Gold

The Federal Reserve’s interest-rate pause, due to successfully lowering inflation, and apparently coming, subsequent pivot to reducing interest rates in 2024, is good news for commodities.

Lower rates will cause the dollar to weaken, fall and commodity prices to strengthen, rise. When positive real interest rates, which favor bond investors, turn negative, it will especially affect gold and silver prices to the upside.

The case for gold revolves around three main factors: an increasingly dovish Fed monetary policy; unsustainably high debt, fueled by excessive government spending; and central bank buying.

We are already seeing bond yields fall and the dollar weakening. Gold and the USD typically move in opposite directions.

The benchmark 10-year Treasury yield has dropped steadily over the last three months, from 5% in November to the current 3.9%. The US dollar index DXY has dropped from 106.88 on Nov. 23 to 101.71, at time of writing, a reduction of 5%.

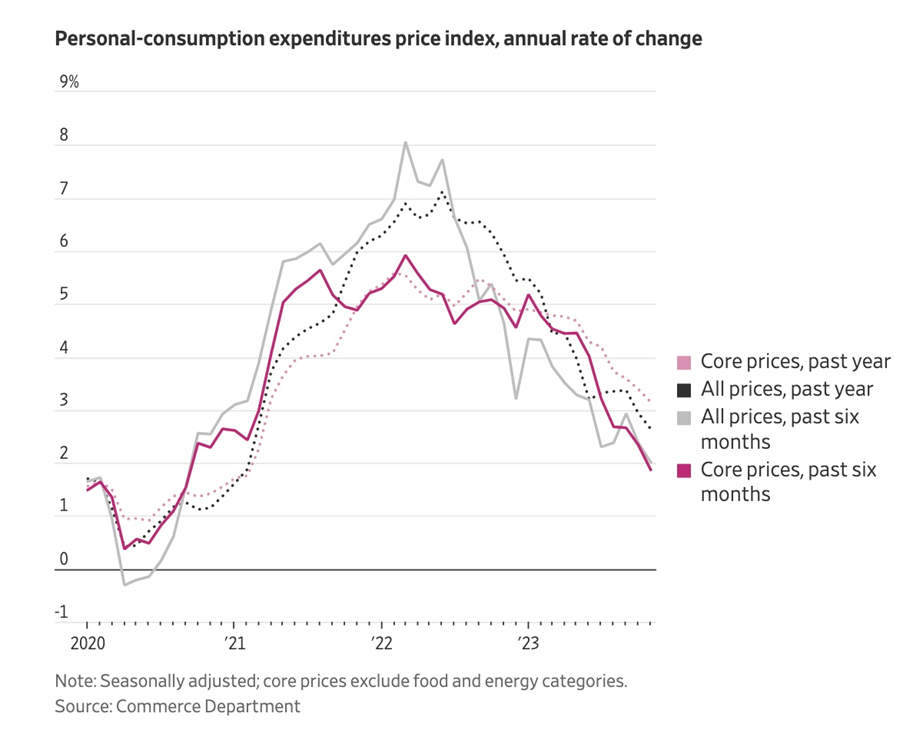

On Friday, Dec. 22, the release of the personal consumption expenditures price index, the Fed’s preferred measure of inflation, strengthened the argument that the Fed will want to reduce rates in 2024, potentially even more than the 75 basis points telegraphed by the organization earlier this month.

US prices in November fell for the first time in more than 3.5 years, pushing the annual increase to 2.6%, according to the Commerce Department. Core prices, which exclude food and energy, rose 1.9% on a six-month annualized basis.

Reuters reported Both headline and core measures cooled more than economists had anticipated, bringing the annualized rates over the past three and six months down to at or below the Fed’s 2% target.

Over the second half of the year, the center of gravity at the Fed policymaking table has become markedly more dovish, as evidence accumulates that price pressures are easing and the labor market is cooling in the face of the Fed’s rates hikes from March 2022 to July 2023.

On Thursday, third-quarter US GDP growth came in weaker than expected, at 4.9%, while claims for unemployment benefits increased by 2,000 to a seasonally adjusted 205,000, worse than market expectations.

Softening economic data and moderating inflation show that the Fed’s monetary policy is restrictive enough to bring inflation to heel.

However, we are still at positive real rates of 1.3% (3.9% 10-year yield minus 2.6% inflation), which for gold means further rate cuts are necessary before we are into a negative real rate environment.

The markets are pricing in around 79% odds of a rate cut in March.

Economist Daniel Lacalle maintains that inflation would be coming down faster if it weren’t for the fact that, “fiscal policy, for the first time in decades, is moving in the opposite direction of monetary policy. And this is likely to create significant problems in the future.”

