Mastercard is a stock that can continue to beat the market for decades.

Al Gore, the former U.S. vice president, co-founded Generation Investment Management in 2004. Today, the firm manages nearly $50 billion, all of which is directed to investments that the firm believes won’t destroy the planet. So-called sustainable investments, the firm believes, have the potential to outperform the market over the long term.

There is some proof for this belief. Data from Morgan Stanley shows that investment funds focused on sustainable investments have outperformed traditional funds in four out of the past five years.

Where is Al Gore’s investment firm putting money to work today? One of its biggest investments — a stake worth roughly $560 million — is in a company nearly everyone knows well: Mastercard (MA -0.18%).

Mastercard is a rocket stock

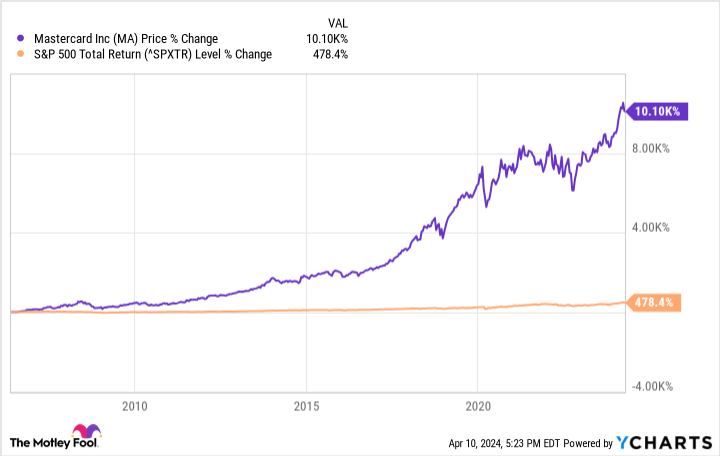

It’s not hard to understand why long-term investors like Al Gore love Mastercard stock. Just pull up a chart of the company’s stock price. During the past two decades, Mastercard stock has risen more than 10,000% in value. The S&P 500, in comparison, delivered a return of just 478% over the same period.

This performance is no fluke. Mastercard has outperformed the S&P 500 over the last one-year, five-year, and 10-year periods, too. It’s a rocket of a stock that keeps rising and rising.

Of course, what investors should really be interested in is why Mastercard keeps outperforming the market.

Look for winning stocks like this

In the final quarter of 2006, $308 billion worth of transactions were processed using Mastercard credit cards. In 2010, total payment volume reached $427 billion. Five years later, payment volume nearly hit $600 billion. Last quarter, it surpassed $1 trillion. The only years in which Mastercard experienced declining payment volumes were during the 2009 recession and the 2020 pandemic. Very soon after those events, however, payment volumes recovered to reach all-time highs.

Because Mastercard’s profit is largely a function of how much people use its cards, a consistent rise in payment volume results in a consistent rise in net income. Earnings per share have hit record highs nearly every year, while profit margins have expanded to between 40% and 50%. In all, Mastercard is a growing, highly profitable business that can weather recessions with relative ease.

High levels of profitability are the result of an asset-light business model. It doesn’t take a ton of equipment or machinery to run Mastercard’s payment network. It mainly runs on software that can quickly accommodate rising volume with little additional capital spending. That naturally results in a sustainable business model. According to Morningstar‘s Sustainalytics rating system — which quantifies how eco-friendly a company is — Mastercard scores in the top 15% of all publicly traded companies. No wonder Al Gore’s firm is heavily invested.

MA Profit Margin data by YCharts

An asset-light business model has produced high profit margins for Mastercard, but it is network effects that have driven consistent growth over the decades. Network effects describe how a business gains value as it becomes larger. Think of every credit card provider you know of right now, and there’s a good chance that you’ll only be able to name Mastercard, Visa, American Express, and Discover. That’s because these four companies control nearly 100% of the U.S. market.

There’s good reason for this industry consolidation. Mainly, there’s benefit to scale. The larger a payment network becomes, the better it works. Industry consolidation, therefore, is a natural feature of the payments industry. It’s possible to get around these networks, but that comes at the cost of access. Customers and merchants want to use payment networks that they know both parties can use and trust. There’s little reason to have dozens of redundant payment networks providing the same service.

In this way, Mastercard is the ultimate network effects business. Its network is huge, only rivaled by Visa’s. This scale only begets more scale, making it ever more difficult for competitors to emerge. And because it is an asset-light business, the company can scale efficiently — a big reason profit margins continue to rise.

Gore’s firm has owned Mastercard stock since the second quarter of 2022. Don’t be surprised to still see it in the portfolio many years down the road.

Discover Financial Services is an advertising partner of The Ascent, a Motley Fool company. American Express is an advertising partner of The Ascent, a Motley Fool company. Ryan Vanzo has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Mastercard and Visa. The Motley Fool recommends Discover Financial Services and recommends the following options: long January 2025 $370 calls on Mastercard and short January 2025 $380 calls on Mastercard. The Motley Fool has a disclosure policy.