Europe Property Management Market Size

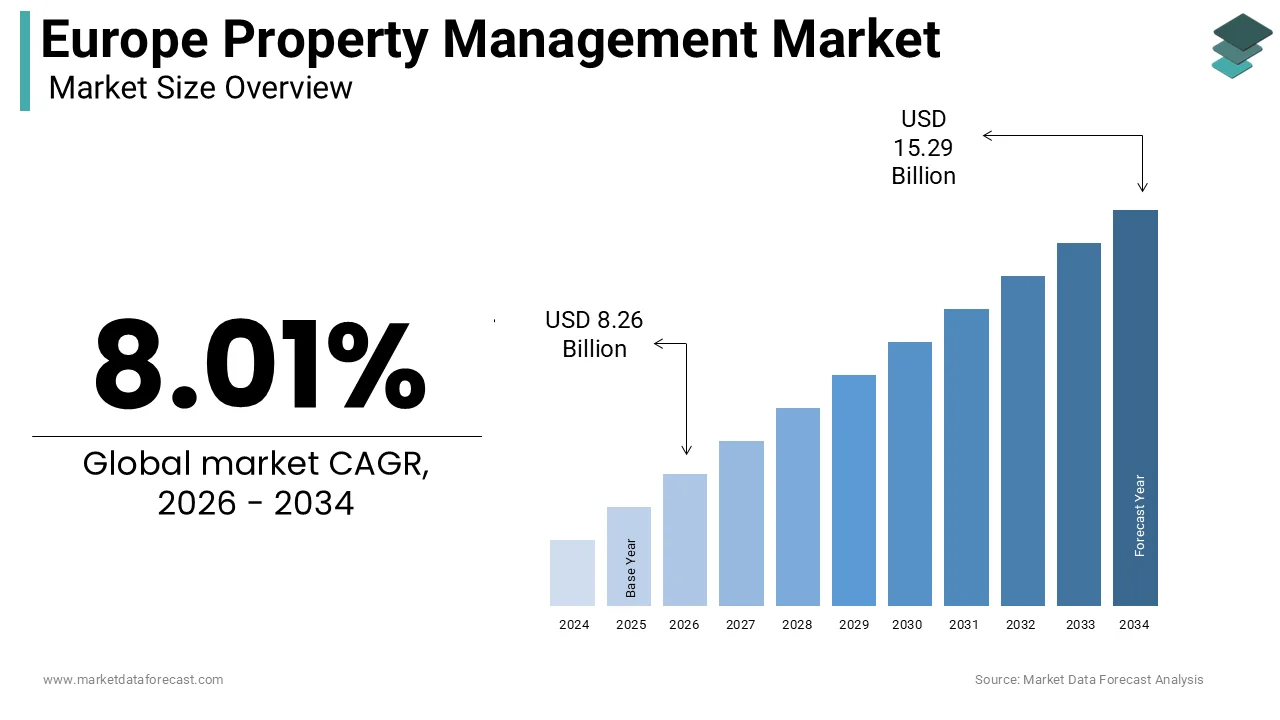

The Europe property management market size was calculated to be USD 7.64 billion in 2025 and is anticipated to be worth USD 15.29 billion by 2034, from USD 8.26 billion in 2026, growing at a CAGR of 8.01% during the forecast period.

Property management encompasses a comprehensive suite of services designed to oversee residential, commercial, and industrial real estate assets on behalf of owners. These services include tenant acquisition, lease administration, maintenance coordination, financial reporting, and regulatory compliance. The sector is undergoing a significant transformation driven by the integration of digital technologies and the increasing complexity of urban real estate portfolios. As per Eurostat data, the urban population in the European Union accounted for 75% of the total population in 2023, which is creating sustained demand for efficient housing and commercial space management. Furthermore, the European Commission reported that the construction sector contributes approximately 9% to the EU GDP, indicating the economic significance of real estate activities. The aging building stock in Europe necessitates rigorous maintenance and retrofitting efforts, which are central to modern property management operations. According to the International Energy Agency, buildings account for 40% of energy consumption in Europe, prompting managers to adopt sustainable practices and smart building technologies. The regulatory landscape is also evolving with the European Green Deal imposing stricter energy efficiency standards on existing structures. This environment requires property managers to possess specialized knowledge in sustainability compliance and technological integration. The shift towards remote work has further altered demand patterns for office spaces, leading to adaptive reuse strategies. Consequently, the property management sector acts as a critical intermediary ensuring asset value preservation, operational efficiency, and tenant satisfaction in a rapidly changing European real estate landscape.

