- “Paper vs. Physical: The Fractured Oil Market”

- “When Energy Meets Geopolitics: A Perfect Storm”

- “The Hidden Risks in America’s Power Infrastructure”

- No deal – The negotiation team could not agree on a forward path.

- Watch the Strait of Hormuz open by force.

- It is clear that the IRGC should not be trusted.

- President Trump ordered a blockade of any ships going through the Strait of Hormuz that paid for passage. This is better than putting troops on Kharg Island as sitting ducks.

Just talked to some great contacts, and President Trump is looking at some great executive orders coming in on Energy Security. Can’t talk about them right now, but we have interviews lined up to discuss them!

The discussion delves into the complexities of oil pricing, distinguishing between paper oil prices (futures contracts) and physical delivery prices. There’s significant focus on tanker traffic, oil flows to the U.S. and California, and analysis of energy-related ETFs and stock performance in the sector.

A major theme is the situation surrounding the Strait of Hormuz, a critical chokepoint for global oil supply. The conversation includes concerns about potential closure, Iran’s alleged inability to fully reopen it due to lost mine maps, and the potential involvement of U.S. military intervention. These geopolitical issues directly impact global energy markets and supply chains.

The transcript highlights serious vulnerabilities in America’s aging power grid, with a significant portion of transformers operating beyond their expected lifespan. There’s particular concern about the vulnerability of the 18 major grid interconnects to potential sabotage or cyberattacks.

Discussion includes the need to redefine how we calculate the levelized cost of energy, particularly to better account for renewable energy sources. There are also mentions of potential policy actions by the Trump administration regarding energy issues.

The transcript covers stock performance and investment opportunities in the energy sector, including major companies like Chevron and ExxonMobil, as well as how climate-focused and ESG investors are navigating market volatility.

1.The Paper Price of Oil is About to Get Hit with Reality and Converge with the Delivery Price of Oil

The New York Times dropped a bombshell on April 10, 2026, that reads like a dark comedy sketch from the Iranian Revolutionary Guard Corps (IRGC) playbook. According to U.S. officials cited in the report, Iran cannot fully reopen the Strait of Hormuz—the artery carrying roughly 20% of the world’s oil and a massive share of global LNG—because it literally cannot locate all the naval mines it scattered there just last month.

The IRGC laid the mines haphazardly from small boats in the chaotic early days of the U.S.-Israel war on Iran. No complete records were kept. Some mines drifted with the currents. And Tehran lacks the technical know-how or equipment to sweep them efficiently. Mine removal is always harder than laying them, and neither Iran nor even the U.S. Navy has a fast, robust demining force ready for this scale. The result? Iran’s own “technical limitations” (their euphemism for self-sabotage) are keeping shipping at a trickle despite a fragile ceasefire and President Trump’s repeated demands for full reopening.

This isn’t just embarrassing for Tehran. It is a self-inflicted chokehold on the global energy market at the worst possible time.

The Strait of Hormuz crisis, triggered by the February 28, 2026, U.S.-Israel strikes that killed Supreme Leader Ali Khamenei, has produced the largest energy disruption since the 1973 oil embargo. Here are the hard numbers as of early April 2026:

Oil shut-in and lost production: Roughly 9–10 million barrels per day (mbpd) of Gulf crude production has been curtailed or shut in. That’s more than 10% of the global supply. Saudi Arabia, UAE, Iraq, Kuwait, and others have run out of onshore and floating storage. Fields like Iraq’s Rumaila and Saudi offshore sites were throttled hard. Traffic through the strait is down over 90% (a few ships per day versus the normal ~140).

Oil in tankers in the Persian Gulf: Over 230 loaded oil tankers are idling inside the Gulf right now, holding tens of millions of barrels that cannot move. Hundreds more vessels (estimates range from 325–600+ tankers and support ships) are stranded or rerouted, creating a floating parking lot the size of a small country.

