Despite an already strong run, IRB Infrastructure Developers Limited (NSE:IRB) shares have been powering on, with a gain of 34% in the last thirty days. The annual gain comes to 155% following the latest surge, making investors sit up and take notice.

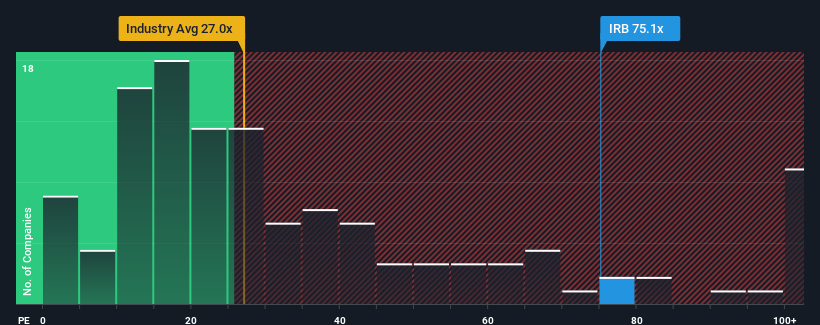

After such a large jump in price, IRB Infrastructure Developers’ price-to-earnings (or “P/E”) ratio of 75.1x might make it look like a strong sell right now compared to the market in India, where around half of the companies have P/E ratios below 31x and even P/E’s below 17x are quite common. Although, it’s not wise to just take the P/E at face value as there may be an explanation why it’s so lofty.

IRB Infrastructure Developers could be doing better as its earnings have been going backwards lately while most other companies have been seeing positive earnings growth. One possibility is that the P/E is high because investors think this poor earnings performance will turn the corner. If not, then existing shareholders may be extremely nervous about the viability of the share price.

See our latest analysis for IRB Infrastructure Developers

If you’d like to see what analysts are forecasting going forward, you should check out our free report on IRB Infrastructure Developers.

How Is IRB Infrastructure Developers’ Growth Trending?

The only time you’d be truly comfortable seeing a P/E as steep as IRB Infrastructure Developers’ is when the company’s growth is on track to outshine the market decidedly.

If we review the last year of earnings, dishearteningly the company’s profits fell to the tune of 29%. However, a few very strong years before that means that it was still able to grow EPS by an impressive 85% in total over the last three years. So we can start by confirming that the company has generally done a very good job of growing earnings over that time, even though it had some hiccups along the way.

Looking ahead now, EPS is anticipated to climb by 72% during the coming year according to the five analysts following the company. That’s shaping up to be materially higher than the 24% growth forecast for the broader market.

In light of this, it’s understandable that IRB Infrastructure Developers’ P/E sits above the majority of other companies. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Final Word

Shares in IRB Infrastructure Developers have built up some good momentum lately, which has really inflated its P/E. It’s argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

As we suspected, our examination of IRB Infrastructure Developers’ analyst forecasts revealed that its superior earnings outlook is contributing to its high P/E. At this stage investors feel the potential for a deterioration in earnings isn’t great enough to justify a lower P/E ratio. It’s hard to see the share price falling strongly in the near future under these circumstances.

It is also worth noting that we have found 4 warning signs for IRB Infrastructure Developers (2 are a bit concerning!) that you need to take into consideration.

If P/E ratios interest you, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Valuation is complex, but we’re helping make it simple.

Find out whether IRB Infrastructure Developers is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.