Michael Ballanger of GGM Advisory Inc. shares his thoughts on the current state of the junior mining sector, and one copper stock he believes should be in your portfolio.

“The desire for gold is the most universal and deeply rooted commercial instinct of the human race.” – Gerald M. Loeb

Gerald M. Loeb was a founding partner of the famous brokerage house E.F. Hutton, where he honed his skills as a Wall Street trader and investment banker. Having survived the 1929 market crash, that experience marred him for life, creating an investment style that involved “never holding a stock position for the long-term.”

He wrote the book that I have read cover-to-cover three times in forty-five years, The Battle for Investment Survival, which emphasized the concept of cutting losses quickly and letting profits “ride” as a surefire strategy for above-average performance and risk control. It is also in direct contravention of the Benjamin Graham/Warren Buffet rules of investment engagement that dictate that value investors buy and hold securities for longer-term periods.

Loeb’s quote at the top of this page joins the famous quote by J.P. Morgan, “Gold is money; everything else is credit.” in defining how these two merchants of the 1900’s bond and stock markets viewed the one asset that today’s Wall Street mavens view as a “barbarous relic.“

As gold moves to escape velocity above the magical USD $2,500/oz. level, and the SPDR Gold Shares ETF (GLD:NYSE) hits an all-time high this morning, it is instructive to sit back and ponder the remarks of two titans of finance when it comes to their view on gold’s utility within portfolios.

The current Wall Street narrative is now dominated with this nagging debate over the Fed’s next course of action. The “stocks for the long-term” spin machine has done such a wonderful job of training the portfolio managers to drool uncontrollably at the mere mention of rate cuts, it is as if Pavlov has forgotten to ring the bell for a solid week in front of a cage of ravenous, starving canines.

It seems like it was just yesterday that the world was on the brink of a total self-immolation of the banking system thanks to the unbridled overindulgence in leverage everywhere that a commission fee could be levied. The GFC of 2008 was followed by bailout after bailout, replete with outsized bonus pools for all that participated in the sub-prime scam. No jail time, no convictions, and zero regulatory reprimand for any of the architects of the largest public swindle of taxpayer money in the history of the planet.

Yet without mention anywhere amongst the legions of “expert commentators” in the financial media is the fact that gold bullion purchased in January 2003 has outperformed the S&P 500 by a margin of 615% to 529%.

Why is that?

Well, let us start with the fee structure. It is no secret that recommending that a client go on a monthly investment plan for gold involves no rotation, and in the world of Wall Street “comp,” there are much larger fees for turning a client’s portfolio over three or four times a year especially when in-house products with big fat underwriting fees are included. Also, investment banking is a huge source of revenue for Wall Street banks like Goldman or JP Morgan, and again, it is no mystery that “paper” products like IPOs are easier with which to conjure up financial wizardry with huge built-in fees that are geared around “sophistication” (more appropriately called “the ability to confuse and confound“) as they bundle up various layers of credit risk to resemble an AAA-rated security.

You simply cannot do that with a metal that carries the periodic number “79.” In reality, if you really backed out all the fees generated within the perimeter of the S&P 500 realm of companies by the Wall Street geniuses, that 529% for the S&P return would probably be half that number.

In a fit of forlorn reasoning, I decided back in May that I would refrain from adding to my gold holdings until mid-August, a practice that I have used frequently in setting up a year-end portfolio structure that captures gold’s seasonality trade. Because I had my head buried in a seemingly enlightened crevice of self-certainty and intransigence, I anchored the notion that just because I thought it made sense, it just had to happen.

Well, a month ago, I woke up to the reality that gold had decided that perhaps — just perhaps — the “analyst” from Port Perry was going to get left summarily behind in his maniacal quest to pick gold off in the $2,250-2,300 range or the GLD in the $200-205 range before new highs could be possibly achieved.

Alas, as usually happens, I forgot the “Twainian” Rule that goes something like this: “It ain’t what you don’t know that gets you into trouble’; it’s what you know for sure that turns out to be not exactly so.”

I knew “for sure” that gold would bottom in mid-August, and luckily, my hedges on GLD were modest at best, and they did not exactly get me “into trouble.” What it represented was more of an opportunity cost more than a financial cost with a smattering of reputational embarrassment thrown in. Nevertheless, as the famous quote by Martin Zweig goes, “It’s OK to be wrong; it’s unforgivable to stay wrong.”