LNG on tankers and lost exports: Zero loaded LNG carriers have successfully transited the strait in weeks. Qatar—the world’s largest LNG exporter—shut production after strikes damaged facilities (some capacity offline for 3–5 years). Dozens of Qatari LNG tankers (50+ reported idle across Asia and the Gulf) sit waiting. Global LNG prices have spiked, forcing Europe and Asia toward coal and rationing.

Broader loss: Combined oil and LNG flows normally exceed 20 mbpd equivalent. The backup has already pushed Brent futures into the $90–$100 range (with physical/spot prices even higher, around $120+ at times), sent European gas prices soaring, and triggered force majeure declarations across the Gulf. Restarting production—even if the strait magically cleared tomorrow—will take weeks to months because of damaged infrastructure, storage limits, and the massive tanker backlog.

In short, the world is staring down a manufactured shortage that Iran helped create and now cannot undo.

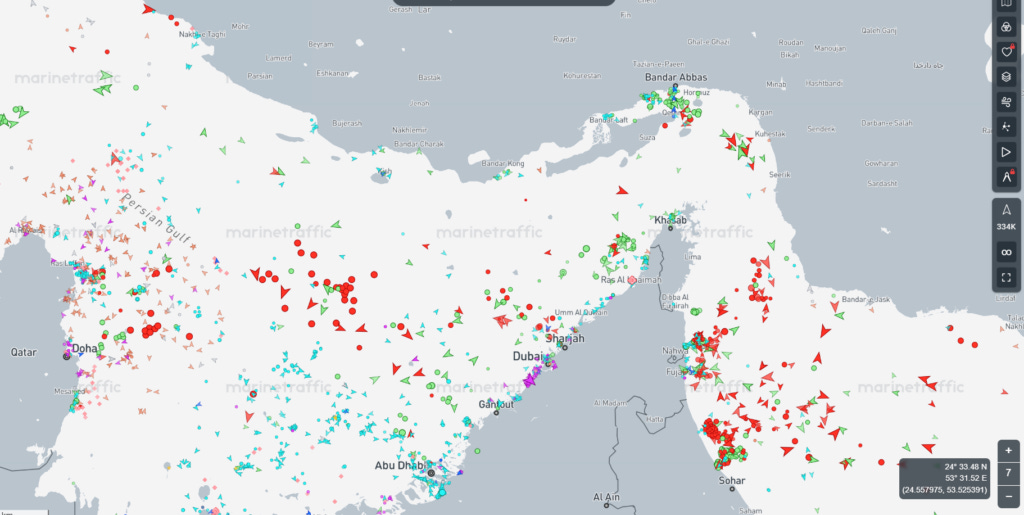

At the time of writing this article, several tankers are passing through the Strait of Hormuz, close to the Iranian side, surrounded by “support” ships. So we also do not have a confirmation that they are paying or not paying a toll.

Today’s High-Stakes Talks in Pakistan

U.S. and Iranian delegations are meeting right now in Islamabad, Pakistan—the first high-level face-to-face since 1979. Pakistan’s Prime Minister called them “make or break.” The U.S. side, reportedly led by Vice President JD Vance, wants the strait open immediately. Iran wants sanctions relief and a permanent end to the war. The mines problem is now a major complicating factor at the table.

Scenario 1: Deal is reached, but mine-clearing takes 30 days

A negotiated agreement emerges from Pakistan. Iran allows limited safe corridors and accepts international (likely U.S.-led) help sweeping mines. Cleaning the strait realistically takes at least 30 days, given the drifting mines and limited equipment. Oil price impact: Prices stay elevated for 4–8 weeks while the backlog clears and damaged fields ramp back up. Brent could ease from current levels toward $80–$90 as supply trickles back, but physical tightness and risk premium keep spot prices higher longer. Global recession risk moderates, but energy inflation lingers into summer. Restart lags mean full normalization takes 3–5 months.