MARKET DRIVERS

Rapid Urbanization and Increasing Demand for Rental Housing

Rapid urbanization and the consequent surge in demand for rental housing are majorly driving the growth of the Europe property management market. As more individuals migrate to urban centers for employment and educational opportunities, the pressure on housing infrastructure intensifies. As per Eurostat, 75% of the EU population lived in cities, towns, and suburbs in 2023, a figure that continues to rise annually. This demographic shift creates a robust tenant base for residential properties requiring professional management to handle leasing turnovers, maintenance requests, and tenant relations efficiently. In major metropolitan areas such as London, Berlin, and Paris, the shortage of affordable homeownership options has led to a long-term rental culture. According to the European Real Estate Society, the share of households renting their primary residence in the EU increased to 31% in recent years, reflecting a structural change in housing preferences. Professional property managers are essential in this context to ensure high occupancy rates and minimize vacancy periods, which directly impact owner returns. The complexity of managing multi-unit residential buildings in dense urban environments necessitates specialized expertise in conflict resolution, community management, and regulatory adherence. Furthermore, the rise of build-to-rent developments has institutionalized the rental sector, attracting large-scale investors who rely on professional management firms to operate their portfolios. This trend ensures a steady stream of revenue for property management companies and drives the adoption of standardized operational protocols across the region.

Regulatory Pressure for Energy Efficiency and Sustainability Compliance

Stringent regulatory frameworks mandating energy efficiency and sustainability compliance significantly drive the demand for specialized property management services in Europe, which is further contributing to the regional market growth. The European Green Deal and the Energy Performance of Buildings Directive require existing buildings to undergo substantial retrofits to meet carbon reduction targets. As per the European Commission, all new buildings must be zero-emission by 2030, and existing stocks must be upgraded to improve their energy performance ratings. Property managers play a pivotal role in coordinating these renovations, liaising with contractors, securing permits, and ensuring compliance with local building codes. According to the International Energy Agency, 75% of the building stock in Europe is energy inefficient, requiring extensive modernization efforts over the next two decades. This regulatory burden transforms property management from a purely administrative function into a strategic consultancy role focused on asset enhancement and value preservation. Managers must also navigate complex reporting requirements related to environmental, social, and governance criteria, which are increasingly important for institutional investors. The implementation of smart building technologies such as automated heating, ventilation, and air conditioning systems requires ongoing monitoring and optimization, which falls under the purview of modern property management firms. Failure to comply with these regulations can result in significant fines and reduced asset valuations, making professional management indispensable. Consequently, the legislative push towards sustainability creates a sustained demand for knowledgeable property managers who can guide owners through the transition to green building standards.

MARKET RESTRAINTS

Fragmented Regulatory Landscape across Member States

The fragmented regulatory landscape across European member states is hindering the growth of the Europe property management market. Each country possesses distinct legal frameworks governing landlord-tenant relationships, rental controls, eviction processes, and safety standards, which complicates cross-border operations. As per the European Parliament, there are substantial differences in tenancy laws between nations, such as Germany’s strong tenant protections versus the more landlord-friendly regulations in the United Kingdom. This lack of harmonization prevents property management firms from implementing uniform operational procedures and software solutions across their European portfolios. According to the European Real Estate Federation, the cost of compliance varies significantly by jurisdiction, requiring firms to maintain localized legal expertise and administrative teams. This fragmentation increases operational costs and reduces economies of scale, particularly for international players seeking to expand their market presence. Additionally, frequent changes in local legislation, such as rent caps in Berlin or Barcelona, create uncertainty and financial risk for property owners and managers. The need to constantly adapt to varying regulatory environments hinders the development of standardized technology platforms that could streamline processes. Consequently, smaller regional firms often dominate local markets while larger international entities face barriers to efficient expansion. This regulatory complexity limits market consolidation and slows the adoption of innovative management practices that rely on standardized data and processes.

