Chris Stevens and Toby Goodworth examine whether the hedge fund sector can drive positive action in the climate transition.

Climate change is evident everywhere, from raging wildfires to alarming sea temperature anomalies. Consequently, investors are keenly focusing on the climate transition theme within their portfolios. Initially, this attention was centred on equities and fixed income but, of late, the spotlight has moved towards alternative investments, including hedge funds – also known as ‘liquid alternatives’. So, is the hedge fund sector ready to meet the challenges posed by clients and the real effects of climate change itself across capital markets?

Equity long/short (L/S) hedge funds, which constitute a significant proportion of the hedge fund universe, are somewhat ahead of their alternatives counterparts. This is primarily because the origins of ‘ESG investing’ lie in the traditional long-only equity world, and climate change has long been the dominant part of the ‘E’ in ESG. As such, the data and analytic techniques developed for traditional equity investing are adaptable into the equity L/S space.

There are nuances, of course. Short positions have often been the subject of debates around the existence or otherwise of ‘real-world impact’ (by increasing a firm’s cost of capital or management pressure). There has also been debate around how to account for short positions in determining portfolio-level metrics, such as carbon intensity.

Aside from these debates, which apply broadly across the alternatives sector, the sector has seen the emergence of a small number of dedicated climate-focused equity long/short strategies. These approaches place climate transition at the centre of their investment processes and seek to invest long or short, depending on whether companies are likely to be advantaged or otherwise from the changes brought about by the move to a lower-carbon future.

Other areas of the hedge fund world are also responding. There’s a growing trend to incorporate the climate transition theme in credit hedge funds (along similar lines to equity strategies), macro (considering impacts at broad asset class or sector levels), and multi-strategy funds (a combination).

Alternatives managers have also explored this theme in portfolios via ‘green securities’ such as green bonds or ESG equity futures, but carbon markets have also emerged as an area where hedge funds can meet the climate issue. Carbon markets allow investors to access alternative return streams directly connected to the climate transition. These markets are gaining traction as regulations establish ‘emissions trading systems’ across different regions and liquidity improves.

Multi-strategy funds and managed futures/CTA managers have been some of the first alternative strategies to access these markets, albeit typically only as a minority part of their portfolios. A small number of dedicated carbon trading strategies have also emerged. Such strategies tend to have a long bias towards the asset class, anticipating a rise in carbon prices and trying to contribute to that increase, whilst also seeking alpha opportunities from active trading of exposures. Investors seeking real world impact from their alternatives strategies may find these approaches to be attractive propositions.

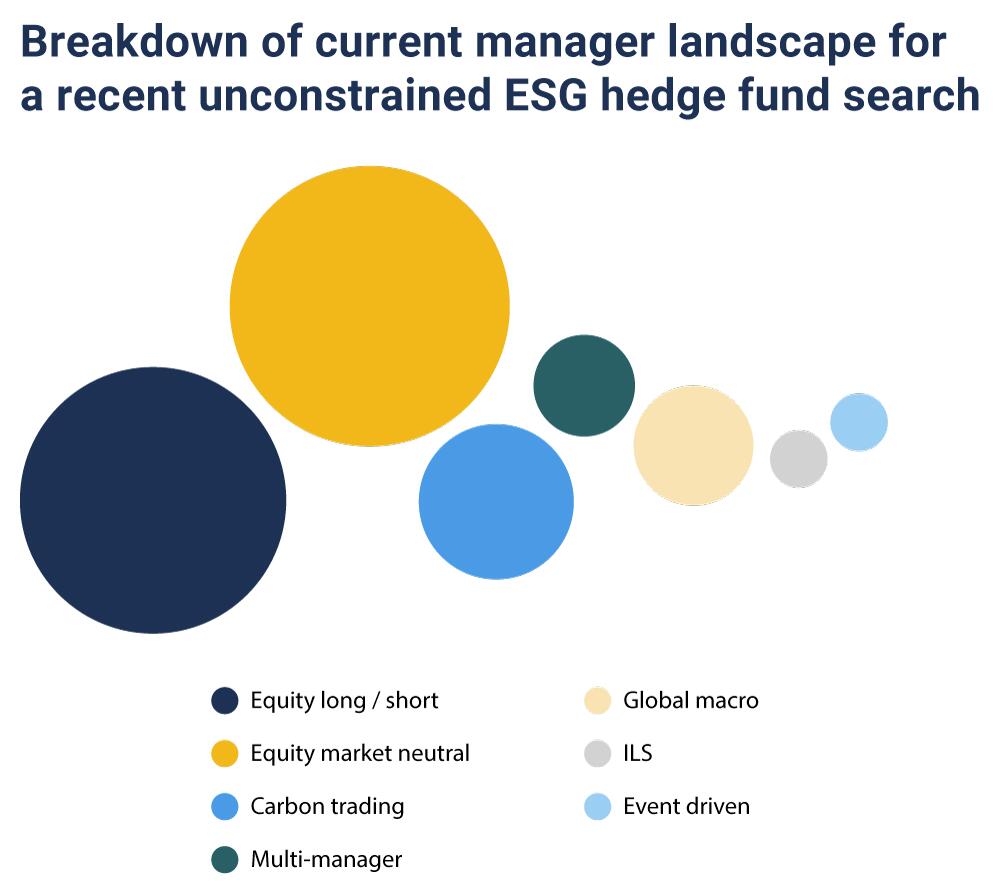

There are some fundamental issues facing hedge fund investors who wish to focus on the climate issue. Typically, investors will place minimum track record and asset level requirements on managers and, as we have seen, most strategies in this sector are new and therefore smaller in assets – and often managed by specialist boutiques. In a recent search we conducted for ESG-oriented hedge fund strategies, the median track record length was just 38 months with median fund assets under management of ~$140 million.

This brings the dilemma of reducing requirements, and facing the increased due diligence needed for ‘early-stage’ managers without lengthy track records, or not reducing those requirements and facing the risk of being exposed to managers greenwashing previously existing products which historically were not climate orientated.

Finally, there is also the issue of portfolio construction for climate-focused investors. As investors pay more attention to climate transition risks and opportunities across all parts of their portfolios, there is a need to be wary of concentration in a ‘climate factor’ – which could perhaps be proxied by a trade such as ‘long renewable energy, short oil and gas’. While this position may well be rewarded over the long-term, investors should be deliberate about risk-taking. On the hedge fund side, risks like this can be managed through techniques such as sector neutrality – but as ever, the focus should be on finding diverse sources of risk and return to the benefit of the portfolio as a whole.

Chris Stevens is senior director within the diversifying strategies team at bfinance

Toby Goodworth is head of liquid markets at bfinance