Scenario 2: No deal—Trump follows through on strikes

Talks collapse. President Trump makes good on his threat to “decimate every bridge in Iran” and turn power plants into “burning, exploding” ruins. Iran’s roughly 3.4 mbpd of crude production (plus associated gas and export infrastructure) goes offline indefinitely. The strait remains contested or mined, and the broader Gulf faces new escalation risks. Oil price impact: Catastrophic. Losing another 3.4 mbpd on top of the existing 9–10 mbpd shut-in pushes total disruption toward 15%+ of global supply. Brent futures could spike to $120–$150+/bbl or higher in a panic, with physical cargoes even pricier. Recession odds skyrocket. Strategic reserves (already tapped) buy only weeks of relief. Asia’s importers (China, India, Japan) face rationing; Europe’s gas crisis deepens. This scenario turns a severe disruption into a multi-year energy shock.

The NYT story exposes Iran’s strategic blunder: it booby-trapped the world’s most important oil lane and then lost the map. Whether the Pakistan talks produce a face-saving deal or collapse into Trump’s promised infrastructure apocalypse, one thing is certain—the world’s oil and LNG markets will remain volatile for months. Energy investors, policymakers, and consumers should brace for higher prices and supply uncertainty well into 2026 and beyond.The mines are still out there. So is the crisis.

3.U.S. Begins Clearing the Strait of Hormuz with Military Ships Passing Through

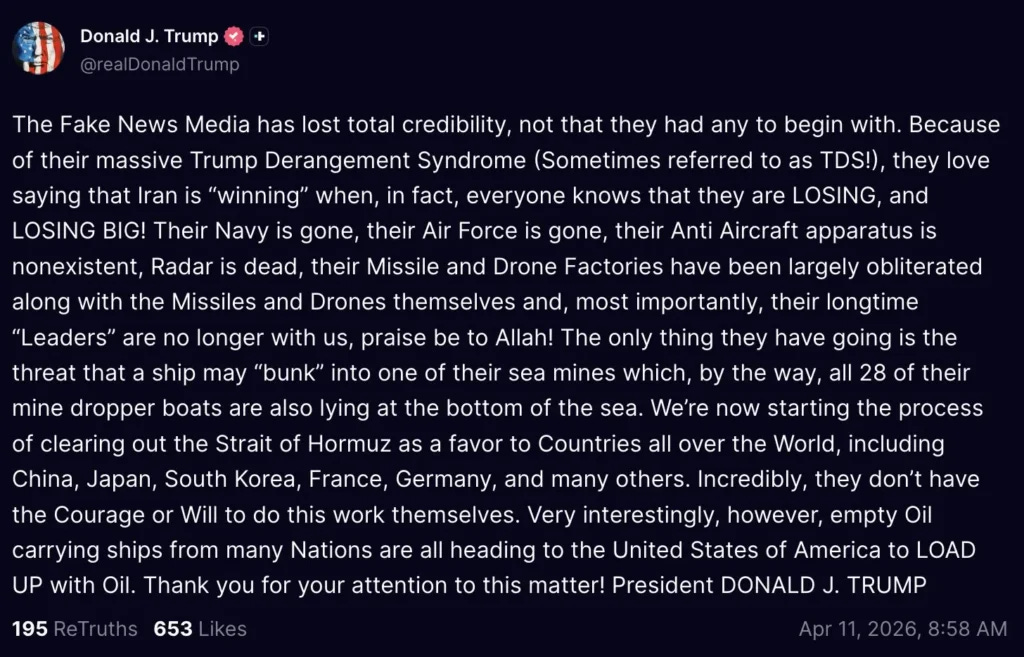

In a significant development for global energy security, the United States has initiated military operations to clear and secure the Strait of Hormuz, with U.S. Navy vessels now transiting the critical waterway amid ongoing tensions with Iran. This move comes as commercial shipping traffic remains a fraction of normal levels despite a fragile two-week ceasefire, and as high-stakes peace talks between the U.S. and Iran open in Pakistan.