High Operational Costs and Labor Shortages

High operational costs and persistent labor shortages are also impeding the regional market expansion. The sector is labor-intensive, requiring skilled personnel for tasks such as facility maintenance, customer service, and financial administration. As per Eurostat, the construction and real estate sectors in several European countries reported acute labor shortages in 2023, with vacancy rates for skilled technicians reaching record highs. This scarcity of qualified workers drives up wage costs and delays maintenance responses, negatively impacting tenant satisfaction and retention. According to the European Centre for the Development of Vocational Training, the mismatch between available skills and industry needs is expected to widen as digitalization advances. Property management firms struggle to find staff proficient in both traditional building maintenance and modern smart building technologies. Furthermore, inflationary pressures have increased the cost of materials and insurance, further squeezing profit margins. In the United Kingdom, the Royal Institution of Chartered Surveyors noted that operational costs for property firms rose by 15% in the past year due to energy price hikes and supply chain disruptions. These financial pressures limit the ability of firms to invest in technology upgrades and staff training, which are crucial for long-term competitiveness. Small and medium-sized enterprises are particularly vulnerable as they lack the financial resilience to absorb these cost increases. Consequently, the combination of rising expenses and workforce constraints restrains market expansion and forces many operators to prioritize cost-cutting over innovation.

MARKET OPPORTUNITIES

Integration of PropTech and Smart Building Solutions

The integration of property technology, PropTech, and smart building solutions presents a lucrative opportunity for the Europe property management market. Advanced technologies such as Internet of Things sensors, artificial intelligence, and cloud-based real-time building performance and predictive maintenance. As per the European PropTech Association, investment in PropTech startups in Europe reached 2 billion euros in 2023, indicating strong investor confidence in digital transformation. Smart meters and automated HVAC systems allow property managers to optimize energy consumption, reducing utility costs and enhancing sustainability credentials. According to McKinsey and Company, the adoption of smart building technologies can reduce operating costs by up to 20% while improving tenant comfort and retention. Property management firms that leverage these technologies can offer data-driven insights, enabling better decision makingdecision-makingtal expenditures and lease negotiations. Mobile applications facilitate seamless communication between tenants and managers, allowing for instant reporting of issues and transparent tracking of resolution progress. This digital engagement enhances the user experience and builds trust. Furthermore, the aggregation of building data supports compliance with environmental reporting requirements and enables participation in green financing schemes. By embracing PropTech, property managers can differentiate themselves in a competitive market and create new revenue streams through value-added technological evolution, transforming property management from a reactive service into a proactive strategic partner.

Expansion of Flexible Workspace and Co-Living Models

The expansion of flexible workspace and co-living models offers significant growth opportunities for the Europe property management market as consumer preferences shift towards flexibility and community. The rise of remote work has reduced demand for traditional long term officlong-termwhile increasing the need for adaptable workspaces. As per Global Workplace Analytics, the number of remote workers in Europe has doubled since 2020, driving demand for coworking spaces and hybrid office solutions. Property managers can capitalize on this trend by converting vacant office floors into flexible work environments or managing dedicated coworking facilities. Similarly, the co-living sector is gaining traction among young professionals and students who seek affordable housing with shared amenities and social interaction. According to JLL, the co-living market in Europe is projected to grow by 15% annually over the next five years. Managing these assets requires specialized skills in community building, dynamic pricing, and short-term leasing. Property management firms that develop expertise in these niche segments can capture higher yields compared to traditional long-term rentals. The ability to manage high turnover rates and provide concierge-style services creates a competitive advantage. Furthermore, these models align with urban densification trends and sustainability goals by maximizing space utilization. By diversifying into flexible living and working solutions, property managers can mitigate risks associated with traditional lease cycles and tap into emerging demographic trends.

