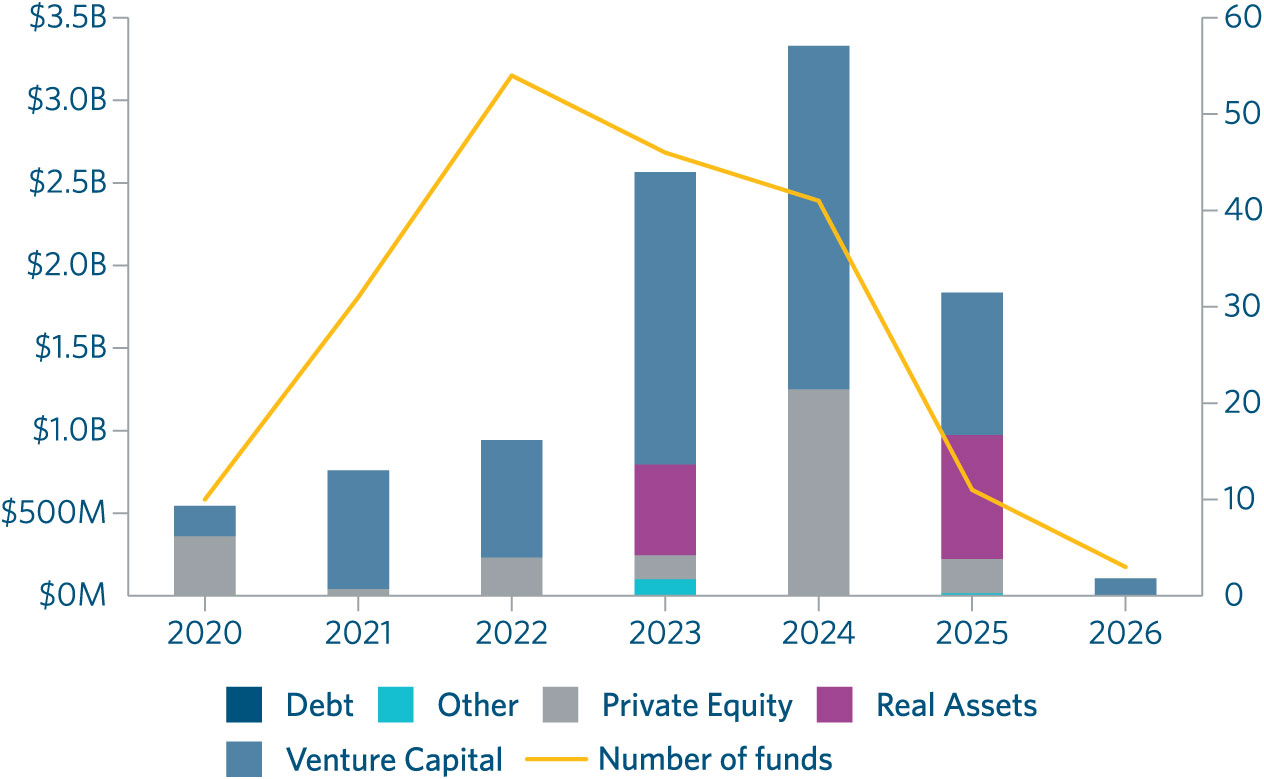

Fundraising declined across all asset classes. Secondaries fundraising, which went from strength to strength over the past few years, showed a particularly pronounced decline.

Asia-based secondaries by asset class

Source: Pitchbook, based on capital raised by closed funds

We believe that two main factors are weighing on fundraising:

- geopolitical uncertainty, including more complex sanctions and national security review regimes, such as the US outbound investment rules; and

- distributions are still lagging behind expectations, with IPO exits picking up but not yet fully translating into sufficient return of capital to investors.

Geopolitical uncertainty is limiting deployment by some of the largest investors, which are often sovereign wealth funds. Apart from the obvious concern of geographical selection, these investors are disproportionately affected by changing sanctions regimes and national security reviews. The associated risks necessitate more careful due diligence on funds before investing and sometimes lower commitments to avoid crossing certain ownership thresholds.

