Hong Kong’s decision to launch trading in Chinese government bond futures has put fresh attention on stocks tied to the city’s financial plumbing, from brokers to exchange operators. For investors watching how new yuan products might shape liquidity, risk management and global access to China’s bond market, this is a moment to reassess which Hong Kong financials appear best placed and which might warrant more caution. This article highlights three stocks from our Hong Kong Financials and Exchange Operators screener that are directly exposed to the bond futures news, and explains how each could be affected by this shift.

China International Capital (SEHK:3908)

Overview: China International Capital is a large Beijing based investment bank and securities firm that helps companies raise money, trade stocks and bonds, manage assets and wealth, and invest through private equity funds across Mainland China and overseas markets.

Market Cap: HK$155.1b

China International Capital stands out in this bond futures story because it already operates across investment banking, trading, asset management and wealth, putting it at the heart of how new yuan products could be structured, traded and distributed. Analysts see solid earnings and revenue growth ahead and the stock is priced on a relatively low P/E compared with peers, which may appeal if you are looking for exposure to China’s capital markets without paying up. At the same time, a history of uneven longer term earnings and questions around funding structure and board turnover mean this is not a set and forget holding. The opportunity is clear, but the real question is how investors weigh that trade off.

China International Capital’s mix of broad capital markets exposure and a relatively low P/E raises an obvious question: how much of that is already explained in the analysis report for China International Capital

Hong Kong Exchanges and Clearing (SEHK:388)

Overview: Hong Kong Exchanges and Clearing runs the core stock, futures and clearing platforms that sit at the centre of Hong Kong’s markets, linking investors and issuers across Hong Kong, Mainland China and the UK in cash equities, derivatives, commodities and market data.

Operations: The company generates most of its revenue from Cash activities at HK$15.5b, followed by Equity and Financial Derivatives at HK$7.0b, with smaller contributions from Commodities at HK$3.4b, Data and Connectivity at HK$2.3b, and Corporate Items at HK$1.9b.

Market Cap: HK$484.6b

Hong Kong Exchanges and Clearing sits at the point where the new Chinese government bond futures will trade. Any uplift in yuan bond risk management and offshore participation flows directly through its trading and clearing pipes. The company reports high profitability, with a 34% ROE and net margins above 60%, and is broadening into fixed income, commodities and data so it is not purely a cash equities story. That strength comes with trade offs, including a rich valuation, reliance on external borrowing rather than customer deposits, and sensitivity to policy shifts between Hong Kong and Mainland China. For investors who see long term value in China access, the key consideration is whether those risks justify a closer look at Hong Kong Exchanges and Clearing.

Hong Kong Exchanges and Clearing’s rich valuation and high profitability raise a bigger question: is the market fully pricing how Chinese government bond futures could reshape its revenue mix, or are investors missing something in the 3 key rewards and 1 important warning sign

