Editor: Mo Bell-Jacobs, J.D.

The tax information–reporting and withholding landscape is undergoing rapid transformation globally, driven primarily by changes in regulatory requirements, the increased use of digital assets, and the integration of artificial intelligence (AI) and automation. Recent legislation has added complexity, such as H.R. 1, P.L. 119–21, commonly referred to as the One Big Beautiful Bill Act (OBBBA), along with new global digital asset reporting rules, such as the Organisation for Economic Co–operation and Development’s (OECD’s) Crypto–Asset Reporting Framework (CARF) and the amended Common Reporting Standard (CRS). Meanwhile, the use of automation by taxing authorities around the world, such as the IRS, increases compliance and exam risk for taxpayers.

For organizations and professionals with oversight of tax reporting and withholding functions, these changes pose considerable challenges as well as opportunities. This item explores top considerations and challenges for navigating the emerging digital tax ecosphere and automating tax reporting functions.

Compliance and noncompliance: An overview of the issue and challenges

Tax reporting and withholding is part of the core compliance function for organizations making payments to U.S. and non–U.S. persons or entities. These processes require payers to determine the character and sourcing of payments, identify the tax status and residency of recipients, assign correct rates of withholding, collect and validate documentation, calculate and remit any taxes withheld, file information returns to taxing authorities, and furnish copies to recipients. Penalties for noncompliance can be significant and vary by jurisdiction.

Compliance with these requirements has historically involved overly manual processes that rely heavily on Excel spreadsheets and hard copies of documentation and generally present a host of challenges. Navigating these challenges presents risk, particularly for managing large volumes of data and transactions and ensuring the accuracy and timeliness of filings in an ever–evolving regulatory landscape.

AI’s effect on tax reporting functions

AI is reshaping the tax reporting and compliance function at companies around the world, particularly in the context of information reporting and withholding. AI–driven systems or agents are routinely ingesting, classifying, and reconciling large volumes of data; flagging payments as reportable or not reportable; and identifying potential compliance risks in real time.

There are exciting implications for complying with requirements for U.S. nonresident aliens, the Foreign Account Tax Compliance Act (FATCA), and backup withholding and reporting set forth under Chapters 3, 4, and 61 of the Code and the regulations thereunder. AI agents can be used to automate matching payee data in internal databases to tax withholding certificates provided by payees, to validate taxpayer identification numbers (TINs), and to perform complex withholding tax calculations involving reduced tax treaty rates. AI agents can also apply presumption rules in the absence of documentation, thus automating what were traditionally manual and time–consuming processes. Companies can also leverage AI to generate reports that can assist with tracking global reporting requirements, such as beneficial ownership reports and FATCA and CRS reporting deadlines, which vary by jurisdiction and are subject to change.

