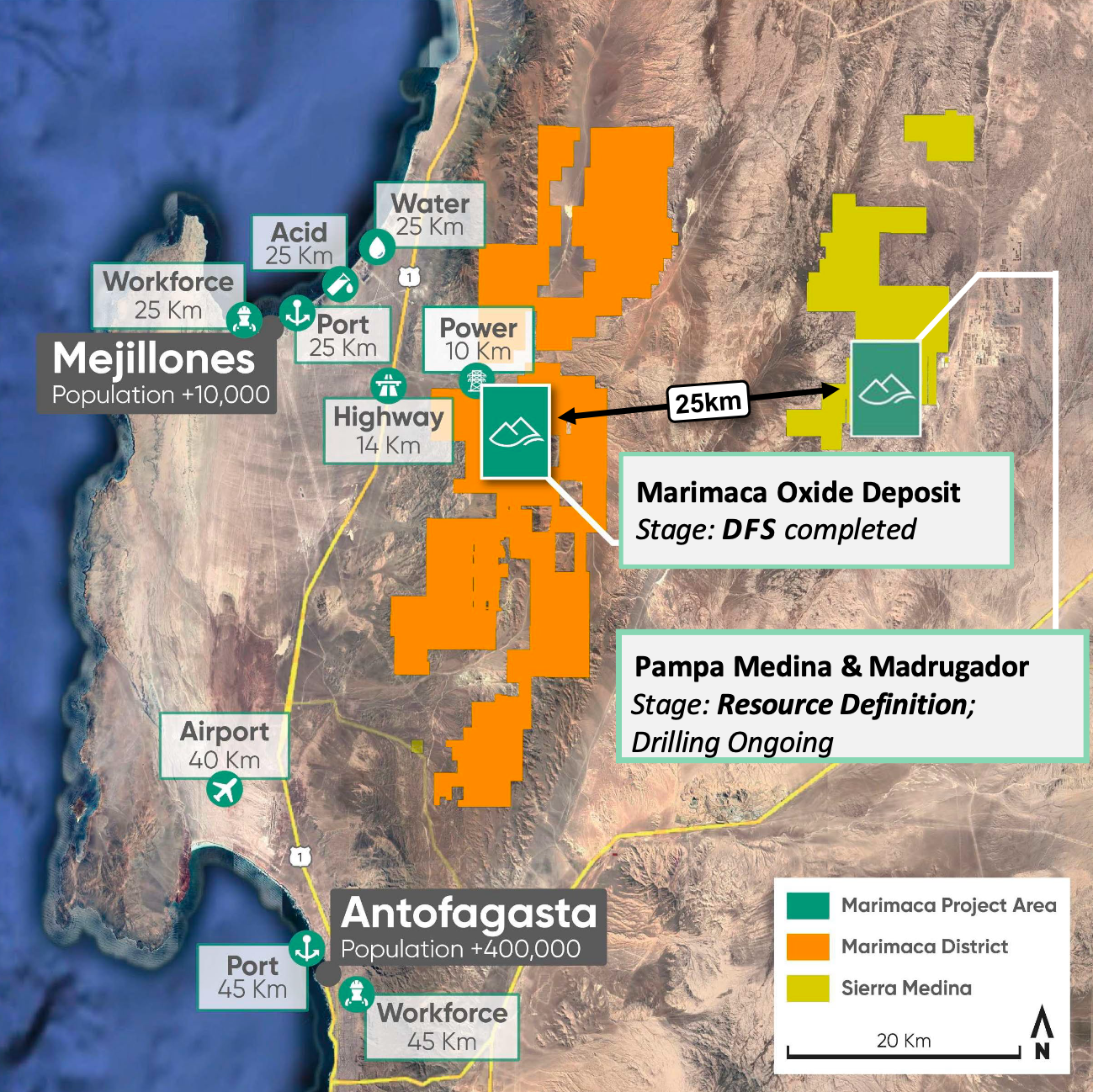

- Marimaca Copper is advancing detailed design and engineering for its flagship oxide deposit with an initial pre-production capital expenditure (capex) of US$587 million.

- Recent step-out drill results at the Pampa Medina target, located 25 kilometres from the planned processing infrastructure, have intersected broad zones of sediment-hosted copper mineralisation containing significant silver grades.

- The silver grades introduce an additional variable that may become economically relevant if future drilling establishes continuity and recoverability within a larger development scenario.

- Management is actively reviewing financing structures to fund the 2026 construction start while seeking to minimise equity dilution for existing shareholders.

- Precious metal by-products like silver can surface exceptional value for mine builders, potentially providing alternative financing avenues to offset construction costs.