We first pointed out this clash between the federal government and the Federal Reserve back in 2018, when Trump was president. The Fed at the time was raising interest rates, to the disappointment of Trump who wanted to keep them low.

Consider: As the Fed has pursued a tight monetary policy, unwinding its balance sheet and raising interest rates, the Treasury has been printing money that the federal government keeps spending to fulfill its many promises. The Biden administration’s three signature pieces of legislation — the Inflation Reduction Act, the Bipartisan Infrastructure Law and the CHIPS and Science Act — are costing trillions.

Remember too, that most of this promised money has yet to be spent.

Unsurprisingly, inflation has added a huge chunk to construction project costs, which has also meant delays. An Economist article notes that the biggest component of the infrastructure package was a 50% increase in funding for highways to $350B over five years. But highway construction costs soared by more than 50% from the end of 2020 to the start of 2023, in effect wiping out the extra funding.

The federal government keeps spending money and the Treasury keeps printing it, to cover the deficits which keep mounting. Around $13 trillion in government debt is expected to roll over next year, at much higher rates, meaning more money-printing is on the way.

In a recent interview with BNN Bloomberg, Pierre Lassonde, chair emeritus at Franco-Nevada Mining, said he believes the US dollar has peaked “and gold is the anti-US dollar so that is one of the reasons why I’m so bullish on gold for 2024.”

He also said that inflation next year will be “sticky”, around 3-4%, noted that the federal government is going to have a $2 trillion deficit, and argued that interest rates will come down because there is a presidential election.

“What does the Fed do in an election year? They like to make it easy for the incumbent to win the election,” said Lassonde. “So interest rates are going to come down but it’s not gonna happen in Europe, I think the euro is going to be going up vis-a-vis the US dollar, all of the other currencies will and gold will be going up.”

Asked whether cryptocurrencies are limiting gold’s upside, Lassonde pointed out that none of the central banks are buying crypto but many of them are buying gold. “They’re diversifying out of US dollars, they say we don’t really trust the dollars, we don’t trust America to let us exchange our money when we need it, and they’re buying gold,” he said, noting that when the EU slaps regulations on the crypto market, “[it] will be very small compared to the gold market.”

Finally, Lassonde said that gold stocks are trading as though gold was $1,500 an ounce, about half of their real value, “so I look at 2024 as a catch-up year for the vast majority of gold stocks. I think they’re gonna outperform any other equities on the market.”

Central banks bought a record 1,136 tonnes of gold last year and followed that up with another 228t in Q1, the most ever in a first quarter.

Central bank gold demand saw its highest first half on record dating back to 2000, the World Gold Council said.

“Record central bank demand has dominated the gold market over the last year and, despite a slower pace in Q2, this trend underscores gold’s importance as a safe haven asset amid ongoing geopolitical tensions and challenging economic conditions around the world,” Louise Street, senior markets analyst at the WGC, commented.

Robust demand for gold continued in the third quarter, with CBs collectively buying 337 tonnes, the second-highest third quarter on record. According to the World Gold Council’s most recent quarterly report, “Global official gold reserves rose… 120% higher q/q and the second highest third quarter total following Q3 2022. On a y-t-d basis, central banks have bought an astonishing net 800t, 14% higher than the same period last year.”

Arguably, the main reason central banks are buying gold is because gold is the solution to monetary debasement. As we wrote in a previous article,

In the extreme hypothetical case where all other asset classes are destroyed, including the currency itself, only gold remains.

Daniel Lacalle, the above-mentioned economist, writes, “Gold is now the only real defense against the loss of the purchasing power of fiat currencies. Considering that central banks are looking to impose their own digital currencies, gold proves again that it is an essential asset in a portfolio where investors try to escape the collapse of money as we know it.”

Two headlines picked this week from my news feed indicate that this dollar debasement trend is real and accelerating.