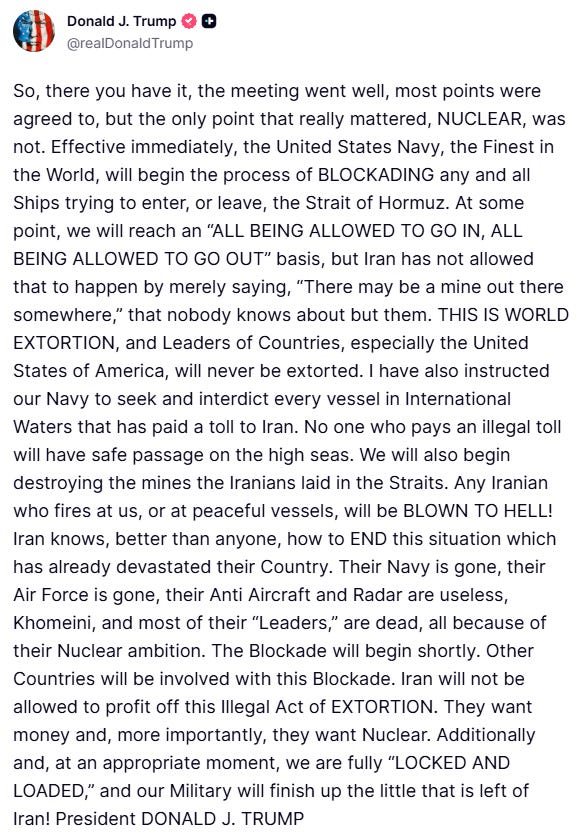

President Donald Trump addressed the situation directly on Truth Social, announcing that the U.S. is “starting the process of clearing out the Strait of Hormuz” as a service to global markets and energy-dependent nations. In the post, Trump highlighted that Iran’s minelaying capabilities have been degraded (with reports of 28 vessels sunk or neutralized) and emphasized that U.S. military ships, aircraft, and personnel will remain in position until full, safe, and unrestricted access is restored. He reiterated that any deviation from the ceasefire agreement—such as continued tolls or restrictions—would trigger stronger action, stating, “If they are [charging fees], they better stop now!” and warning that “the ‘Shootin’ Starts’” otherwise.

4.$2B Investment Drives Expansion of U.S.-Canada Oil Flows

5.TAL Pipeline Connecting Germany and Italy May Have Been Sabotaged

6.Iran War Fuels Rush to Energy ETFs and Oil Stocks. Climate Investors See No Reason to Chase Returns

7.Europe’s Gas Market is under Stress During Refill Season

8.The US Grid Transformers are a Critical Junction and Is A National Security Risk

This is a huge problem.

The backbone of America’s electricity system is under unprecedented strain. As highlighted in a widely discussed analysis by investor Felix Prehn, roughly half of the nation’s power transformers are operating well past their useful life—not merely aging, but “running on borrowed time.” JP Morgan has flagged the U.S. power grid itself as a national security risk. With AI-driven data centers, electric vehicles, and widespread electrification pushing electricity demand to new highs, the humble transformer has become one of the most critical bottlenecks in the energy transition.

The U.S. electric grid relies on an enormous fleet of transformers. Estimates place the total number of in-service distribution transformers at 60–80 million units. Approximately 55% of these are already more than 33 years old, approaching or exceeding their typical 30–40-year design life. Failure rates are expected to accelerate sharply after 2030.

Large power transformers (including generator step-up and substation units) number in the thousands rather than millions, but they are equally strained. Demand for these high-voltage units has surged 116–119% since 2019, while distribution transformer demand is up 34–41%. Two-thirds of transmission lines are over 25 years old, many built before the internet era.

Lead times tell the story: large power transformers can take 3–5 years to procure, with some generator step-up units averaging 128–144 weeks. In 2025 alone, the U.S. faced projected shortfalls of 30% for power transformers and 10% for distribution units, forcing heavy reliance on imports (historically covering up to 80% of large power transformer demand).

Electricity consumption is accelerating faster than many forecasts anticipated. Data centers (largely AI-related) already consume 3–4% of U.S. grid capacity and are projected to reach 10% by 2028. Nearly half of the planned data centers opening this year have been delayed or canceled—not for lack of capital, but because there simply isn’t enough reliable power or grid infrastructure ready.