MARKET CHALLENGES

Cybersecurity Risks and Data Privacy Concerns

Cybersecurity risks and data privacy concerns are major challenges to the Europe property management market as firms increasingly rely on digital platforms and connected devices. Property managers handle sensitive personal and financial data, including tenant identities, payment details, and access codes, making them attractive targets for cyberattacks. As per the European Union Agency for Cybersecurity, the number of ransomware attacks on real estate firms increased by 30% in 2023, highlighting the growing vulnerability of the sector. The integration of Internet of Things devices in smart buildings expands the attack surface, potentially allowing hackers to compromise building security systems or disrupt essential services. Compliance with the General Data Protection Regulation imposes strict obligations on data handling, requiring robust encryption, access controls, and incident response plans. According to the European Data Protection Board, non-compliance can result in fines of up to 4% of global annual turnover, posing significant financial risks. Many property management firms, particularly smaller operators, lack the resources to implement comprehensive cybersecurity measures, leaving them exposed to breaches. A successful attack can damage reputation, erode tenant trust, and lead to legal liabilities. Furthermore, the complexity of managing data across multiple jurisdictions with varying privacy laws adds to the operational burden. Ensuring the security of digital ecosystems requires continuous investment in technology and staff training, which strains limited budgets. Consequently, cybersecurity remains a persistent and evolving challenge that threatens the stability and integrity of property management operations in Europe.

Resistance to Technological Adoption Among Traditional Stakeholders

Resistance to technological adoption among traditional stakeholders, including property owners, tenants, and legacy management firms,s poses a significant challenge to the expansion of the Europe property management market. Many older property owners are accustomed to manual processes and are reluctant to invest in digital tools due to perceived costs and complexity. As per a survey by the Royal Institution of Chartered Surveyors, 40% of real estate professionals cited cultural resistance as a primary barrier to digital transformation. Tenants, particularly in the senior demographic, may struggle with mobile apps and online portals, preferring face-to-face interactions and paper-based communications. This digital divide hinders the implementation of efficient self-service models and automated workflows. Legacy management firms often operate on outdated software systems that are incompatible with modern PropTech solutions, creating data silos and inefficiencies. According to Deloitte, integrating new technologies with legacy systems can take up to two years and cost significantly more than initial estimates. The lack of standardized data formats further complicates interoperability between different platforms. Overcoming this resistance requires extensive change management efforts, including training programs and demonstration of tangible benefits. However, the slow pace of adoption delays the realization of efficiency gains and limits the scalability of innovative solutions. Consequently, the industry faces a fragmented landscape where digital leaders coexist with laggards, impeding overall market progress and standardization.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

8.01% |

|

Segments Covered |

By Property Type, Service Type, End User, And Region |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

Yardi Systems, Inc., AppFolio, Inc., MRI Software LLC, SAP SE, Oracle Corporation, Trimble Inc., IBM Corporation, Accruent, LLC, Planon Group, ARCHIBUS, Inc. |