What Has Happened

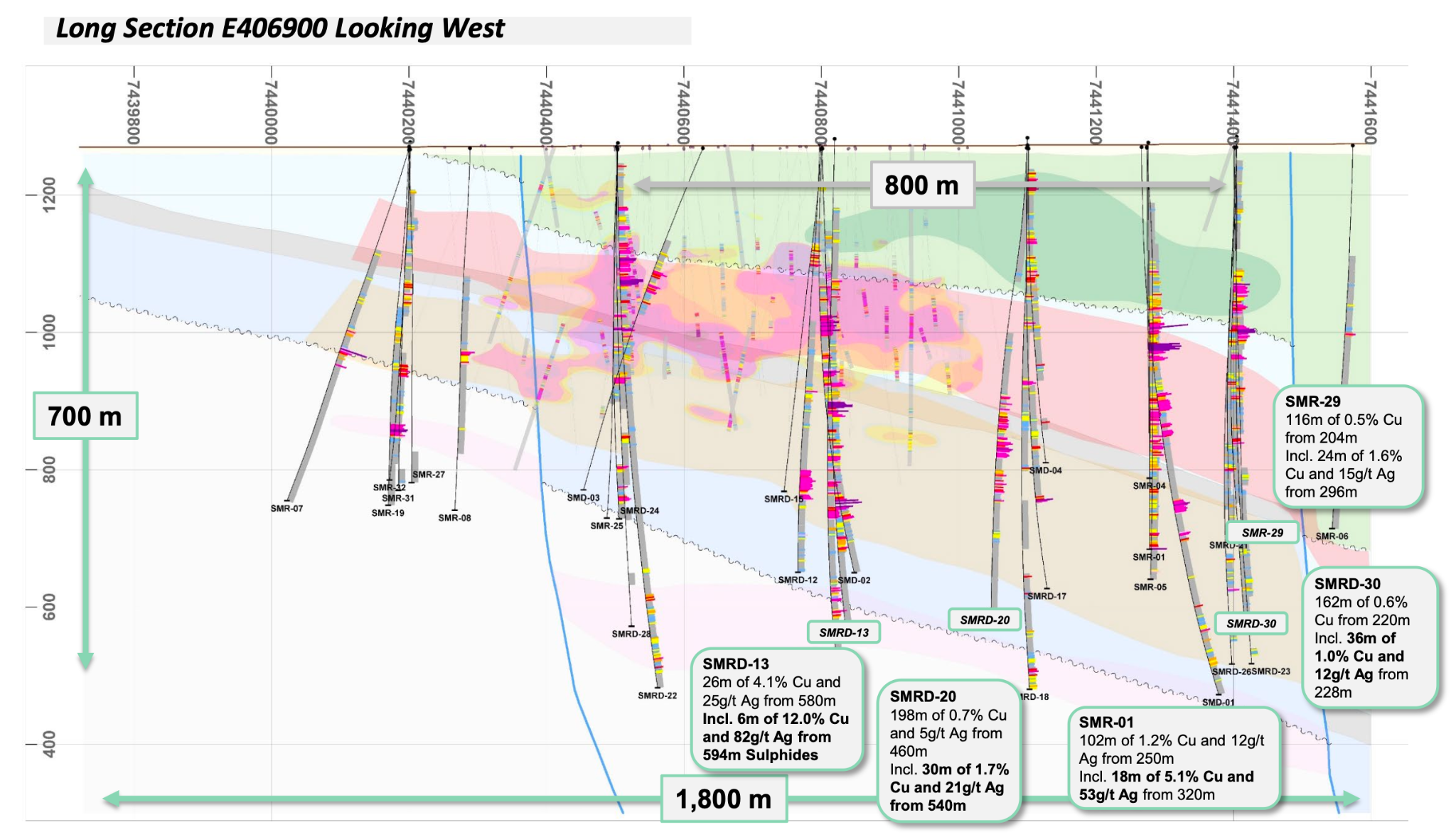

Marimaca Copper (TSX: MARI; ASX: MC2) has released step-out drilling results from its Pampa Medina target, located 25 kilometres from the planned processing infrastructure for the flagship Marimaca Oxide Deposit (MOD) in the Antofagasta Region of Chile. While the ongoing 30,000-metre drill program is primarily designed to confirm a large-scale, sediment-hosted copper system, the assay results have consistently revealed significant silver mineralisation alongside the copper. Intercepts from the high-grade corridor include 100 metres at 1.28% copper and 6.9 grams per tonne silver from 580 metres depth, which features a higher-grade internal zone of 6 metres at 12% copper and 82 grams per tonne

These results carry implications that extend beyond geological continuity. As Marimaca Copper advances toward a final investment decision (FID) for a US$587 million mine build at the MOD, the presence of silver mineralisation at a regional satellite target introduces a potential source of future financing flexibility. In large-scale copper developments, precious metal by-products can influence both long-term operating economics and the range of non-dilutive funding structures available to developers seeking to minimise equity dilution.