The list of the 10 largest funds closed in 2026 so far reflects these circumstances and is dominated by China and India-focussed funds, including four RMB funds. Domestic funds that do not rely on international investors are evidently not as affected by geopolitical headwinds.

Source: Pitchbook, top 10 Asia based closed funds, Q1 2026

Liquidity in the exit market is still limited, even if improving. The slowdown in secondaries fundraising suggests that secondaries funds raised in previous years still have sufficient capital to deploy and that GPs with eligible assets continue to hold on to these assets for longer.

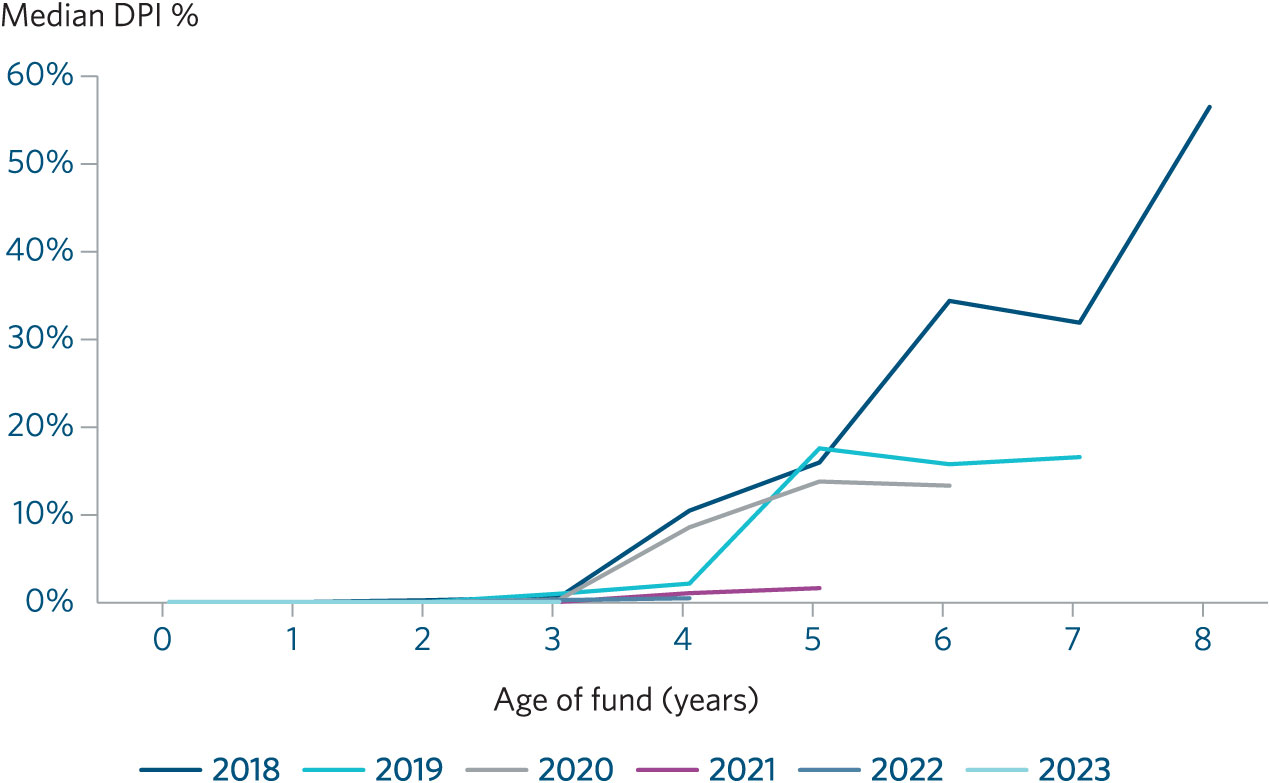

The latest data shows that GPs have been focussed on generating exits for 2018 vintage funds, while 2019 and 2020 vintage funds continue to lag behind. This may be setting the scene for a strong year for continuation vehicles in Asia.