SEGMENTAL ANALYSIS

By Property Type Insights

The residential segment held the leading position in the Europe property management market by holding 54.6% of the regional market share in 2025. The dominance of the residential segment in the European market is attributed to the rapid urbanization and a persistent shortage of affordable housing, which has shifted demographic preferences towards renting. As per Eurostat, 75% of the European Union population lived in cities, towns, and suburbs in 2023, creating a concentrated demand for managed rental units. The high cost of homeownership in major economic hubs such as London, Paris, and Munich has forced younger generations and mobile professionals into the rental market for extended periods. According to the European Real Estate Society, the share of households renting their primary residence in the EU reached 31%, reflecting a structural shift in housing tenure. Professional property managers are essential in this context to handle the high volume of tenant turnover, lease negotiations, and maintenance requests associated with dense urban living. The rise of institutional investors in the build-to-rent sector has further professionalized the market, requiring standardized management practices to ensure asset performance. Additionally, stringent tenant protection laws in countries like Germany and France necessitate expert navigation of legal compliance regarding evictions and rent controls. This regulatory complexity makes professional management indispensable for landlords seeking to mitigate risk. Consequently, the combination of demographic trends and regulatory requirements solidifies the residential segment as the cornerstone of the European property management industry.

On the other hand, the industrial segment is projected to register the highest CAGR of 9.4% over the forecast period in the European market. Factors such as the explosive growth of e-commerce and the strategic reshoring of supply chains are propelling the growth of the industrial segment in the regional market. The demand for last-mile delivery hubs and large distribution centers has surged as consumers increasingly rely on online shopping. As per Eurostat, e-commerce sales in the European Union accounted for 23% of total retail turnover in 2023, necessitating an extensive logistics infrastructure. Property managers are critical in maintaining these facilities, which often feature advanced automation and high ceiling specifications. According to CBRE, the vacancy rate for industrial properties in key European markets remained below 5% in 2023, indicating strong demand and limited supply. These tight market conditions require proactive leasing strategies and efficient facility management to minimize downtime. Furthermore, geopolitical tensions and pandemic-related disruptions have prompted manufacturers to nearshore production facilities closer to end markets, increasing the need for industrial space in Europe. The European Commission’s industrial strategy supports this trend by encouraging domestic manufacturing capabilities. Property management firms adapt by offering specialized services such as energy management for high-consumption facilities and compliance with environmental regulations. The integration of smart warehouse technologies also requires technical expertise for maintenance and optimization. These factors combine to make industrial property management a rapidly expanding sector within the European market.

By Service Type Insights

The facility management segment led the market and occupied 41.4% of the regional market share in 2025. The growth of the facility management segment in the European market is driven by the critical need for comprehensive operational support to maintain building functionality, safety, and compliance. Facility management encompasses a wide range of services, including cleaning, security, maintenance, and utilities management, which are essential for the daily operation of any property. As per the European Facility Management Network, the facility management sector in Europe employs over 6 million people, highlighting its economic significance and widespread adoption. Property owners rely on professional facility managers to ensure that buildings operate efficiently and meet health and safety standards. According to ISO standards, facility management integrates people, place, process, and technology to enhance the quality of life and core business productivity. The complexity of modern buildings with integrated smart systems requires specialized expertise that individual owners often lack. Outsourcing these services allows owners to focus on core competencies while ensuring professional oversight of operational tasks. The recurring nature of facility management contracts provides stable revenue streams for service providers. Furthermore, regulatory requirements for regular inspections and maintenance of fire safety systems, elevators, and HVAC units mandate professional involvement. This mandatory compliance aspect ensures consistent demand regardless of market cycles. Consequently, the essential nature of facility services solidifies their leading position in the property management landscape.

On the other hand, the real estate management segment is predicted to register a promising CAGR of 8.1% over the forecast period in the European market, owing to the increasing focus on strategic asset value enhancement and portfolio optimization. Unlike traditional facility management, which focuses on operations, real estate management involves high-level strategic planning, including acquisition, disposition, leasing strategy, and capital expenditure planning. As per PwC, real estate investors are increasingly prioritizing active asset management to maximize returns in a volatile market. Professional real estate managers provide insights into market trends, helping owners make informed decisions about when to buy, sell, or hold assets. According to JLL, active asset management can increase property values by 15% to 20% through strategic repositioning and renovation projects. This segment involves detailed financial modeling and performance analysis to identify opportunities for value creation. Real estate managers also handle complex lease negotiations, ensuring optimal terms that align with long-term investment goals. The growing complexity of real estate investments, particularly in mixed-use developments, requires specialized expertise in zoning laws and urban planning. Furthermore, the integration of environmental, social, and governance criteria into investment strategies necessitates strategic oversight to ensure compliance and attract capital. Real estate managers coordinate sustainability retrofits and green certifications, which enhance asset appeal. This strategic layer of management is becoming indispensable for institutional investors seeking to outperform market benchmarks. Consequently, the demand for high-level strategic advice drives the rapid growth of the real estate management segment.