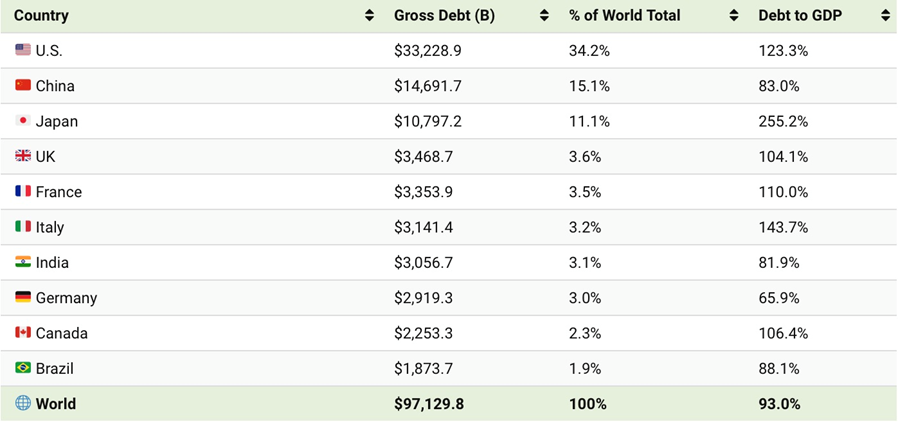

Visual Capitalist reports global government debt is projected to hit $97.1 trillion this year, a 40% increase since 2019. In a table of general government gross debt, the United States is top of the heap with a debt to GDP ratio of 123.3%. This compares to a world average of 90%.

Just as US debt has ballooned, so has Canada’s, now ranked 10th globally at 106.4% of GDP.

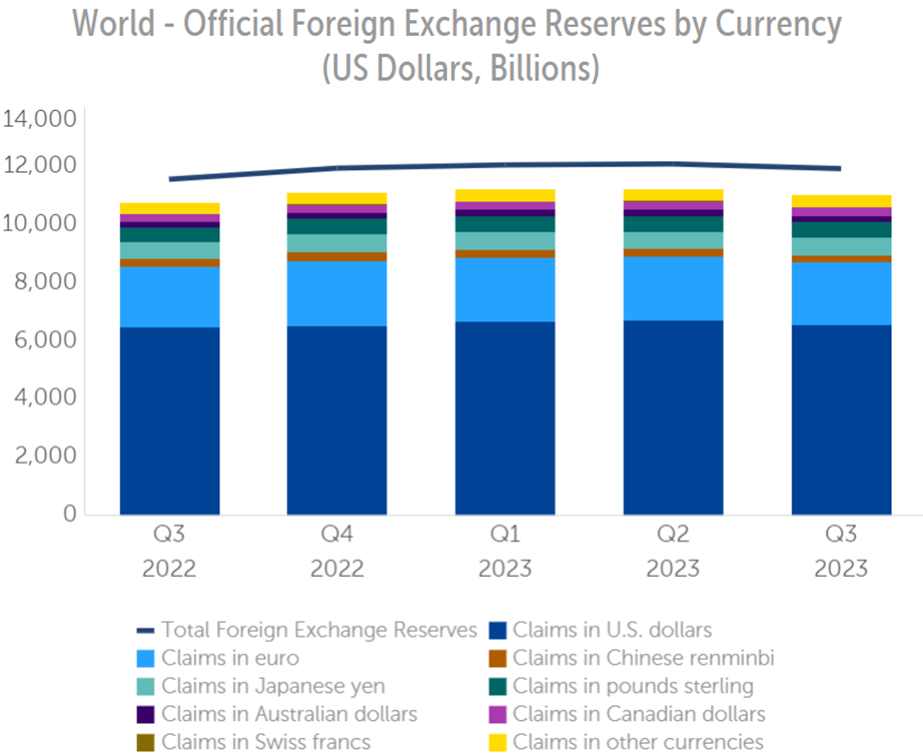

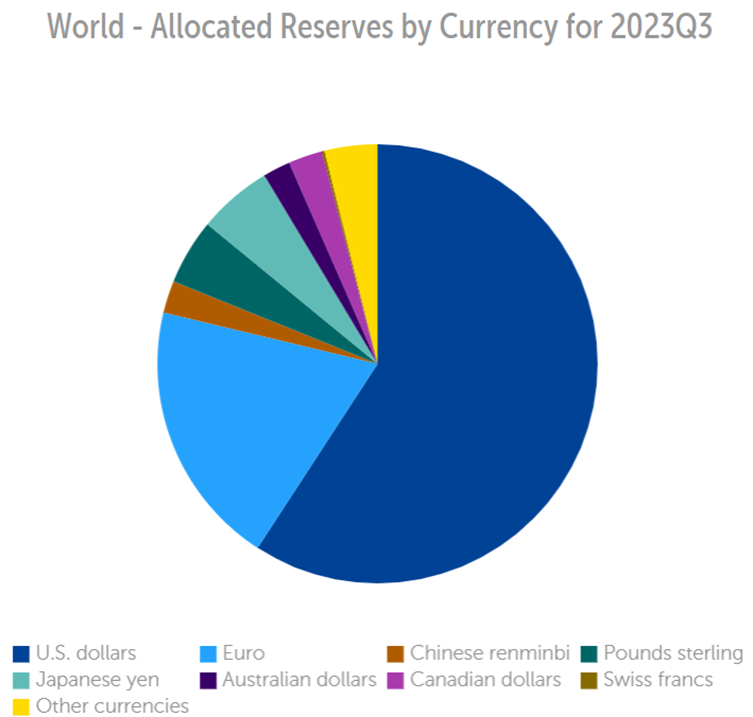

While the dollar is the most important unit of account for international trade, the main medium of exchange for settling international transactions, and the store of value for central banks, “de-dollarization” is being pursued by countries with agendas at odds with the US, including Russia, China, Saudi Arabia and Iran.

