For the first time this cycle, a silver miner has filed hard numbers on a forced production cut, and a mine-safety crackdown in China is behind it, not anything the price did.

Silver trades near $58 today, having slipped back below its early-July low. The metal is down roughly 18% from where it closed 2025, near $71, and it sits about 52% below the all-time high of $121.62 set on January 29, though it remains up more than half from a year ago. Against gold near $4,000, the gold-silver ratio is about 69. The correction of the past two months has been a monetary story, driven by a firm dollar and a hawkish Federal Reserve as renewed US-Iran tension lifts oil and inflation risk, rather than anything that happened in silver’s own supply and demand.

Underneath that price, the structural picture has not changed. The market is on track for its sixth consecutive annual deficit, forecast at 46.3 million ounces for 2026 by Metals Focus and the Silver Institute, meaning the world is set to use more silver than it produces for the sixth year running. Much of the bull case has rested on a single claim: that silver supply cannot respond to a higher price the way most commodities do, because roughly three-quarters of it comes out of the ground as a byproduct of mining copper, lead, zinc, and gold, and you cannot will more of it into existence by drilling a silver mine. This window gave that argument a concrete, quantified example, and it came from an unexpected direction. This is the kind of supply-side development the Silver Catalyst newsletter I publish through Golden Meadow® tracks issue by issue, and it is worth seeing in full against how silver has traded in 2026.