Newer vintages are showing delayed distribution trajectories

Source: Preqin, median DPI at age of fund

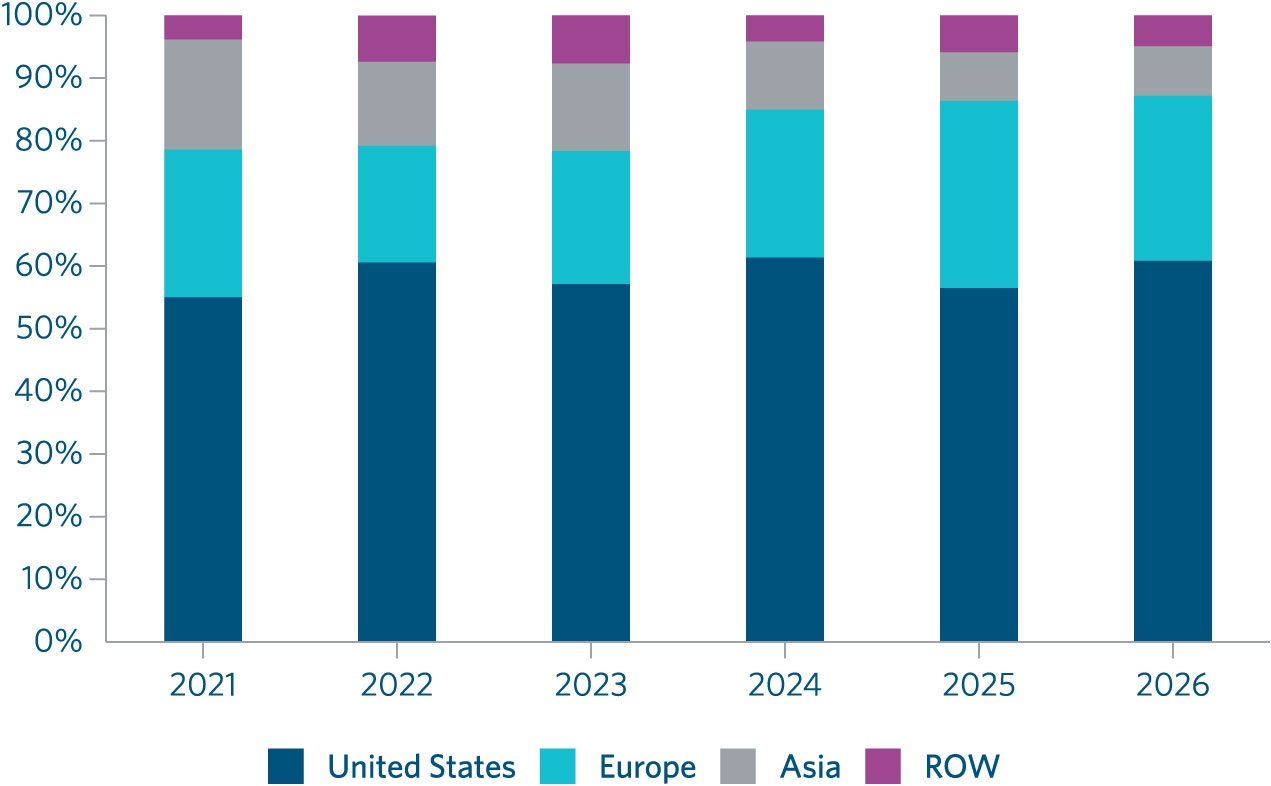

The trend of fundraising shifting to Europe did not carry over into Q1 2026, with early figures for 2026 suggesting that US fundraising has regained its momentum. It is too early to tell of course where fundraising will end up this year, but we can certainly say that US fundraising is not dropping off significantly for now.

We suspect that there are two key factors at play. One might be that the capacity of Europe to absorb the inflows has hit limits. Another may be that the US is still considered the safest place to invest in private assets, with the most sophisticated GPs.

Asia fundraising in Q1 has marginally increased its share of the global total in Q1. We are cautiously optimistic that this trend will continue throughout the year.