As Lassonde alludes to, many emerging-market economies are buying gold because they don’t want to be stuck in the same situation as Russia, which had about half of its foreign-currency reserves frozen following the 2022 invasion of Ukraine.

According to Markets Insider, China and Russia have now almost completely phased out their use of the US dollar in bilateral trade. More than 90% of trade between the two countries is now denominated in the Russian ruble or the Chinese yuan. Also, trade between them has expanded this year due to Western sanctions, which has made Russia more reliant on China for trade. Russian Prime Minister Mikhail Mishutstin reportedly said total transactions hit a record $200 billion this year, while Russia-US trade plummeted to a 30-year low.

Silver

Gold and silver tend to trade in tandem. When gold pushes higher, silver usually lags, but then it can outperform gold.

When precious metals rallied in 2020, on the back of lockdowns, interest rates slashed to zero, QE, and general market fear, silver’s gain was double that of gold. The price ran up 43% from January to December, 2020, compared to gold’s ‘mere’ 20.8% rise. Earlier in the year, as gold punched above $2,000 an ounce, a 39% gain, silver rallied to nearly $30 an ounce, a 147% increase.

Silver is interesting in that there is the same amount of investable silver above ground as there is gold, because 60% of silver goes into industrial uses and 80% of that end up in landfills. Just 40% is used for investing.

As the metal with the highest electrical and thermal conductivity, silver is ideally suited to solar panels. A 2020 Saxo Bank report stated that “potential substitute metals cannot match silver in terms of energy output per solar panel.”

Using silver as conductive ink, photovoltaic cells transform sunlight into electricity. Silver paste within the solar cells ensures the electrons move into storage or towards consumption, depending on the need. It is estimated that approximately 100 million ounces of silver are consumed per year for this purpose alone.

“The U.S. Department of Commerce has made it official: It’s imposing import duties on Chinese solar manufacturers that have been evading tariffs and are “undermining American industries,” according to the trade law arbiter.

The Commerce Department found that a number of major Chinese solar panel suppliers — BYD, Canadian Solar, Trina Solar and Vina Solar — circumvented existing antidumping tariffs by routing products to Cambodia, Malaysia, Thailand or Vietnam for “minor processing” before shipment to the U.S. The companies, which supply a sizable portion of American solar panels, will now face heavy tariffs starting in June 2024. Duties were also levied on a fifth company, Cambodia-based New East Solar, which failed to comply with the investigation.” Canary Media

Analysis by BMO Capital Markets has annual silver consumption by the solar industry growing even higher at 85% to about 185 million ounces within a decade.

5G technology is set to become another big new driver of silver demand. Among the 5G components requiring silver, are semiconductor chips, cabling, microelectromechanical systems (MEMS), and Internet of things (IoT)-enabled devices.

The Silver Institute expects silver demanded by 5G to more than double, from its current ~7.5 million ounces, to around 16Moz by 2025 and as much as 23Moz by 2030, which would represent a 206% increase from current levels.

A third major industrial demand driver for silver is the automotive industry. Silver is also found in many car components throughout vehicles’ electronic systems, and despite not being used in batteries, its superior electrical properties make it hard to replace across a wide and growing range of automotive applications.

A Silver Institute report says battery electric vehicles contain up to twice as much silver as ICE-powered vehicles, with autonomous vehicles requiring even more due to their complexity. Charging points and charging stations are also expected to demand a lot more silver.

It estimates the sector’s demand for silver will rise to 88Moz in five years as the transition from traditional cars and trucks to EVs accelerates. Others estimate that by 2040, electric vehicles could demand nearly half of annual silver supply.

In 2021, brazing and soldering alloys used 47.7Moz of silver, representing 9.3% of the total industrial demand for silver that year. Last year brazing and alloys accounted for 49Moz.

By 2030, the demand for silver used in brazing and soldering is forecast to reach 58.8Moz, a 23% increase over 2021, according to a Silver Institute report titled ‘Silver in Brazing and Solder Alloy Materials’.