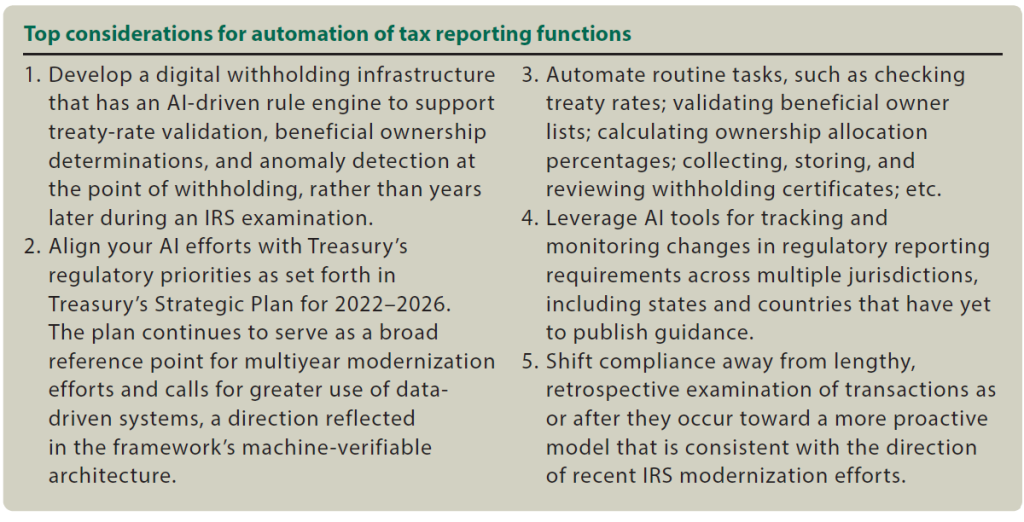

With the benefits of integrating AI into information–reporting processes comes a need for caution. AI models and agents are only as good as the data and logic they are built on and must be managed carefully. For example, if an AI system is not updated for the latest regulatory changes (such as new OBBBA thresholds for Form 1099 series reporting or new schemas for CRS reporting), it may misclassify transactions or fail to trigger required withholding when necessary, or it could produce misleading conclusions or results in a format that is not recognized by taxing authorities. Moreover, AI can introduce new risks, such as overreliance on automated determinations without sufficient human review or the propagation of errors at scale, which can be costly if an AI agent is deployed throughout an organization. Tax departments must ensure robust governance, including regular model validation, audit trails, and exceptional management processes (see the sidebar, “Top Considerations for Automation of Tax Reporting Functions,” below).

IRS use of automation and AI during examinations of information returns

The IRS is increasingly leveraging automation and AI in its examinations of information returns. The agency’s use of data analytics allows it to cross–reference information returns (Form 1099 series; Form 1042–S, Foreign Person’s U.S. Source Income Subject to Withholding; etc.) with taxpayer filings, identify discrepancies, and select returns for audit based on risk scoring models. For example, the IRS’s Discriminant Function System (DIF) and Unreported Income Discriminant Index Formula (UIDIF) use algorithms to flag returns with a high likelihood of underreporting or noncompliance.

For taxpayers, this means the IRS is more likely to detect errors or omissions in information reporting and may expect taxpayers to have similar capabilities in their own compliance processes. Automated IRS income and name/TIN matching capabilities also increase the importance of timely and accurate corrections to information returns, as errors or mismatches can trigger backup withholding, notices, penalty assessments, and exams. Tax reporting functions should ensure their automation tools can produce original and corrected returns in the required format and time frame and that they maintain documentation to support their reporting positions.

Automating efforts to address key regulatory requirements

Challenges with automating new information and fields for compliance with new digital asset reporting requirements: The OECD’s recent enactment of CARF, which mandates and standardizes reporting of certain information on digital assets, has introduced a new era of transparency, with jurisdictions such as the United Kingdom enacting regulations for implementing these rules. Additionally, in the United States, the final digital asset regulations under Sec. 6045 require brokers to report gross proceeds, basis, and other information for sales of digital assets, including cryptocurrencies and nonfungible tokens, on Form 1099–DA, Digital Asset Proceeds From Broker Transactions, starting with transactions occurring in 2025. Automation is essential for managing the volume and complexity of these requirements and will simplify this reporting for most filers, but several challenges arise as companies endeavor to use AI to automate this process:

- Data sourcing and standardization: Digital asset transactions often occur across multiple platforms, wallets, and blockchains, with inconsistent data formats. Automated systems must be able to aggregate, normalize, and reconcile this data to accurately report sales, basis, and holding periods.

- Noncovered tax lots: Transfers from self-custody wallets or nonreporting brokers create noncovered tax lots for which basis and the acquisition date may be unknown. Automation must allow for customer-supplied information and then flag discrepancies for review.

- Dual-classification assets: Some digital assets may also be classified as securities or commodities, requiring coordination between Form 1099-DA and Form 1099-B, Proceeds From Broker and Barter Exchange Transactions, reporting. Automated systems must apply the correct coordination rules to avoid duplicate or missed reporting.

- Regulatory updates: The IRS and Treasury continue to issue guidance and notices (e.g., transition relief, new exceptions), requiring organizations to update their automation tools accordingly to remain compliant (e.g., Notice 2025-23).

Automating to address new requirements under the OBBBA: The OBBBA has introduced sweeping changes to information reporting and withholding that provide opportunities for tax reporting functions to leverage AI to manage challenges associated with implementing these changes, including:

- New thresholds: The threshold for reporting on Form ١٠٩٩-MISC, Miscellaneous Information, and 1099-NEC, Nonemployee Compensation, under Sec. 6041(a) increases from $600 to $2,000 for payments made after Dec. 31, 2025. Automation must be updated to apply the correct threshold based on the payment date. The threshold for reporting on Form 1099-K, Payment Card and Third Party Network Transactions, was also updated by the OBBBA, reverting to the pre-2023 level of 200 transactions in the aggregate and $20,000.

