Last month, J.P. Morgan released its first ever Global Family Office Report summarizing how some of the wealthiest households on Earth manage their money. One of their most notable findings was that the average family office allocation to alternatives was 46%.This sizable allocation to alternatives, which includes private equity, hedge funds, and real estate, among others, raises an important question for retail investors: Do you really need alternatives to get rich?

While it can be tempting to copy the asset allocation of the ultra-wealthy, it’s also crucial to understand when their investment strategies are suitable for the typical investor. In this blog post, I’ll explore the role of alternative investments in wealth creation and discuss whether they are necessary for achieving financial success.

But before we can discuss whether alternatives can make you rich, let’s first define what they are and some of their core characteristics.

What Are Alternative Investments?

Alternative investments are a broad category of assets that fall outside the realm of traditional investments like stocks, bonds, and cash. They often have less liquidity, higher fees, a higher minimum investment, and more complex structures than the more traditional investment vehicles. Some of the most common types of alternative investments include:

- Private Equity: Direct ownership in private companies or buyouts of public companies, often with the goal of improving operations and increasing shareholder value.

- Venture Capital: Equity investments in early-stage, high-growth potential startups and companies.

- Hedge Funds: Actively-managed pooled investments that employ a wide range of strategies including: long/short equity, relative value, and global macro, among others.

- Real Estate: Direct ownership or financial interest in residential or commercial real estate properties. These can be done through private transactions or real estate investment trusts (REITs) of various kinds.

- Private Credit: Private arrangements for extending credit that are negotiated directly between the lender and borrower, outside of the traditional banking system or public markets.

- Collectibles: Ownership of tangible assets that are rare, unique, and have the potential for appreciation in value over time. Some notable collectible asset classes include: art, fine wine, rare coins, and classic cars, among others.

The benefit of using alternatives is the potential for higher returns that are less correlated with traditional financial assets. While each of the asset classes listed above will have a different correlation with stocks, bonds, and cash, the hope is that these alternative asset classes will provide a diversification benefit that you cannot get anywhere else. As a result, investing in alternatives should improve your returns while also lowering your portfolio’s overall volatility.

However, these benefits don’t come without costs. One of these costs is less liquidity. Unlike publicly traded stocks and bonds, alternatives can be difficult to sell quickly or at a reasonable price. As a result, your capital can be locked into an alternative investment for much longer.

In addition, alternatives tend to have higher fees and higher minimum investment requirements than traditional asset classes. You need to have lots of money to access these assets and you have to be willing to pay the price of admission (the fee). When the returns are high enough, it can all be worth it. However, when alternatives underperform, it can feel like you are getting a bad deal.

Lastly, many alternatives are less regulated and more complex than traditional asset classes. As a result, it can be difficult to understand how they work and the exact risks you might be taking.

Overall, alternatives can be a great diversifying asset class for your portfolio. However, they also can be harder to sell, more expensive, and more complex than many traditional asset classes. Make sure to think through these tradeoffs before you consider investing a large sum of money into an alternative asset class.

Now that we’ve defined what an alternative investment is, let’s look at how the wealthy actually allocate their wealth to the alternative space.

How Do the Wealthy Allocate to Alternatives?

We already know that the wealthy have nearly half (46%) of their investable assets in alternatives, but which ones do they prefer? According to the J.P. Morgan Global Family Office Report, here is how this 46% is broken out:

- Private Equity: 17%

- Real Estate: 15%

- Hedge Funds: 5%

- Venture Capital: 5%

- Private Credit: 4%

As you can see, the vast majority of alternative investments are in private equity and real estate. Private equity typically involves investments in private companies where the goal is operational improvements and increased profitability. When a private equity deal goes well, the new and improved company is typically sold off at a higher valuation.

On the real estate front, wealthy investors are able to capitalize on the many tax advantages that this asset class has to offer. For example, if you learn about how 1031 exchanges work, you will see why so much wealth has been built in this asset class. And note that I am referring to real estate investments, not someone’s primary home. According to the Survey of Consumer Finances (2022), households with a net worth greater than $100 million typically allocate only 3% of their total assets to their primary home. While your primary home can be an investment, this is generally not how the wealthy use this asset class.