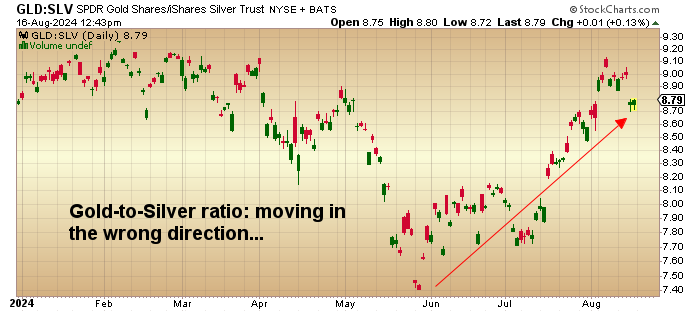

GLD has moved to an all-time high today (which is the exact definition of the term “mid-August) with a move to $231.10, surpassing the prior high of $229.65 last seen on July 17.

iShares Silver Trust (ETF) (SLV:NYSE), by contrast, has failed to come anywhere near its 2022 high of $29.56, last seen on May 20. Using the GLD:SLV to arrive at the gold-silver ratio, the GSR is now at 88.30 up from 74, which marked the May low for that very important ratio. The GSR is the concrete that bonds together all aspects of the gold-silver bull thesis because (and I know you are all rolling your eyes) without this ratio making new lows as the precious metals advance, any rally is doomed. Silver is the speculative spark that ignites the animal spirits that drive the precious metals shares which in turn drives the retail public into the explorers and developers where most of the leverage is contained. To attract the interest (and dollars) of the wild-eyed speculator, there needs to be a “hook.“

Silver fills that roll.

Just as most of the tried-and-true rules surrounding stocks are now prehistoric drivel thanks largely to the predominance of the algobots, it is entirely possible that gold can continue to outperform silver right through $3,000/ounce driven by the current narrative that the main buyers of the precious metals are central banks where record after record continues to be broken in terms of physical offtake.

No such offtake is occurring in the silver arena. Only industrial and investment demand (primarily from retail) drives silver, and thus far, that has been insufficient to replace the sheer volume of central bank buying in the yellow metal. Hence, I have stuck to gold and copper as my top metals to own for the past decade.

Copper

Speaking of the copper market, I have been typing away since the Nikkei “carry trade crash” on August 5, urging subscribers to replace all of the copper names they sold back in May when copper broke below $4.00/lb. bottoming in the $3.92/lb. range joining stocks in that Monday rout.

Copper just initiated a bullish MACD crossover and is now on a “buy signal,” as is the money flow indicator. RSI at 48.73 provides considerable runway for price before it approaches overbought territory so these momentum indicators are pretty powerful reasons to own the red metal.

As for target prices, the 50-dma at $4.33/lb. and the 100-dma at $4.42 will probably cap the advance but if they are taken out, what now must be classified as a “bear market rally” will be reclassified as a “bull market resumption” and the negative implications of the 24.6% correction from the May highs get thrown overboard.

Fundamentals for copper remain strongly bullish, with the most recent comment by RBC being retweeted by Ivanhoe Mines founder Robert Friedland. “An attractive entry point for

The stock touched down on crash day at $39.21, sporting an RSI under 25, and gave me the fortuitous window in which to replace the positions that I jettisoned back in May when the RSI was screaming toward 80 and trading over $53 per share.

The terror I felt in dumping my beloved FCX was overshadowed only by the capital gains I crystallized in both stock and June call options, but for the past three months, I writhed in stressful agony every time the stock upticked a dime or two. Now, I own an oversized position in the company that produces two of my favorite metals for the decade ending in 2030 — copper and gold.

