The fight against climate change is gaining momentum among governments and consumers, with 92 per cent of global GDP now covered by net-zero targets. Yet these commitments cannot be met by behavioural change alone. Much will also depend on the deployment of existing technologies as well as the development of new ones. Adoption has been a problem. The penetration of cleantech is currently too low.

But there are grounds for optimism. The International Energy Agency estimates that most of the cleantech needed to achieve the world’s net-zero commitments by 2030 is already market-ready. Moreover, the environmental technologies market is forecast to more than double in size from USD4.9 trillion in 2020 to USD12.1 trillion by 2030.

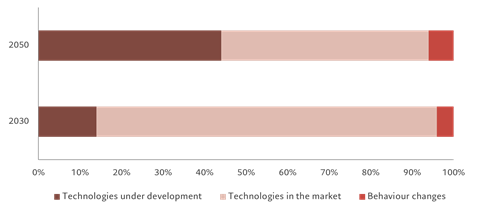

Fig. 1 – Powerful technologies

The proportion of the total emissions savings achieved through technologies (new and existing) and by behavioural change, %, relative to 2020

Yet for these technologies to reach their full potential, they still need significant investment. The Climate Policy Initiative calculates that, at a minimum, climate financing must increase by 590 per cent to meet the world’s declared climate objectives by 2030.

That’s a challenging target, but it presents a potentially rewarding opportunity for investors.

Investing in the transition

In our view, there are five key areas where this investment can have the greatest effect:

- Greenhouse gas reduction: batteries and storage; energy efficiency; low/no carbon and carbon removal technologies; as well as renewable energy technologies and services.

- Sustainable consumption: agri-tech; food safety; supply-chain optimisation; and food tech.

- Pollution control: water quality; air quality; soil preservation; and waste treatment.

- The circular economy: the sharing economy; recycling; resource efficiency; and bio-based materials.

- Enabling technologies: sensors and data capture; the semiconductor value chain; design and engineering software; and green chemistry.

These solutions are already attracting interest from investors, and we believe the opportunity is particularly compelling in private markets, not least because private companies are at the cutting edge of these technologies. Globally, the cumulative number of private environmental companies with a valuation above USD1 billion, firms known as unicorns, has increased 14-fold since 2017. This compares with an increase of only four times in the number of total unicorns over the same period.

Such a boom in valuations is not surprising given that private companies are taking the lead in many areas of environmental technology. For example, the efficiency record for converting the sun’s rays into electricity via a commercial-sized panel was set in May by a private European company. Private companies also include some of the largest players in the electric-vehicle value chain, as well as leaders in recycling lithium-ion batteries. Investors that have built stakes in firms operating in these sectors have enjoyed healthy returns.

The co-investment approach

Of course, investing in private companies is not without risks. That’s particularly the case for the environmental tech industry, where governments and regulators play an outsized role in shaping the competitive landscape.

However, there is one area within private equity (PE) which offers investors some degree of protection from such risks: co-investments. Through this structure, PE managers (known as general partners, or GPs) offer select investors (limited partners, LPs) the opportunity to invest directly alongside them in a specific transaction.

In the past two decades, co-investment funds have raised over USD175 billion. As PE continues to expand, we expect co-investments to grow too.

For GPs, the main benefit of co-investment is the ability to invest more in firms they consider attractive (GPs are often subject to concentration restrictions, limiting how much capital they themselves can invest in a single company.)

For LPs, meanwhile, one of the key advantages of co-investing is direct access to high quality private companies. Rather than investing in hundreds of firms through a fund-of-funds vehicle, a co-investment strategy is much more focused (typically in 25-30 companies) while retaining adequate diversification across GPs, countries and industries.

Another benefit is the fact that co-investments are deployed much more rapidly (usually over two to three years) than traditional PE funds of funds, which can take six to seven years to reach full investment. Earlier deployment can help mitigate the problem embodied by the J-curve, or the tendency for PE investments to report capital losses in the early years of their life before generating gains. This is borne out by our own 30 years’ experience of co-investing at Pictet.

Ultimately, the net return is boosted by the fact that GPs typically offer co-investments free of the usual management (1.5-2.0 per cent) and performance fees (20 per cent). This is significant in an asset class that tends to command considerably higher fees than listed assets.

We believe co-investment can thus be an attractive route to invest in private markets in general, and in environmental pioneers in particular.

Grounds for optimism

By funding innovation in the private sector, investors will have a major role to play in putting the world economy on a sustainable footing.

History testifies to this.

Forty years ago, one of the planet’s foremost environmental concerns was the hole growing in the ozone layer. Activism led to the 1989 Montreal Protocol on phasing out ozone-depleting substances, such as chlorofluorocarbons (CFCs), and then the wider Kyoto Protocol in 1997. Businesses, backed by investors, developed a host of alternatives to CFCs.

Today, stratospheric ozone levels are among the few of the nine Planetary Boundaries that humanity hasn’t breached.

“Technological innovation, supported by private finance, can help restore the planet and deliver healthy investment returns.”

Technological innovation, supported by private finance, can help restore the planet and deliver healthy investment returns.

You can now read the full whitepaper at the link below