By End User Insights

The institutional investors segment accounted for 44.7% of the European market share in 2025. The dominance of the institutional investors segment in the European market is driven by the large scale of their portfolios and the necessity for professional, standardized management to ensure consistent performance. Institutional investors, including pension funds, insurance companies, and sovereign wealth funds, allocate significant capital to European real estate for stable long-term returns. As per the European Institutional Real Estate Association, institutional investment in European property reached 100 billion euros in 2023, reflecting strong confidence in the asset class. These entities require rigorous reporting, compliance, and risk management, which professional property management firms provide. According to MSCI, institutional investors prioritize environmental, social, and governance performance, requiring managers to implement sustainable practices and detailed tracking. The scale of institutional portfolios allows for the implementation of centralized management systems that drive efficiency and cost savings. Professional managers handle complex tasks such as cross-border tax compliance, regulatory reporting, and investor relations, which are beyond the capacity of individual owners. The fiduciary duty of institutional investors mandates high standards of care and diligence, necessitating experienced management partners. Furthermore, the trend towards passive investment strategies increases the reliance on third-party managers to execute operational strategies. This structural dependence on professional expertise ensures that institutional investors remain the primary clients for top-tier property management firms in Europe.

However, the individual investors segment is on the rise and is expected to grow at a CAGR of 7.4% over the forecast period, owing to the rise of accidental landlords and the popularity of buy-to-let investments. Many individuals have become landlords due to inheritance, relocation, or inability to sell properties in stagnant markets, creating a need for professional management assistance. As per Eurostat, the home ownership rate in the EU varies significantly, but rental participation is increasing among younger demographics, providing a steady tenant base for individual landlords. According to the National Residential Landlords Association, in the UK alone, there are over 2 million private landlords, many of whom manage only one or two properties. These accidental landlords often lack the time, expertise, or desire to handle tenant screening, maintenance, and legal compliance themselves. Professional property management firms offer tailored packages for small portfolios, providing peace of mind and reducing administrative burdens. The complexity of tenancy laws, particularly in countries with strong tenant protections, makes professional guidance valuable for avoiding legal pitfalls. Furthermore, the increasing availability of digital platforms has made it easier for individual investors to access professional management services at affordable rates. This democratization of property management services allows individual investors to compete with larger entities in terms of service quality. As the rental market continues to grow, more individuals are entering the landlord sector, driving demand for management support. This trend ensures steady growth for the individual investor segment.

REGIONAL ANALYSIS

United Kingdom Property Management Market Analysis

The United Kingdom occupied the major share of 23.2% of the European market in 2025. The dominance of the UK is mainly due to the UK’s mature rental sector and strong institutional investment. The UK has a long history of private renting with a well-established regulatory framework that supports professional management practices. As per the Office for National Statistics, the private rented sector in England accounts for 20% of all households, creating substantial demand for management services. London remains a global hub for real estate investment, attracting capital from around the world, which requires sophisticated management infrastructure. The introduction of stricter safety regulations, such as the Building Safety Act, has increased the need for compliant management services. According to the Royal Institution of Chartered Surveyors, demand for property management services rose by 15% in 2023 due to regulatory changes. The presence of major global property management firms headquartered in London further strengthens the market. The trend towards build-to-rent developments is accelerating with significant pipeline projects requiring professional oversight. Additionally, the devolved administrations in Scotland and Wales have introduced their own rental reforms, adding complexity that favors professional managers. The robust legal system and transparent market practices make the UK a leader in professional property management standards. This combination of market size, regulatory depth, and institutional activity positions the UK as the dominant force in the European sector.