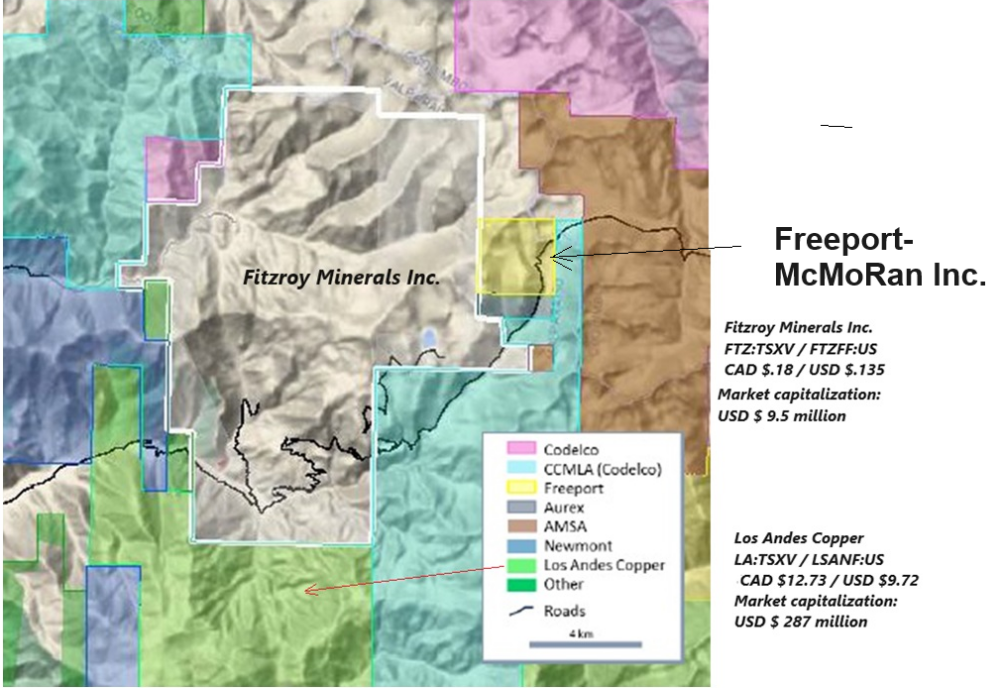

Everyone should visit its website and take the time to review their operations around the world. They are everywhere — including next to my largest junior explorer-developer Fitzroy Minerals Inc. (FTZ:TSX.V; FTZFF:OTCQB)in the Valparaiso district of Chile where FTZ is conducting exploration on the highly-prospective Caballos Copper Property.

The junior miners as a group are still about as challenged a group as I have seen in my forty-five years as an “incubator” of these little guys who have made most of the world-class discoveries in the past five decades. As the Boomers age and settle on clipping coupons and playing golf, the last demographic to experience true financial rapture through mineral discoveries of all types and sizes on all five continents is now a pitiably smaller force than in the 1990s when listening to exploration “stories” was the ultimate in water cooler conversation.

The mania that swept investors into a financing frenzy that brought untold wealth through ownership of juniors finding ore bodies that became world-class mining operations like Dia Met (diamonds in Canada) and Diamondfields (Voisey’s Bay nickel-copper-cobalt) and Eskay Creek (gold-silver) is going to return with a vengeance. This is going to be driven when the Gen-X and Millennial generations suddenly wake up and realize that they are missing the biggest commodity boom in world history.

It was only 15 years ago that I first learned that a “Tier One” gold asset involved a minimum of 5 million ounces, with gold prices at $1,250 per ounce. Today, we are at $2,534. Using simple math, that should mean that a gold project with half as many ounces should now be valued as a “Tier One” asset.

How many junior gold developers out there have 2.5 million ounces in the ground trading for a fraction of a proper “Tier One” valuation?

Dozens upon dozens in jurisdictions like Nevada and Quebec that cannot get a meeting with investment bankers if their lives depended on it. That, my friend, is going to change at a point where rising gold prices force the bankers and the M&A specialists to smell the money and start dialing feverishly to cement banking relationships from these struggling juniors.

It will not just be gold; juniors with copper-gold porphyry or IOCG deposits will be in the queue, readily open for business. As in all eras, it is the allure of fee-generating deals that drives the bankers into the waiting arms of anyone with a story. For most of this decade, that story has been technology and is now cresting with the latest mania called “artificial intelligence.” The rotation I foresee is into the junior exploration space where gold and copper are kings.

As they used to say in the pork belly pit on the old Chicago Board of Trade: “Buy ’em!“

| Want to be the first to know about interesting Critical Metals, Silver, Gold and Base Metals investment ideas? Sign up to receive the FREE Streetwise Reports’ newsletter. | Subscribe |

Important Disclosures:

- As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Fitzroy Minerals Inc.

- Michael Ballanger: I, or members of my immediate household or family, own securities of: All. My company has a financial relationship with Fitzroy Minerals Inc. I determined which companies would be included in this article based on my research and understanding of the sector.

- Statements and opinions expressed are the opinions of the author and not of Streetwise Reports, Street Smart, or their officers. The author is wholly responsible for the accuracy of the statements. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Any disclosures from the author can be found below. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

- This article does not constitute investment advice and is not a solicitation for any investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Each reader is encouraged to consult with his or her personal financial adviser and perform their own comprehensive investment research. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company.

For additional disclosures, please click here.

Michael Ballanger Disclosures

This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.