The Silvercorp cut

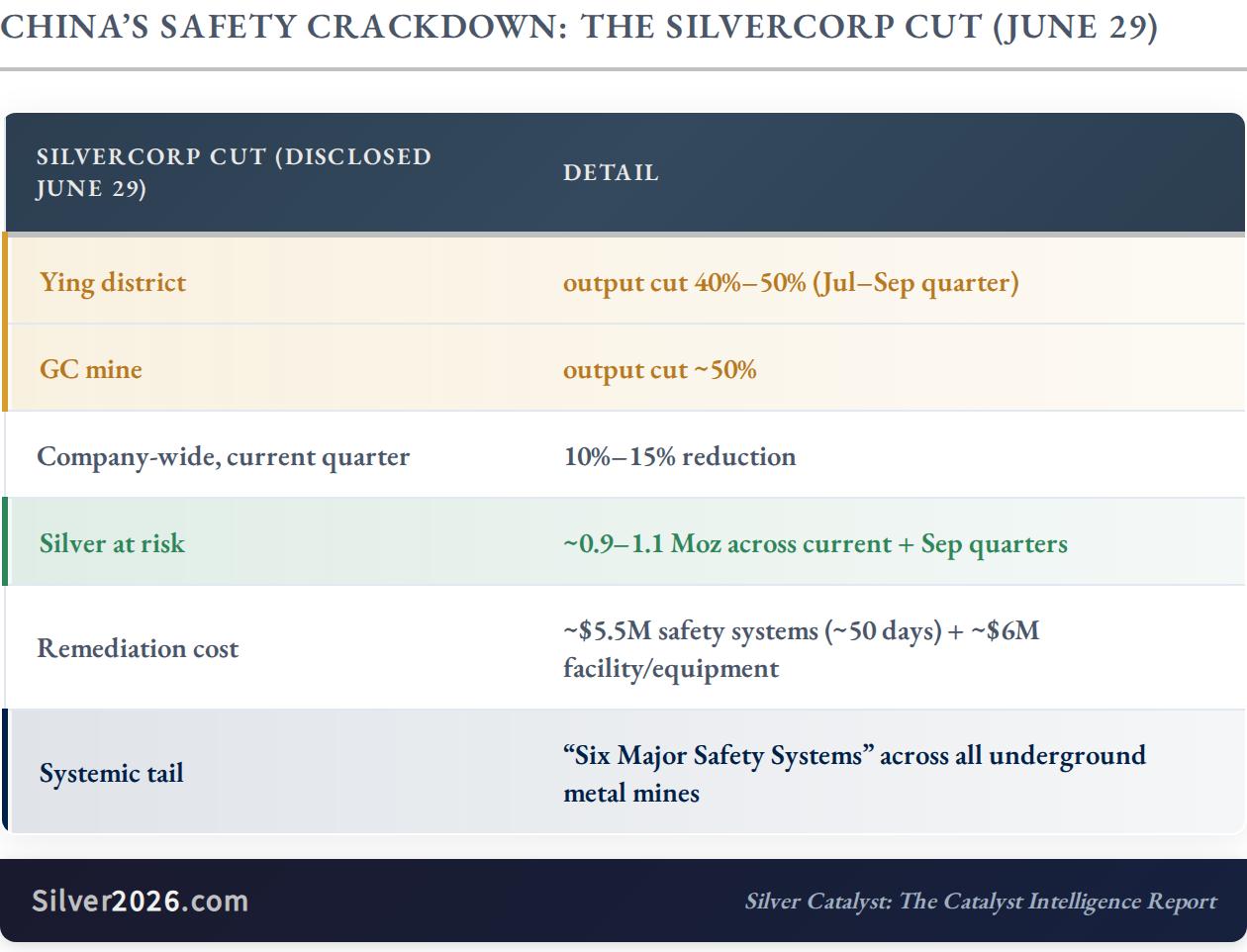

On June 29, Silvercorp Metals, a Canadian-listed company that operates silver mines in China, disclosed that an intensifying mine-safety crackdown will cut its production over the July-to-September quarter. Output at its Ying district will fall by 40% to 50%, its GC mine by roughly 50%, and the company as a whole expects a reduction of 10% to 15% this quarter. Set against Silvercorp’s most recent full-year output of about 6.3 million ounces at Ying and 0.5 million at GC, the cut puts somewhere between 0.9 and 1.1 million ounces of silver at risk across the affected quarters.

The important part is not the company. It is the reason. The trigger was a fatal coal-mine accident in Shanxi province in late May that pushed Beijing to extend its long-standing “Six Major Safety Systems” requirements to every underground non-coal mine in the country, backed by a national monitoring network that now tracks more than a million sensors in real time. For Silvercorp, complying means spending about $5.5 million on certified safety-system installations over roughly 50 days, plus another $6 million on facility and equipment upgrades, close to $11.5 million in all. That is money spent to keep operating, not to produce more, and it raises the real cost of every ounce that still comes out.

Sources: Silvercorp — Updates on China Operations | Silvercorp — FY2026 Results and FY2027 Guidance | StockTitan — Silvercorp 6-K | SBS — Shanxi Mine Disaster | CGTN — China’s Mine-Safety Sensor Network | The Globe and Mail — Silvercorp Slows China Mines as New Safety Rules Bite | Metals Focus and the Silver Institute — World Silver Survey 2026

Silvercorp is one operator, but the rule that hit it applies to every underground metal mine in China, which is why the same enforcement that slowed Silvercorp could remove several million more ounces across the country, even though only the Silvercorp figure is firm today. China is a major silver producer and an even larger force in refining, so the direction of travel matters more than the figure from any single company.

What this means to Silver investors

Keep the size honest first. A cut of 0.9 to 1.1 million ounces is small against the roughly 846.6 million ounces the world’s mines produced in 2025, barely more than a tenth of one percent, and by itself it does not move the annual balance. Anyone selling this as an overnight shortage is overselling it.

What makes it matter is the mechanism. The claim that silver’s supply cannot answer a higher price gets its obvious test when the price rises sharply, as it did to record highs into early 2026. The answer this window is that supply did not expand, it contracted, and it contracted for a reason a higher price cannot reverse. A safety crackdown pulled ounces offline that a far higher price could not have called forth and cannot bring back. If supply bends that way under enforcement while it refuses to bend upward under price, then the supply side that underwrites a sixth straight deficit is even less able to answer a rally than the balance assumes.

That is the quiet significance here: not the tonnage, but the proof of concept. In Issue #19, I discussed the two-speed split between a rebuilding New York vault and a rising Shanghai premium, a market where the West looks amply supplied while the East pays up to hold physical. The Silvercorp cut sits on the same side of the ledger as that Eastern tightness: evidence that the physical squeeze runs deeper than the Western paper price lets on. None of this points to a particular level on the chart, and I would be wary of anyone who says it does. The longer-term case for silver rests on a structural deficit and a supply base that cannot easily grow, and this window added a piece of evidence that the second half of that sentence is real.

China’s safety crackdown is one dimension of the 100-catalyst framework I analyze in Silver Rising, alongside the five other Deep Dives in this issue of the Silver Catalyst newsletter. If you’ve at least considered investing in silver, I strongly encourage you to sign up, because it takes just $1 to get both. Get full Silver Catalyst Newsletter and Silver Rising book for $1 today.