Germany Property Management Market Analysis

Germany held a promising share of the European property management market in 2025. The growth of Germany in the European market is attributed to the strong rental culture and large institutional portfolios. Unlike many other European countries, Germany has a majority renting population with over 50% of households renting their homes. As per the Federal Statistical Office of Germany, the rental market is highly regulated with strict rent control mechanisms known as the Mietpreisbremse. This regulatory environment necessitates professional management to ensure compliance and avoid legal disputes. The presence of large housing corporations such as Vonovia and Deutsche Wohnen creates a massive demand for standardized management services. According to the German Property Federation, these institutional players manage hundreds of thousands of units requiring efficient operational structures. The energy transition agenda Energiewende is driving extensive retrofitting programs for older building stocks, which property managers coordinate. The technical complexity of these upgrades requires specialized facility management expertise. Furthermore, the strong tenant protection laws mean that eviction processes are lengthy and complex, requiring expert legal handling. Professional managers provide the necessary expertise to navigate these challenges effectively. The stability of the German rental market attracts long-term investors who prioritize professional oversight. This structural reliance on renting and regulatory complexity sustains Germany’s prominent role in the European property management landscape.

France Property Management Market Analysis

France is expected to showcase a prominent CAGR in the European property management market during the forecast period, owing to a large urban population and active real estate investment trusts REITs known as SIICs. The French government actively promotes rental housing through tax incentives, which encourage individual and institutional investment. As per the National Institute of Statistics and Economic Studies, the rental sector in France has grown steadily, with Paris being a key market for high-value properties. The implementation of the Decent Housing Decree imposes strict minimum standards for rental properties, requiring regular inspections and maintenance. According to the French Federation of Real Estate Professionals, compliance with these standards has increased demand for professional management services. The energy climate law mandates energy performance improvements for buildings classified as thermal sieves, driving retrofitting activities. Property managers play a crucial role in coordinating these works and securing grants. The strong legal framework protecting tenants requires managers to handle lease agreements and disputes with precision. Additionally, the growth of student housing and senior living sectors creates niche opportunities for specialized management. The presence of international investors in Parisian real estate further boosts demand for high-quality management services. This combination of regulatory pressure and investment activity drives the growth of the property management market in France.

Spain Property Management Market Analysis

Spain is predicted to hold a notable share of the Europe property management market over the forecast period due to a booming tourism sector and increasing foreign investment in residential real estate. The short-term rental market facilitated by platforms like Airbnb has created a need for specialized management services, including guest coordination and cleaning. As per the National Statistics Institute of Spain, tourism revenues have rebounded strongly, increasing the profitability of short-term lets. Professional managers help owners navigate complex local licensing requirements, which vary by municipality. According to the Spanish Property Registry, foreign buyers account for a significant portion of transactions, particularly in coastal areas and major cities.

COMPETITION OVERVIEW

The competition in the Europe property management market is intense and characterized by the presence of large global firms alongside specialized regional providers. Major players leverage their extensive resources and technological capabilities to offer comprehensive integrated services, while niche firms compete on local expertise and personalized attention. The market is fragmented with numerous small operators serving specific segments or geographic areas. Differentiation is achieved through superior customer service, advanced technology adoption, and sustainability credentials. Regulatory compliance, particularly regarding energy efficiency and data privacy, serves as a key competitive factor requiring significant investment in expertise and systems. Price competition remains relevant, but value-added services such as strategic asset management and consultancy are increasingly important for retaining high-value clients. The rise of PropTech startups introduces new competitive dynamics by offering innovative software solutions that challenge traditional management models. Consolidation through mergers and acquisitions is common as firms seek to achieve scale and broaden their service offerings. Collaboration between traditional managers and technology providers is becoming essential to meet evolving client expectations. This dynamic environment drives continuous improvement and innovation across the sector, benefiting property owners and tenants alike.

