Bill Ackman is the founder of Pershing Square Capital Management. The billionaire hedge fund manager built his reputation through a series of bold, activist campaigns — making him one of the most distinctive figures in modern investing.

Ackman’s investing style hinges on concentrated, long-term bets — often focusing his portfolio among a small number of mispriced companies rather than taking a broad, diversified approach. At heart, Ackman is a value investor — seeking businesses with durable competitive moats, steady cash flow, and the potential for significant earnings expansion.

This philosophy is on full display when it comes to Ackman’s top artificial intelligence (AI) stocks. Currently, roughly 38% of Pershing Square’s capital is held across just three names: Alphabet (GOOGL +1.71%) (GOOG +1.44%), Amazon (AMZN +3.47%), and Meta Platforms (META +2.48%).

Each company is not merely riding the AI wave but actively shaping it. What unites these “Magnificent Seven” members is a rare combination of market leadership and still-reasonable valuations that will reward patient capital.

Image source: Getty Images.

Alphabet

Alphabet has quietly transformed itself from a search and advertising powerhouse into a vertically integrated AI powerhouse. At the core of the company’s strategy are custom chipsets known as Tensor Processing Units (TPUs).

These chips are made with Broadcom and designed to train and deploy Alphabet’s Gemini models. They power everything from AI enhancements in Google Search to new features integrated across Android and Workspace applications. In addition, the same hardware supports Waymo, Alphabet’s autonomous-driving subsidiary.

The idea of vertical integration is a decisive differentiator in Alphabet’s playbook. The company is able to control its own silicon, software models, the data flywheel from billions of daily searches, and the distribution channels that deliver AI services directly to consumers and enterprises.

Meanwhile, Google Cloud Platform (GCP) has become a high-growth engine as businesses migrate AI workloads to the company’s capacity infrastructure. Furthermore, Alphabet’s legacy advertising empire — spanning Google Search and YouTube — stands to benefit from machine learning algorithms that improve targeting and engagement without raising privacy concerns.

Alphabet’s forward price-to-earnings (P/E) multiple sits around 29, and this year’s free cash flow will likely compress sharply as the company pours nearly $200 billion into AI capital expenditures (capex).

Today’s Change

(1.71%) $5.80

Current Price

$344.69

Key Data Points

Market Cap

$4.2T

Day’s Range

$335.39 – $345.30

52wk Range

$147.84 – $349.00

Volume

982K

Avg Vol

32M

Gross Margin

59.68%

Dividend Yield

0.24%

What smart investors understand is that this spending is not a maintenance cost — it is growth capital. Once new data centers, next-generation TPUs, and the full networking backbone come online, Alphabet’s costs should lag the explosive revenue its next wave of AI-driven growth generates.

Amazon

Similar to Alphabet, Amazon’s AI evolution is supported by its own silicon: Trainium and Inferentia chips. These chips give Amazon Web Services (AWS) a structural cost advantage that competitors outsourcing to third-party hardware from Nvidia and Advanced Micro Devices struggle to match.

After years of somewhat mundane growth, AWS has emerged as a premier cloud platform for hosting AI workloads. Within its ecosystem, enterprises can access and deploy AI models more efficiently compared to building this advanced infrastructure from scratch.

Beyond the cloud, Amazon leveraged AI-powered robotics in its fulfillment centers. Furthermore, predictive analytics are used to optimize last-mile delivery, while computer vision systems reduce shrinkage in brick-and-mortar storefronts.

Today’s Change

(3.47%) $8.85

Current Price

$263.93

Key Data Points

Market Cap

$2.8T

Day’s Range

$257.69 – $264.40

52wk Range

$178.85 – $264.50

Volume

2.4M

Avg Vol

52M

Gross Margin

50.29%

On the consumer side, personalized recommendations and dynamic pricing are being used to lift e-commerce margins. Moreover, Prime Video relies on machine learning to improve curated content and insert more targeted advertising campaigns. What makes Amazon particularly attractive is the way its AI initiatives reinforce one another rather than cannibalize its various businesses.

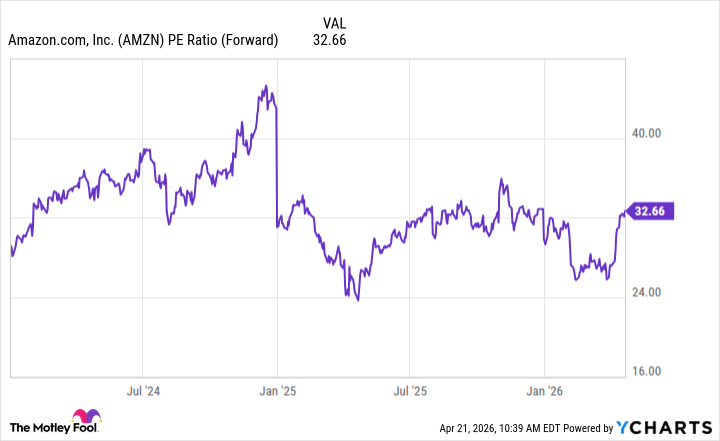

Amazon shares trade at a forward P/E ratio that, when stripped of its higher-growth AWS and advertising segments, looks reasonable. The overall business continues to generate robust free cash flow, which is being used to expand the company’s addressable market into new verticals such as healthcare and satellite broadband.

AMZN PE Ratio (Forward) data by YCharts

I think that Ackman recognizes that the broader market undervalues the durability of Amazon’s integrated ecosystem. Once AI efficiencies are fully integrated and begin flowing through to the bottom line, the stock’s earnings multiple is positioned to rerate higher.

Meta Platforms

Meta’s AI advantages are more acute than Alphabet’s and Amazon’s, but no less important. The company’s main source of AI-driven growth stems from a suite of automated advertising tools called Advantage+.

Advantage+ uses generative AI to create different variations of ad campaigns. It then tests these promotions in real time across Meta’s Family of Apps, including Facebook, Instagram, and WhatsApp. From there, the system optimizes these ads for conversions without requiring marketers to manually manage the campaign. The goal is to drive improvement in return on ad spend for businesses, which, in turn, drives higher platform engagement and increased ad budgets from Meta’s customers.

Since Advantage+ runs on Meta’s proprietary Llama model, the product creates a virtuous cycle: Better ad performance leads to more ad dollars. This capital funds further AI enhancements, which are used to constantly improve performance.

Today’s Change

(2.48%) $16.34

Current Price

$675.49

Key Data Points

Market Cap

$1.7T

Day’s Range

$653.90 – $680.64

52wk Range

$520.26 – $796.25

Volume

1.1M

Avg Vol

16M

Gross Margin

82.00%

Dividend Yield

0.31%

Meta’s valuation profile is especially compelling for a value-oriented investor. The company’s P/E multiple is supported by billions of users around the world and a capital-light business model. Meanwhile, the incremental revenue growth from AI-optimized advertising carries particularly high margins.

Investors like Ackman view Meta as a classic example of a high-quality business that’s temporarily misunderstood. While the market continues to fixate on headline risks around social media regulation, user growth, or infrastructure budgets, some on Wall Street are missing the company’s structural shift toward automated, high-ROI advertising that Advantage+ is already proving at scale.

As adoption deepens, Meta’s ability to compound earnings growth should fuel meaningful valuation expansion in the long run. This setup rewards those who bought when the narrative was still cautious.