Additional pressures come from electric vehicles, heat pumps, battery storage, and renewable integration. The National Renewable Energy Laboratory projects transformer capacity requirements could rise by up to 260% by 2050 to support electrification goals.

Overall, U.S. electricity demand could be 14–19% higher by 2030 and 27–39% higher by 2035 compared with 2021 levels.

President Trump’s recent executive actions—declaring a national energy emergency and directing AI data center operators to develop their own on-site power generation (gas turbines, solar, batteries, microgrids)—underscore the urgency. The grid built for the Eisenhower era simply cannot support the AI buildout without massive upgrades.

Utilities and grid operators are responding with historic spending. U.S. electric companies are projected to invest nearly $208 billion in the power grid in 2025 alone, with more than $1.1 trillion expected over the next five years and roughly $1 trillion through 2035. The Department of Energy has allocated billions in targeted funding, including a recent $1.9 billion opportunity for accelerated transmission upgrades.

Every dollar flows through transformers, switchgear, conductors, and the contractors who install them. Backlogs remain stubborn despite new capacity coming online.

Major players dominating the U.S. market include: GE Vernova (GEV), Eaton (ETN), Hubbell (HUBB), Siemens Energy, Hitachi Energy (formerly ABB), Schneider Electric, and Prolec GE.

Pure-play U.S.-owned leaders such as Virginia Transformer Corporation (the largest domestically owned manufacturer), ELSCO Transformers, Maddox Industrial Transformer, and others focused on custom and medium-voltage units.

These companies enjoy multi-year order books. Five-year lead times translate into locked-in revenue visibility for the foreseeable future.

Progress is being made. Manufacturers have announced billions in new U.S. factory investments: Hitachi Energy’s Virginia plant expansion, Siemens’ North Carolina facility, Eaton’s $340 million commitment to three-phase transformer capacity, and others. Domestic production of certain distribution transformers has improved, and policy support (including tariffs and incentives) aims to reduce reliance on foreign supply.

Yet challenges remain. Critical components like grain-oriented electrical steel (GOES) still have limited U.S. capacity. Imports continue to fill much of the gap for large power transformers, and full reshoring will take years. Lead times, while slightly better for some distribution units, remain multi-year for high-voltage equipment.

A parallel risk looms in the supply chain. Investigations dating back years (including Sandia National Laboratories analysis) have identified hardware backdoors in certain Chinese-manufactured large power transformers that are capable of remote disablement from overseas. While utilities have largely curtailed new purchases of Chinese large transformers due to these risks, legacy units may still exist in parts of the grid.

More recent and widespread concerns center on solar inverters and related power electronics. Approximately 85% of U.S. utilities surveyed use inverters assembled by companies tied to the Chinese government or military. Rogue communication devices—“kill switches”—have been discovered in Chinese-made inverters deployed at U.S. solar farms. These could potentially allow remote shutdown or manipulation, bypassing firewalls and destabilizing portions of the grid. Cybersecurity experts warn that this represents a built-in vulnerability that could be weaponized during a conflict.

As of 2025–2026 reporting, these devices remain in widespread use across solar installations. Federal efforts to map and mitigate foreign-origin components continue, but full replacement will be costly and time-consuming.

Transformers may not make headlines like the latest AI model, but they are the literal junction where electrons meet demand. The convergence of aging infrastructure, exploding load growth, and geopolitical supply-chain risks has turned the U.S. grid transformer market into one of the most strategically important industrial sectors of the decade. The trillion-dollar investment wave is no longer optional—it is existential for reliability, economic competitiveness, and national security.

Whether through domestic manufacturing resurgence, accelerated permitting, on-site generation mandates, or targeted replacement of high-risk foreign components, the decisions made at this critical junction will shape American energy security for the next half-century.

A shout-out to Steve Reese and the Reese Energy Consulting group for sponsoring the Podcast https://reeseenergyconsulting.com/.

A shout-out to our New Sponsor, Data2 – We will be running an AI Centered Series and have lots of data rolling out!. https://www.data2.ai/resources/the-decision-lag-report

And we have WellDatabase rolling in as a new sponsor.