- Special deductions and credits: The OBBBA introduced new deductions (e.g., for qualified tips, overtime, car loan interest) and credits (e.g., for scholarship contributions). Automated systems should flag payments that may qualify for these provisions and track supporting documentation.

- Qualified auto loans: There is a new deduction for interest on loans for new U.S.-assembled vehicles. Automation should flag qualifying loans, track interest paid, and ensure proper reporting for both payers and recipients.

AI and automated processes should be updated to reflect these changes. Organizations should consider leveraging AI to update or create new process flows and written procedures to be used throughout the organization. In general, AI agents and automated processes should be flexible and rules–driven, with the ability to update logic as new provisions are clarified, updated, or amended. Additionally, while federal reporting thresholds have been published, many states have not published guidance and may not adopt federal thresholds. Organizations can leverage AI agents to monitor state–equivalent Form 1099—series reporting requirements to ensure compliance and manage risk going forward.

Automation of processes for validating tax withholding certificates: Automating the collection, review, and storage of tax withholding certificates, such as the Form W–8 series; Form W–9, Request for Taxpayer Identification Number and Certification; or FATCA and CRS self–certifications are critical for compliance with existing tax reporting and withholding requirements. Key considerations include:

- Electronic collection: Automated systems should support secure electronic collection of withholding certificates, including digital signatures that meet IRS requirements (seeIRS Publication 5316, Internal Revenue Service Advisory Council Public Report (November 2024), page 352, in which the Advisory Council recommends that the Service align electronic signature rules among reporting forms and withholding certificates).

- Validation and review: Automation should validate that forms are complete, current, and appropriate for the payee type and payment type. For example, a Form W-٨BEN-E, Certificate of Status of Beneficial Owner for United States Tax Withholding and Reporting (Entities), must include the entity’s correct Chapter 3 and Chapter 4 status, and a Form W-9 must be signed under penalties of perjury (Regs. Sec. 1.1441-1 (as amended in 2017)).

- Expiration and change in circumstances: Automated reminders should be generated for expiring forms (generally, every three years for Forms W-٨) and for changes in circumstances that may affect withholding or reporting.

- Secure storage and retrieval: Certificates must be stored securely, easily accessible by the withholding agent relying on the form, and readily retrievable for IRS examination or in response to IRS name/taxpayer identification number mismatch notices.

Considerations in proposed mergers and acquisitions: Tax reporting functions play a particularly important role when companies acquire entities or move into new jurisdictions that may require them to file information returns and deduct withholding for a new jurisdiction. Mergers and acquisitions (M&As) present unique challenges for automated tax reporting and withholding systems:

- Data migration and integration: Combining entities that may have different systems, data formats, and compliance histories may be especially challenging, particularly when the successor entity does not have access to legacy systems or documentation used by the target or business unit acquired. Automated processes must reconcile and integrate data to ensure continuity of reporting and withholding.

- Historical compliance review: Automated tools can assist in reviewing the target’s historical information returns, withholding certificates, and backup withholding compliance to identify potential exposures or liabilities.

- Change in payee status: M&A activity may result in changes to payee status (e.g., from foreign to U.S. person, or vice versa), requiring updated withholding certificates and changes to reporting logic (Regs. Sec. ١.١٤٤١-١ (as amended in 2017)).

- Transaction-specific reporting: Certain M&A transactions may trigger specific reporting requirements (e.g., Forms 1099-MISC for payments to consultants, Forms 1042-S for payments to foreign sellers, or Forms 1099-B/1099-DA for sales of securities or digital assets). Automation should flag and process these transactions appropriately.

- Due diligence and representations: Organizations should leverage automated systems and processes to support due diligence by flagging missing or expired certificates, unreported payments, or prior-year corrections and by generating reports for inclusion in transaction representations and warranties.

Automation now necessary

In an era of increasing market competitiveness, regulatory complexity, and IRS scrutiny, automation of tax reporting and withholding functions is a compliance necessity. Tax professionals must ensure that their automation strategies are robust, flexible, and responsive to ongoing changes in law and technology. By focusing on the considerations outlined above, organizations can reduce risk, improve efficiency, and position themselves for success in the evolving tax compliance landscape.

Editor

Mo Bell-Jacobs, J.D., is a senior manager, Washington National Tax, with RSM US LLP and a member of the AICPA Tax Executive Committee.

For additional information about these items, contact Bell-Jacobs at Mo.Bell-Jacobs@rsmus.com.

Contributors are members of or associated with RSM US LLP.