Now that we’ve looked at how the wealthy invest in alternatives, you may be wondering how the other 54% of their portfolio. Thankfully, J.P. Morgan provided that data as well:

- Public Equities: 26%

- Fixed Income & Cash: 21%

- Commodities & Other: 7%

Note that the “Fixed Income & Cash” category is broken down into Investment Grade Fixed Income (10%), High Yield Fixed Income (2%), and Cash (9%).

While the wealthiest investors are known for investing into alternatives, technically they have more of their money in traditional asset classes (e.g. stocks, bonds, and cash). This may come as a surprise to you, but the wealthy use many of the same wealth building tools that everyone else has access to. While it’s easy to focus on what the wealthy do differently, maybe we should be focusing on what they do that is the same.

Why You Probably Don’t Need Many (If Any) Alternatives

Though alternative investments play a large role in the portfolios of the ultra-wealthy, they are not a prerequisite for building significant wealth. First, the wealthy tend to invest in these alternatives after they’ve already become wealthy. Otherwise, how else would they afford the large minimums that are typically required to invest? Second, many of the supposed benefits of these asset classes may not be as advertised.

For example, one of the primary reasons to invest in alternatives is due their low correlation to traditional asset classes. Unfortunately, this “low correlation” may simply be an artifact of how often the data is collected. If your assets are less liquid and you value them less often than traditional assets, then they may seem less correlated to traditional markets even though they aren’t.

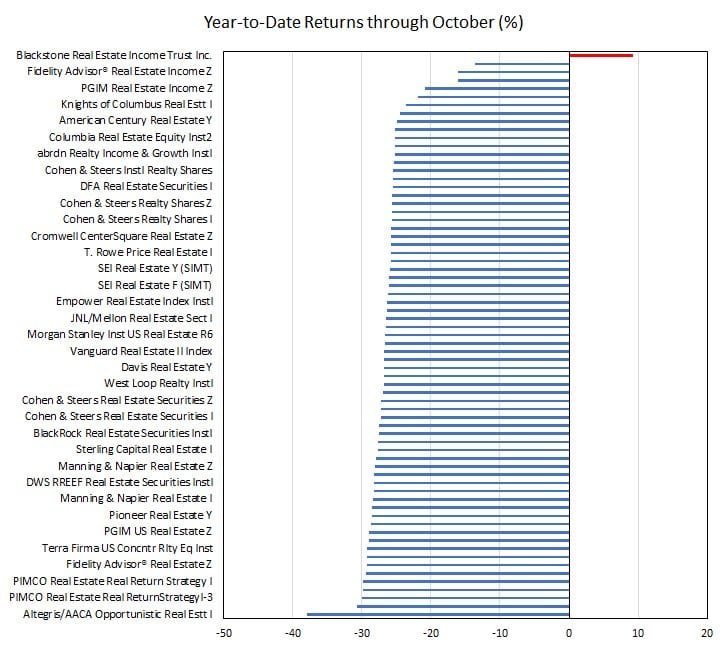

My favorite example of this comes from Blackstone’s Real Estate Income Trust (BREIT), which according to Blackstone’s own data, had nearly a 10% positive return from January 2022 to October 2022. The only problem is that this positive return occurred while the rest of the real estate sector was getting hammered (as pointed out by @EconomPic):

How is it possible that BREIT was up 10% while the rest of the real estate sector was down double digits? Is Blackstone really that good at selecting properties? Or could something else be going on?