The Cost of Building in a High-Inflation Market

The definitive feasibility study (DFS) for the MOD outlines a highly competitive project with an initial US$587 million capex. At steady state, the mine is projected to produce 50,000 tonnes of copper cathode annually, translating to an industry-leading capital intensity of US$11,700 per tonne of copper production capacity. Despite this capital efficiency relative to global peers, raising over half a billion dollars remains a significant challenge for any single-asset developer in the current inflationary environment.

To mitigate execution risk, the company is dedicating the course of 2026 to detailed design and engineering. The goal is to mature the project to a level that prevents the cost overruns frequently seen when developers rush into construction. A longer engineering runway also provides the executive team with more time to evaluate various tranches of debt, equity, and alternative financing, with the explicit goal of securing a capital structure that minimises equity dilution for existing shareholders.

How Silver Could Lower Future Operating Costs

In large-scale copper mining, precious metal by-products like silver serve a specific financial function: they generate secondary revenue that can be credited against the operating costs of the primary metal. The DFS for the MOD already models a robust operation, featuring a second-quartile C1 cash cost of US$1.69 per pound of copper and an all-in sustaining cost (AISC) of US$2.09 per pound at steady state.

If Pampa Medina is eventually integrated into a broader production scenario, silver revenues could be credited against operating costs, potentially lowering the effective cost per pound of copper. This margin expansion would provide an additional buffer against copper price volatility and broader cost inflation. The extent of this benefit depends on factors that remain undefined at this stage, including silver recovery rates, future resource definition, and whether Pampa Medina ultimately enters a mine plan.

The drill results suggest that the silver is not confined to narrow, high-grade veins but is present throughout the deposit and broadly correlates with the copper mineralisation. Intercepts such as 198 metres at 0.65% copper and 5.1 grams per tonne silver from 460 metres indicate that mining at scale could yield a consistent stream of precious metals alongside copper cathode production, although recoverability and economic contribution will require further technical work to establish.

How Silver Could Affect Construction Financing

Beyond their impact on operating margins, precious metal by-products in large primary copper deposits can unlock exceptional value for mine builders and operators through alternative financing transactions, as management has noted in reference to recent and past sector transactions. For a company advancing a US$587 million capex project, the presence of a silver by-product at a satellite target opens the possibility of accessing additional financing avenues without expanding the share registry.

Pampa Medina remains in an early exploration stage: no resource has been defined, no metallurgical work on silver recovery has been completed, and no economic study incorporating silver has been published. The presence of consistent silver mineralisation introduces the type of precious metal exposure that financiers typically evaluate in large copper districts, although the pathway from exploration intercept to a financeable by-product depends on the outcomes of ongoing drilling and future technical studies.

In practice, a defined silver resource within an integrated district can provide lenders with additional collateral comfort when structuring financing packages for a primary development, broadening the range of terms available to the developer. Whether that pathway becomes available to Marimaca Copper depends on the technical milestones ahead.

Prioritising Operability & Capital Discipline

The integration of new assets and alternative financing tools must align with the company’s broader philosophy of capital discipline. Marimaca Copper has actively pushed back against market pressure to rush the project into production, prioritising a de-risked, operable mine design over speed. This deliberate approach extends to how the engineering team evaluates potential cost reductions. Any reduction in upfront capex must be assessed within the context of its broader impact on project risk and long-term operational reliability.

Chief Executive Officer of Marimaca Copper, Hayden Locke, commented on the balance between capital efficiency and operability:

“We do want to reduce capex, but every single design change that we make that reduces capex has to be thought about within the greater impact on risk of the project, and that’s around operability.”

What to Watch Next

The ongoing 30,000-metre drill program at Pampa Medina will remain central to defining the scale and continuity of the copper-silver system. Future results are expected to clarify whether the silver mineralisation can evolve into a sufficiently defined by-product opportunity within the broader district development strategy. Additional milestones may include silver-focused metallurgical testwork, as Marimaca Copper has not yet completed Phase I metallurgy programs at Pampa Medina. Such work would represent an important step toward evaluating potential silver recoveries and future monetisation pathways.

Beyond exploration, the company continues advancing detailed engineering for the MOD ahead of a targeted FID. As the project matures, market attention will increasingly shift toward updates to the financing structure and whether alternative funding mechanisms tied to precious metal by-products emerge within the broader capital stack. Announcements related to long-lead equipment procurement will also be important indicators of construction readiness and schedule commitment.

FAQs (AI-Generated)