Geographical allocation

Source: Pitchbook, based on capital raised by closed funds

All eyes on secondaries

With 2018 to 2020 vintages looking for exits and secondaries funds having sufficient dry powder, many of our conversations with GPs in the recent weeks have centred around secondaries.

We are seeing strong interest in continuation vehicles to allow remaining assets in these funds more runway to exit while generating as much liquidity for existing investors as possible. Judging from our recent conversations with secondaries investors and GPs, more GP-led transactions are likely to come to the market in Asia this year.

As noted in previous editions of our quarterly updates, the Asia secondaries market is disproportionately small compared to Asia’s share of global private capital formation, particularly when it comes to GP-led transactions. While continuation vehicles are well established in the US market and increasingly common in the European market, they have been few and far between in Asia.

Consequently, there is limited experience with these transactions among advisers in Asia. This in turn has slowed the development of the secondaries market in Asia, creating a self-limiting cycle.

An increase in continuation vehicle transactions in Asia is an opportunity for advisers to catch up and create a more sophisticated market with Asian characteristics.

Our disputes update below examines the development of continuation vehicles in Asia in further detail. We point out the main risks that Asia GPs should consider when planning a continuation vehicle to avoid disputes with investors – with commentary from our market-leading disputes resolution experts.

Our outlook for the year ahead

From an Asia perspective, the Q1 figures are of course disappointing. However, these figures go against the market sentiment that we observed in Q1. In fact, we generally saw an increase in deal activity and interest in Asia among our clients. We therefore remain cautiously optimistic about Asia fundraising for the remainder of the year, with distinct opportunities for secondaries for 2018 and 2019 vintage funds.

We also expect that the uptick in exit activity via IPOs and secondaries will then translate into increased fundraising activity, and that the headline fundraising figures for Asia will improve in Q3 and Q4. Geopolitical uncertainty remains the main risk factor for private capital fundraising in 2026.

Disputes

Rise of continuation funds and potential for conflict between GPs and LPs

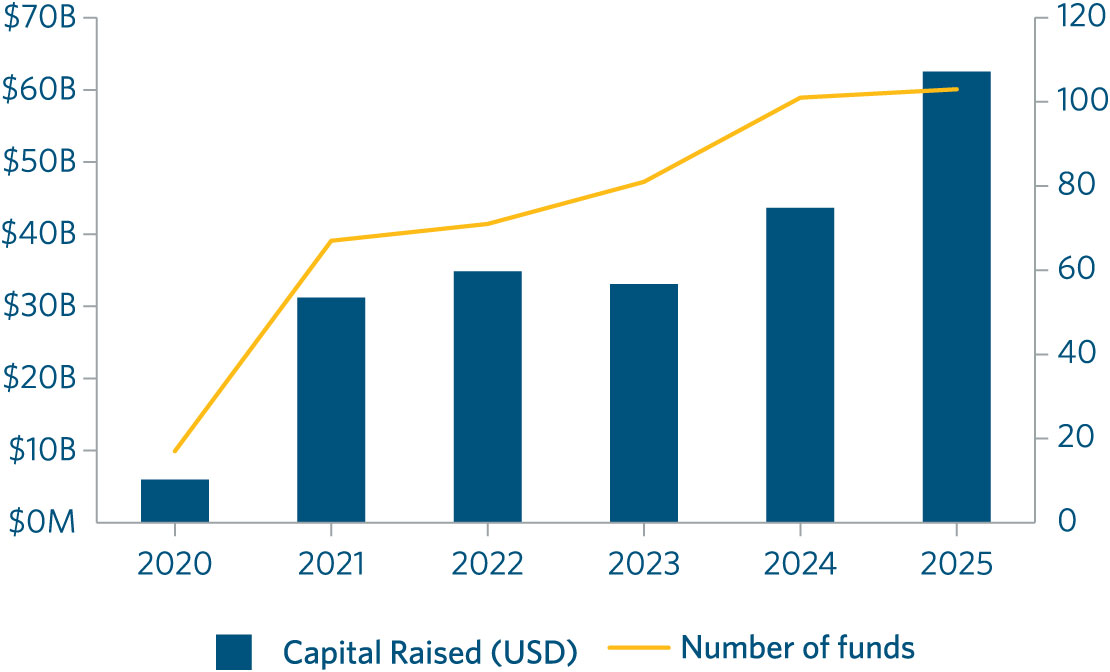

Continuation fund transactions have been increasing globally for several years, and the trend continued in 2025. The data shows approximately 100 transactions with an aggregate value of approximately US$60 billion, dwarfing the number and value of transactions in this space that were happening only a few years ago.