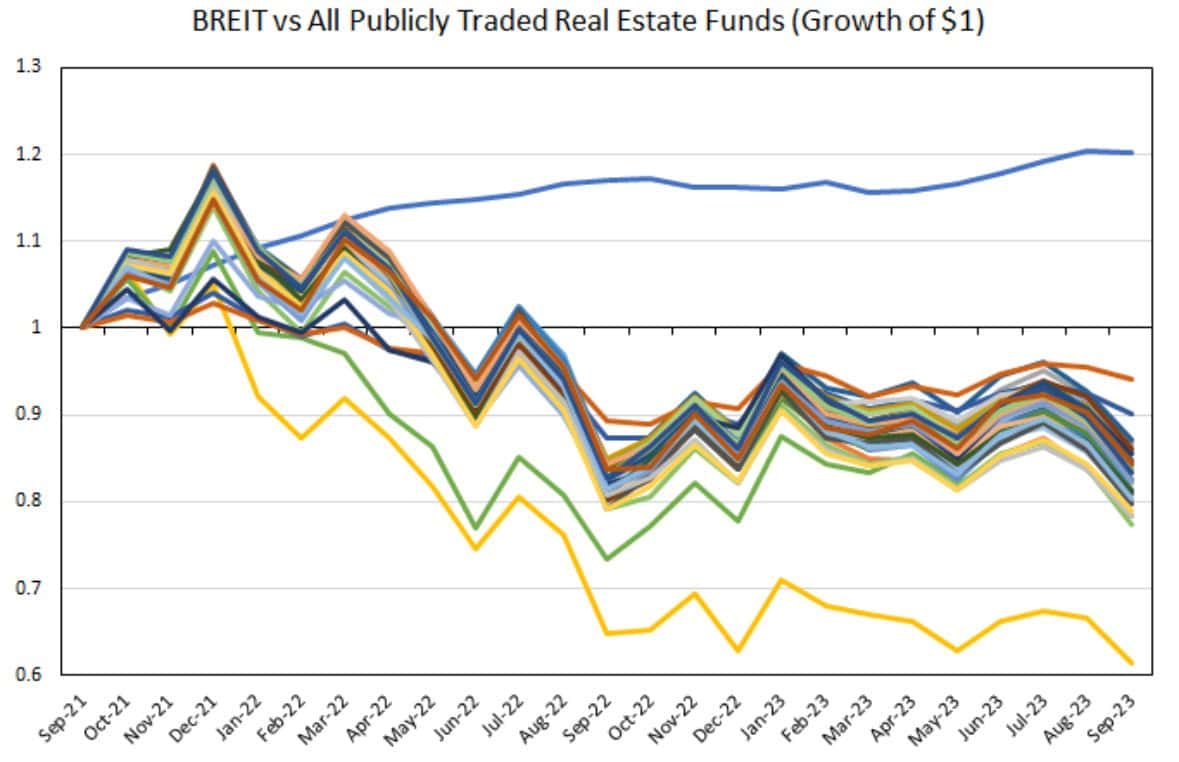

I don’t know with certainty, but when you look at the volatility of their fund (BREIT) compared to the rest of the industry, things seem off. Another gem from @EconomPic:

Yes, this is just one example, but I am inclined to believe that many alternatives are more correlated with traditional investments than the industry wants to admit. After all, if the economy isn’t doing well, it’s highly unlikely that your private equity, real estate, and venture capital investments will be thriving.

Nevertheless, even if these assets don’t provide the low correlation they promise, the ultra-wealthy will still invest in them. Why? Status. There’s nothing sexy about buying an index fund. But put your money into private companies that you can’t find anywhere else and you’ve got yourself something you can sell. If you find this exclusivity appealing, I get it. However, you should find another way to get your status fix and leave your portfolio out of it.

At the end of the day, whether you decide to invest in alternatives is up to you. If you find the possible diversification benefits and exclusivity exciting, that’s great. Just make sure to balance these out against the illiquidity, high fees, and increased complexity that accompany them. It’s also important to remember that the wealthiest investors allocate most of their assets to traditional asset classes like stocks, bonds, and cash. So while alternatives can play a role in a retail investor’s portfolio, they are not the sole driver of long-term wealth creation.

Ultimately, the key to building wealth isn’t in any specific asset class. It’s in the power of consistent, disciplined investing over time. It’s in the continual purchase of income-producing assets.

This is my 400th blog post. That means 400 weeks of writing and 400 weeks of investing. Here’s to the next 400.

Just Keep Buying and thank you for reading!

If you liked this post, consider signing up for my newsletter.

This is post 400. Any code I have related to this post can be found here with the same numbering: https://github.com/nmaggiulli/of-dollars-and-data