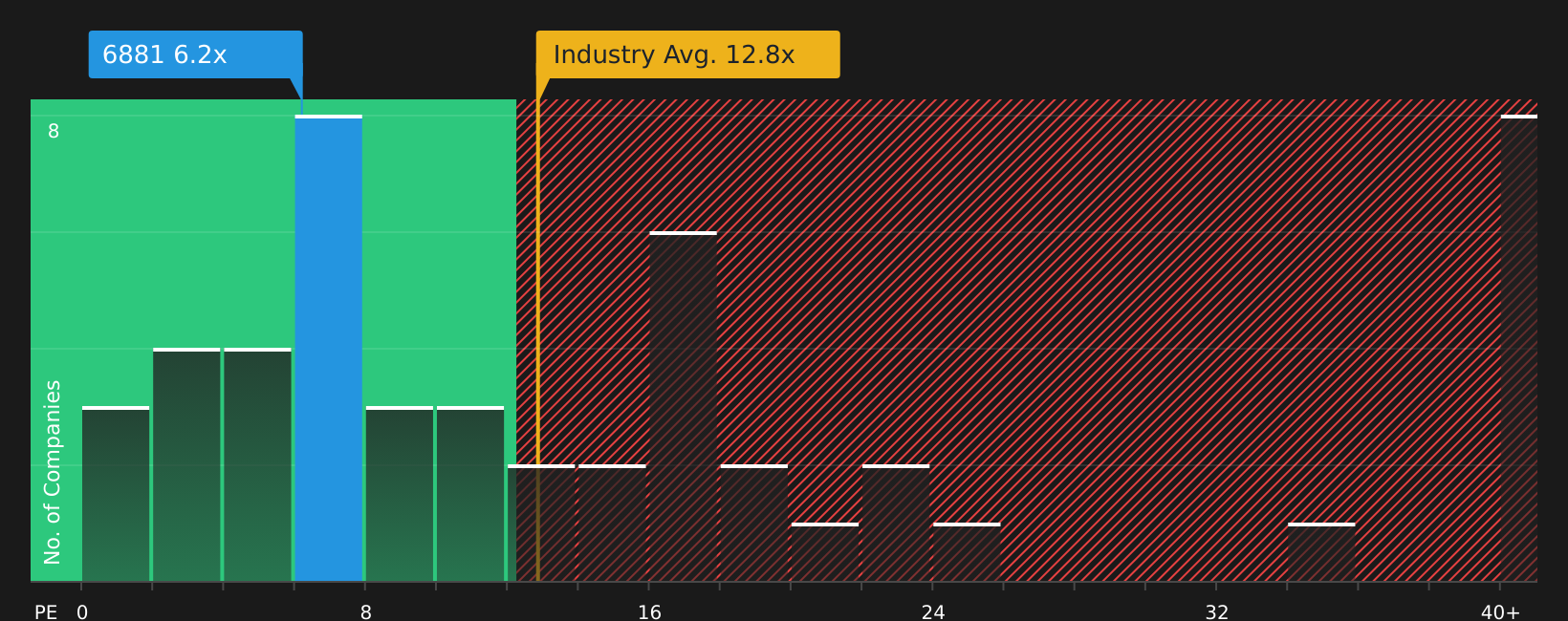

China Galaxy Securities (SEHK:6881)

Overview: China Galaxy Securities is a Beijing based brokerage and investment firm that helps retail and institutional clients trade stocks, bonds, funds and derivatives, while also offering investment banking, research, asset management and international securities services.

Market Cap: HK$135.9b

China Galaxy Securities looks interesting in the context of Hong Kong’s new Chinese government bond futures because it combines a broad brokerage and derivatives platform with what analysts view as solid revenue and earnings growth expectations. Yet it trades on a P/E that is below both peers and the wider Hong Kong capital markets industry. Forecast revenue growth of around 10.6% a year and an earnings growth trajectory of 11.58% sit alongside a high net profit margin of 38.5%. However, investors still have to weigh funding that relies entirely on higher risk external borrowing and an unstable dividend track record. With board turnover and governance changes also in focus, the real question is whether the pricing already reflects those risks or if China Galaxy Securities is being overlooked.

China Galaxy Securities’ combination of a lower P/E and analyst expectations for both revenue and earnings growth invites a closer examination of whether the market is mispricing its risks, beginning with the analyst forecasts for China Galaxy Securities

The three Hong Kong financial stocks in this article are just a starting point, and the full Hong Kong Financials and Exchange Operators screener surfaces 5 more companies with equally compelling stories around exchange operations, brokerage and investment banking. Use Simply Wall St to identify and analyze the specific catalysts and narratives that matter to you so you can focus on the highest conviction opportunities in this theme.

Take Control of Your Investment Journey

If Hong Kong Exchanges and Clearing or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point.

Once you’ve made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates.

Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives.

By uncovering hidden catalysts and risks early, you’ll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Before They Fly?

New themes are breaking out, momentum is building and the best ideas rarely stay under the radar for long. Before the crowd catches up, consider looking for opportunities early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Hong Kong Exchanges and Clearing might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com