Continuation vehicle fundraising based on closed funds 2020 – 2025 (Global)

Source: Pitchbook, based on capital raised by closed funds

With an increasing number of continuation fund transactions, there is a potential for a greater number of disputes between LPs and GPs. This is because of the inherent challenge GPs face when acting on both sides of the transaction, as the seller (for the original fund) and the buyer (for the continuation fund). Unless the process is managed carefully, allegations of conflicts can easily arise.

One of the most visible examples is the litigation between ADIC and EMG in the US courts in December 2025. In that case, ADIC sought to halt a transaction on the basis that the GP had breached its fiduciary duties to the LPs in the original fund, by selling the asset at an undervalue and providing different information to different investors to get support for the transaction. The result of the litigation was that the transaction was temporarily blocked, pending review by an independent arbiter.

As a result of this case, LPs will be more attuned to their rights and assertive in enforcing them. The volume of transactions, and the inherent risk of conflicts, means that disputes between LPs and GPs in continuation fund deals are likely to increase over the coming years.

Continuation vehicles in Asia and risks arising from lack of expertise

In contrast to the global picture, the use of continuation funds in Asia is much lower and their growth is considerably slower.

Continuation vehicle fundraising based on closed funds 2020 – Q1 2026 (Asia)

_Graph-6.jpg)

Source: Pitchbook, closed funds with a CV fund structure

Although the number of transactions has grown over the past few years, they are still in the single digits, and the aggregate value is around US$1 billion. (The exception was 2022, where a GLP continuation vehicle closed at US$5 billion.)

As noted above, one of the factors limiting the use of continuation vehicles in Asia is a relative lack of adviser expertise and institutional knowledge; in turn, the limited number of deals slows the development of this expertise.

We see this as a risk factor that GPs should take into account when considering a transaction through a continuation fund. Balancing the interests of the investors on both sides of the transaction requires careful handling of the substantive and procedural aspects of the deal. A lack of expertise or attention to detail on these issues can mean that the balance is not achieved, and one set of investors is aggrieved – potentially resulting in litigation as seen in the ADIC/EMG case.

Variance in NAV discounts

Pricing is at the centre of the conflicts of interest that a GP has to manage in connection with a continuation vehicle transaction.

From a global perspective, in 2024 and 2025 assets sold into continuation funds were generally priced at a modest discount to NAV.

Roughly two-thirds of transactions (by value) involved a discount to NAV of 5% or less; and around 80% to 90% involved a discount of 10% or less. Single asset funds did not enjoy a noticeably higher price (i.e. lower discount) than multi-asset funds, despite single-asset funds often comprising ‘trophy’ assets which can command a premium.

However, there are a significant number of transactions that involve a discount of 20% or more. In those cases, LPs may question whether the transaction has been fairly priced and whether the continuation fund investors are getting too much of the upside. It will be important for GPs to be able to demonstrate that the valuation is fair and that proper procedures were used to obtain informed approval for the deal.

Key takeaways

GPs can avoid litigation by structuring the transaction prudently and working with existing LPs and new LPs.

Key sources of disputes between LPs and GPs are likely to be:

- Valuations – are there good grounds for the valuation (eg, a fully informed fairness opinion and/or lead investor scrutiny)?

- Information – has the GP been transparent with the LPs, and provided consistent information to investors on both sides of the deal?

- Procedures – have approval procedures been followed with sufficient time and information for proper deliberations of advisory committees and LPs generally?

If there are shortcomings on these matters, then LPs may have the tools to slow or block deals through action in the courts or arbitral tribunals

[View source.]