“Looks like someone is trying to take more than $10,000 from us.”

That’s the message my husband typed to me on a Monday morning in October. By the time I wrote back, he was on the phone with our bank. The weekend before, someone walked into a bank branch, pretended to be one of us, and took thousands of dollars from our checking account.

We joined the tens of millions of Americans who each year are victims of identity fraud, where criminals steal a bank or credit card number and use the personal information to achieve illegal financial gain.

We were lucky in so many ways, most notably that our bank reimbursed our losses within 36 hours.

What we learned is this: The many steps we take to safeguard our personal data don’t always work.

Experts suggest creating strong passwords with extra layers of authentication, changing them often, and not using the same one on multiple accounts.

Having text alerts on your credit and debit cards for all transactions can also thwart illegal activity in real time, as can email alerts when someone tries to change an email or address associated with your account.

You should do all these — and we did — but they wouldn’t have prevented the fraud we experienced. Our data was already out there for the picking.

Hacks that expose the personal financial information of Americans soared to a record high of 3,205 in 2023, according to the nonprofit Identity Theft Resource Center. That total includes breaches of companies across many industries such as healthcare, utilities, financial services, and transportation.

A well-known example of this was the massive Equifax data breach in 2017 that affected 147 million Americans — including us. That motivated us to freeze our credit reports at Equifax, Experian, and TransUnion.

“At this point, all of our information is out on the dark web,” Suzanne Sando, senior analyst for fraud and security at Javelin Strategy & Research, told me. “It’s now just a matter of when is it going to be used against me.”

‘Huge time suck’

Here’s what else we learned: Knowing how to respond to one of these frauds after they happen is also crucial — and time consuming.

Because of my past reporting on this subject, I knew we needed to act quickly. We checked our other accounts — bank, credit, and retirement — for any suspicious activity. There was none. We then met up at our local bank branch to shut down the old account, establish another, and identify which upcoming transactions to allow to go through.

It took more than two hours, and we weren’t close to done.

“Fixing a run-in with identity fraud, it’s a huge time suck,” Sando said, “and people don’t necessarily have the time to do it.”

My husband fortunately was able to take the day off and spent the afternoon undoing automatic transactions from the old account and rerouting them to the new one. I also took off the day from work and headed to our local police precinct to file a report to provide to other financial institutions if the fraud followed us elsewhere.

Our local precinct took our report immediately. That’s not often the case for identity theft, according to Identity Theft Resource Center CEO Eva Velasquez, because it’s so hard to solve these cases.

Several factors worked in our favor, she said. In New York, the total amount stolen — which ended up being $11,300 — made the crime a Class D felony, which includes thefts of more than $3,000 but less than $50,000.

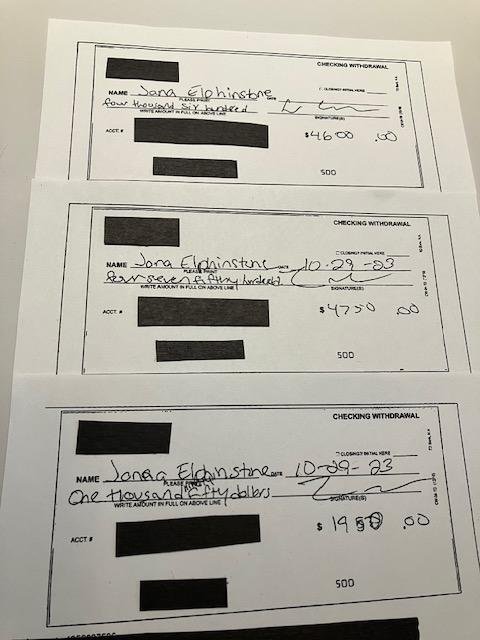

The bank also gave me copies of the withdrawal slips, which became critical evidence. The criminal made the withdrawals under my maiden name, albeit misspelled on each slip. It’s a name that hadn’t appeared on my checking account for well over a decade.

The slips also showed where the withdrawals occurred: three bank branches in south New Jersey — nowhere near New York City, where we bank regularly. That meant the perpetrator was likely captured on surveillance tape at the bank.

“I’m sure that played into their increased willingness to give you the report,” Velasquez said of the police, “and to make that a priority.”

Getting that report was more than many fraud victims receive. But five months later we still don’t know how this happened or who did it.

A detective assigned to the case told me about a month ago that the police department was working on issuing a subpoena for the security cameras in the bank branches. When I visited the precinct on Friday for another update, the detective was in court and unavailable.

“We need more streamlined processes so that people know where to start,” Velasquez said, “and they don’t have to relive this nightmare over and over.”

It’s a nightmare that more and more people are forced to face. Almost 7 in 10 people said they had previously been the victim of an identity crime, according to a general population survey of 1,048 people that ITRC conducted last year.

A survey of 144 ID theft victims who reached out to the nonprofit in 2022 found that almost two-thirds said their issues were still unresolved months after discovering the fraud.

The lasting impact of identity fraud

Like so many things in life, the impact of identity fraud often depends on the resources available to you.

“Some people will look at a $100 loss and go, ‘That sucks, but it’s not that big of a deal’… and other people will say, ‘This is going to derail everything, that was all that I had left after I paid my bills to buy groceries. I can’t feed my family. I can’t keep the lights on,'” said Velasquez, the ITRC CEO.

We were fortunate. We had a financial cushion to fall back on if we had not gotten our money back as quickly as we did.

Still, we encountered hassles. We spent the next weeks getting late fees and interest charges waived because some bill payments were denied. We also had to scramble to make sure a maturing CD was deposited into the new checking account, rather than the old one.

But the financial fallout was largely limited.

That’s not how it always is for many people who have their credit histories ruined, loans denied, and employment opportunities lost due to the lingering effects of fraud. After all, the type of fraud I experienced cost 15 million Americans $24 billion in losses in 2021, according to Javelin’s latest data.

And there’s the emotional side, too. For me, it’s unnerving to think that someone is walking around impersonating me. Could it happen again? Possibly.

The ID theft victims ITRC surveyed often reported feeling violated and having trust issues — and 16% considered suicide, up by double since 2021.

“The emotional impacts are increasing,” Velasquez said. “People are feeling even more vulnerable and unable to recover.”

Janna Herron is a Senior Columnist at Yahoo Finance. Follow her on Twitter @JannaHerron.