Finally, silver demand for “printed and flexible electronics” is forecast to increase 54% over the next nine years, rising from 48Moz in 2021 to 74Moz in 2030, meaning a consumption of 615Moz during this time frame.

A Silver Institute news release describes them as “mainstays” in a variety of electronic products, including sensors that measure everything from temperature, pressure and motion, to moisture, relative humidity and carbon monoxide. They are also used in medical devices, mobile phones, appliance displays and consumer electronics.

In 2021, a comprehensive report by Sprott titled ‘Silver’s Clean Energy Future’ found that three areas of growing demand for silver — solar, automotive and 5G — potentially account for more than 125 million ounces in 10 years. This doesn’t include the growth in investment demand for silver, which as mentioned represents about 40% of usage.

Analysts have long been pointing to a severe shortage of silver due to the relentless growth in demand for the metal.

According to the 2023 World Silver Survey, the global silver market was undersupplied by 237.7 million ounces in 2022, which the Institute says is “possibly the most significant deficit on record.”

It took just two years of undersupply — the 2022 deficit and the 51.1 million oz shortfall from 2021 — to wipe out the cumulative surpluses from the previous decade.

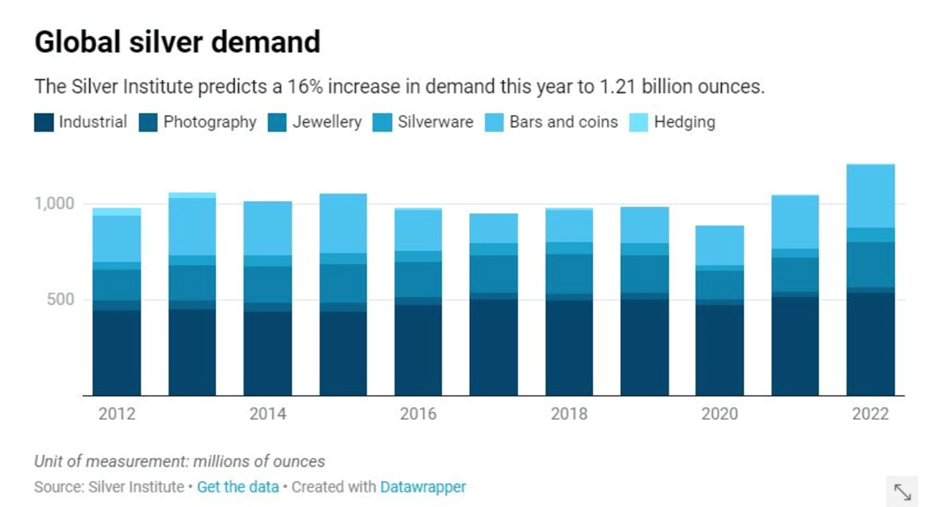

Global silver mine production is projected to fall 2% this year to about 820 million ounces, compared to forecasted demand of 1.2 billion ounces. First Majestic Silver’s CEO Keith Neumeyer recently commented that the solar panel and electric car industries now consume about 30% of mined silver supply. Moreover, he said one primary silver mine produces about 10 million ounces a year, meaning it has “zero impact” on the deficit, which represents several mines worth of production.

The Silver Institute forecasts a 140Moz silver deficit this year, the third consecutive annual shortfall, against robust silver industrial demand, which is expected to grow 8% to a record 632Moz. Key drivers include investment in photovoltaics, power grid and 5G networks, growth in consumer electronics, and rising vehicle output.

Metals Focus believes the deficit will persist in the silver market for the foreseeable future.

Conclusion

At AOTH, we see strong upside for gold and silver as we head into 2024.

I’ve been right in my prediction that the Fed would pause in June, and hike once or twice more before the end of the year.

I’ve also voiced my opinion that we will get a soft landing with no, or an extremely shallow and very short recession, with the important proviso that the Fed pauses its rate-hiking cycle, which it has already done.

Remarkably, the Federal Reserve has raised interest rates high enough to reverse the inflation rate, without causing a severe downturn. And it’s done it in an extremely short amount of time.

Softening economic data and moderating inflation show that the Fed’s monetary policy is restrictive enough to bring inflation to heel.

The US dollar is weakening and bond yields are falling. We aren’t yet in a gold-friendly environment due to positive real rates but we believe rates will turn negative as bond yields fall further and inflation remains sticky, likely in the 3-4% range.

There are multiple reasons to trade gold — US dollar movements, geopolitical tensions, ETF outflows, central bank buying, negative real rates, etc., but only one reason to own it: maintaining your purchasing power against dollar (or other currency) losses incurred by inflation.