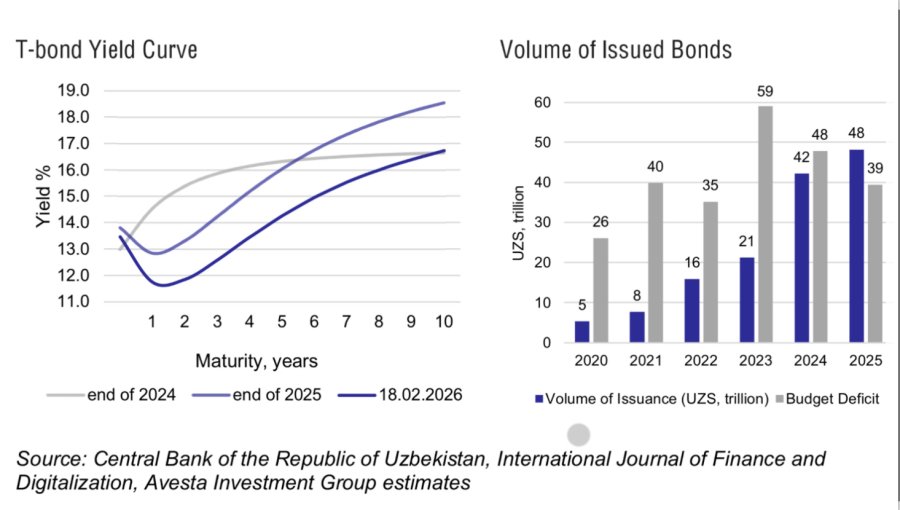

Uzbekistan has sharply stepped up its bond market activity. Issuance made by the Central Asian country doubled from UZS 21.3 trillion ($1.76bn) in 2023 to UZS 42.2 trillion ($3.50bn) in 2025, according to a report by Avesta Investment Group.

Tashkent has become increasingly reliant on local-currency borrowing to finance a widening fiscal deficit. It has reduced dependence on external debt while building a domestic yield curve, according to the analysis.

The development of the bond market activity is closely tied to monetary policy. The Central Bank of Uzbekistan (CBU) has alternated between tightening and easing cycles in recent years, raising the policy rate to 17% in 2022, before lowering it to 13.5% in 2023–2024 and then increasing it again to 14% in 2025 in a more cautious stance. Each shift has fed directly into bond pricing, influencing yields, investor appetite and issuance activity.

By 2025, the overall bond market had grown to around 6–7% of GDP, up from less than 3% in 2022. Government securities remain the dominant instrument, but demand is heavily concentrated among domestic banks, supported by zero-risk weighting, liquidity recognition and eligibility for central bank repo operations, anchoring primary market demand while limiting broader investor diversification, says Avesta.

The yield curve reflects an economy in transition. Short- and medium-term government bond yields have eased to roughly 11.5–13% in 2025–2026 as inflation expectations stabilise and policy credibility improves. However, longer-dated yields remain elevated at around 16.5–18.5%, reflecting persistent term and inflation risk priced in by investors.

The country’s strengthening external position has reinforced this trend. Uzbekistan’s international reserves rose from $34bn at the end of 2023 to about $66bn in 2025, with gold accounting for roughly 83% of holdings.

This has been bolstered by credit rating upgrades, with S&P Global Ratings and Fitch raising Uzbekistan to ‘BB’ with a stable outlook, while Moody’s maintained a ‘Ba3’ rating with a positive outlook, supporting investor confidence.

Investor appetite has also been evident in international markets, says Avesta. In February, Uzbekistan raised $1.5bn through a triple-tranche sovereign bond sale, attracting $4.2bn in orders.

The issuance included $500mn in seven-year dollar bonds at 6.95%, €500mn in four-year euro bonds at 5.1% and UZS 6 trillion ($497mn) in three-year local-currency bonds at 15.5%. These were priced below comparable 2024 issuances, when Uzbekistan sold $600mn in seven-year dollar bonds at around 6.9%, €600mn in euro bonds at about 5.375% and UZS 3 trillion ($249mn) in local-currency bonds at roughly 16.6%.

Part of the euro-denominated tranche was structured as green bonds, with proceeds earmarked for environmental projects such as water-saving technologies and waste management.

While sovereign borrowing dominates, the corporate segment has expanded rapidly from a low base. Outstanding corporate bonds reached a record UZS 5.28 trillion ($437mn) by February this year, more than doubling from UZS 2.2 trillion ($182mn) a year earlier.

The growth has been driven in part by regulatory changes allowing limited liability companies to issue bonds, with such entities now accounting for around 76% of issuers.

Microfinance institutions have been particularly active. By early 2026, 21 bond issues in the sector totalled UZS 431bn ($35.7mn), with individuals making up 98% of bondholders, a sign of rising retail participation in capital markets, notes Avesta.

Pricing, however, remains highly segmented. Corporate bond coupons vary widely depending on credit quality: microfinance institutions often pay up to 29%, mid-tier issuers typically offer yields in the 23–26% range, while banks and state-linked entities borrow at around 17–18%.

Tax incentives have also supported market growth. Interest income on corporate bonds is exempt from personal and corporate income tax until 2028, while interest payments are treated as deductible expenses for issuing companies, improving the attractiveness of bond financing.

Despite this growth, structural constraints remain. Secondary market liquidity is still limited and investor participation remains concentrated, even as reforms gradually expand access, Avesta advises.

Further reforms are in the pipeline. A December 2025 presidential decree paves the way for new trading platforms for foreign and foreign-currency bonds on the Tashkent Republican Stock Exchange, aimed at expanding the investor base and boosting liquidity.

If implemented effectively, these measures could deepen Uzbekistan’s capital markets and provide companies with an alternative to bank financing.