KEY MARKET PLAYERS

A few major players of the Europe property management market include

- Yardi Systems, Inc

- AppFolio, Inc

- MRI Software LLC

- SAP SE

- Oracle Corporation

- Trimble Inc

- IBM Corporation

- Accruent

- LLC

- Planon Group

- ARCHIBUS, Inc

Top Strategies Used by Key Market Participants

Key players in the Europe property management market primarily focus on digital transformation to enhance operational efficiency and tenant engagement. Companies invest heavily in property technology solutions such as Internet of Things sensors and artificial intelligence to optimize building performance and reduce costs. Sustainability is a central strategy with firms offering green building certifications and energy management services to comply with European regulations. Strategic acquisitions enable larger firms to expand their geographic reach and service capabilities rapidly. Partnerships with technology startups facilitate the integration of innovative tools for predictive maintenance and automated leasing processes. Customer-centric approaches emphasize personalized services and transparent communication to improve retention rates. Firms also diversify their portfolios by managing emerging asset classes like co-living spaces and logistics hubs. Talent acquisition and training programs ensure staff possess the necessary skills for modern property management. These multifaceted strategies drive competitive advantage and support long-term growth in the evolving European market landscape.

Leading Players in the Europe Property Management Market

- CBRE Group Inc. stands as a global leader in commercial real estate services and investments with a robust presence in the European property management sector. The company manages a diverse portfolio,s including office retail, industrial, and residential assets across major European cities. CBRE recently enhanced its digital capabilities by integrating advanced data analytics into its property management platforms to improve operational efficiency. This technological upgrade allows clients to access real-time insights regarding building performance and tenant satisfaction. The firm also expanded its sustainability consulting services to help property owners meet stringent European environmental regulations. By leveraging its global network, CBRE provides seamless cross-border solutions for multinational corporations. Its commitment to innovation and client-centric strategies strengthens its competitive position. CBRE continues to invest in talent development and technology infrastructure to maintain its leadership status in the dynamic European market.

- JLL is a prominent professional services firm specializing in real estate and investment management with significant influence in the Europe property management market. The company offers comprehensive management solutions that encompass leasing facility management and asset optimization for various property types. JLL recently launched new sustainability initiatives aimed at helping clients achieve net-zero carbon emissions through energy-efficient building operations. These efforts align with the European Green Deal and enhance the value of managed properties. The firm also adopted artificial intelligence tools to streamline maintenance workflows and predict equipment failures proactively. JLL’s strong focus on environmental, social, and governance criteria attracts institutional investors seeking responsible management partners. Its extensive local expertise, combined with global resources, enables tailored solutions for diverse client needs. This strategic approach reinforces JLL’s reputation as a trusted advisor and operator in the European real estate landscape.

- Cushman and Wakefield is a leading global real estate services firm with a substantial footprint in the Europe property management market. The company provides integrated management services for commercial, residential andmixed-usee properties, focusing on maximizing asset value and tenant experience. Cushman and Wakefield recently expanded its PropTech partnerships to implement smart building technologies that enhance operational transparency and efficiency. These innovations allow property owners to monitor energy usage and space utilization in real time. The firm also strengthened its presence in key European markets through strategic hires and localized service offerings. Its emphasis on data-driven decision-making helps clients navigate complex regulatory environments and market fluctuations. Cushman and Wakefield prioritizes sustainability by offering green certification support and retrofitting guidance. These actions demonstrate its commitment to delivering high-quality,y sustainable management solutions. This dedication to innovation and client success solidifies its position as a key player in the European industry.

MARKET SEGMENTATION

This research report on the European property management market has been segmented and sub-segmented based on property type, service type, end user & region.

By Property Type

- Residential

- Commercial

- Industrial

- Retail

- Mixed-Use

By Service Type

- Property Leasing

- Property Maintenance

- Facility Management

- Real Estate Management

- Tenant Management

By End User

- Institutional Investors

- Individual Investors

- Real Estate Developers

- Property Owners

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe