The global platinum group metals market has rarely offered investors such a convergence of constructive forces simultaneously. Multi-year supply deficits, a reassessment of electric vehicle adoption timelines, resilient autocatalyst consumption, and climbing jewellery demand have collectively shifted the fundamental outlook for PGMs in ways that were not fully anticipated even twelve months ago. Against this backdrop, Implats robust PGM demand and pricing conditions have created a compelling operational environment for one of the sector’s most integrated producers.

Understanding what is happening beneath the surface of the PGM market requires more than tracking spot prices. It demands a granular view of production economics, refining throughput, inventory management, and the geopolitical variables that shape input availability across southern African operations. Furthermore, PGM supply constraints are becoming increasingly difficult to resolve quickly, which adds structural urgency to current market dynamics.

When big ASX news breaks, our subscribers know first

Why PGM Pricing Has Entered a Structurally Different Phase

The Supply Gap That Is Being Systematically Underpriced

Few commodity markets can credibly claim multi-year structural deficits without facing challenge from new investment cycles. The PGM market, however, presents a genuine supply constraint that is difficult to resolve quickly. New mine development in platinum-bearing geology is exceptionally capital intensive, geologically complex, and subject to long lead times measured in years rather than months.

South Africa’s Bushveld Igneous Complex, which hosts the world’s largest known platinum group metal deposits, presents unique extraction challenges. The Merensky Reef and UG2 Chromitite Layer, the two primary ore horizons exploited by producers including Implats, are relatively narrow-seam, tabular ore bodies. Mining them efficiently at depth requires highly skilled labour, mechanised equipment suited to confined stopes, and sophisticated ventilation infrastructure. This geological reality places a natural ceiling on how quickly production can be scaled upward.

Revised EV Forecasts Are Quietly Reshaping Demand Models

For several years, platinum demand models incorporated a significant headwind from anticipated battery electric vehicle growth. The core thesis was straightforward: BEVs do not require catalytic converters, so rapid EV adoption would erode autocatalyst demand for platinum and palladium over time.

That thesis is being substantially revised downward. Slower-than-expected consumer adoption rates, infrastructure bottlenecks, range anxiety, and affordability barriers have pushed out the timeline for meaningful displacement of internal combustion engines. This recalibration has had a material effect on forward demand projections for PGMs used in emissions control systems. The broader platinum and palladium dynamics at play here are reshaping how analysts model long-term pricing trajectories.

The implications for platinum pricing are significant. Where analysts previously modelled declining autocatalyst demand as an overhanging bearish factor, the revised EV trajectory has reintroduced demand durability into pricing models. Consequently, this shift in market psychology has contributed to price appreciation that many investors were unprepared for.

Jewellery Demand as a Structurally Underappreciated Tailwind

While autocatalysts dominate the narrative around PGM demand, jewellery consumption has quietly re-emerged as a growth vector. Platinum jewellery demand, particularly from Asian markets, has shown resilience that challenges the assumption that this segment is purely discretionary and price-sensitive.

The combination of autocatalyst stability and jewellery growth creates a demand foundation that industrial applications can complement. Industrial uses of platinum span hydrogen fuel cell membranes, pharmaceutical production, petroleum refining catalysts, and electronics manufacturing, each representing steady, non-cyclical consumption pathways. In addition, the broader critical minerals demand picture reinforces why PGMs are receiving renewed institutional attention heading into the energy transition.

| Demand Driver | Trend Direction | Impact on Pricing |

|---|---|---|

| Autocatalyst demand | Stable to rising | Supportive |

| Jewellery consumption | Increasing | Positive |

| BEV penetration revisions (downward) | Reducing substitution pressure | Bullish |

| Industrial applications | Steady growth | Neutral to positive |

| New mine investment | Limited | Supply-constrained |

Implats Q3 2026 Performance: Reading the Numbers Behind the Headlines

Nine-Month Production: Stability Under Operational Pressure

For the nine months ending March 31, 2026, Implats reported total six-element (6E) group production volumes that held stable at 2.56 million ounces. This figure encompasses the full basket of platinum group elements captured in the 6E metric, a measurement that aggregates platinum, palladium, rhodium, ruthenium, iridium, and gold into a single volumetric indicator of total PGM output.

Breaking this figure down reveals the underlying operational dynamics:

- Managed operations produced approximately 2.0 million ounces, largely unchanged year-on-year

- Joint venture production dipped 2% to 395,000 ounces

- Third-party receipts grew 16% to 167,000 ounces, demonstrating the value of Impala Refining Services as a volume aggregator

The stability of total production against a backdrop of operational changes at individual assets represents a meaningful operational achievement. Changes in parameters at Marula and Impala Canada were offset by strengthened momentum at Impala Rustenburg and Zimplats.

Sales Volume Acceleration Confirms Real Demand Pull

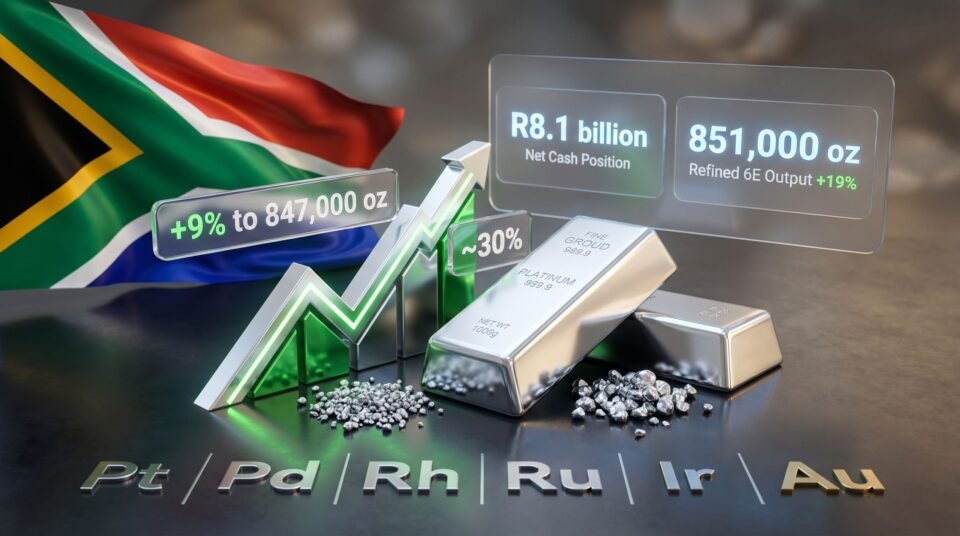

While production stability demonstrates operational consistency, the 9% increase in 6E sales volumes to 847,000 ounces for the third quarter is arguably the more strategically significant data point. Sales volumes that outpace production are a direct indicator of genuine end-market demand absorption rather than producer-driven supply push.

This acceleration in sales is occurring within a pricing environment that has been described as broadly beneficial, with platinum prices having risen approximately 30% in recent months. According to reporting from Mining Weekly, Implats has highlighted these pricing conditions as among the most favourable seen in recent years. The combination of higher volumes and elevated prices creates a multiplier effect on revenue that extends well beyond what either variable would generate independently.

Platinum prices have climbed approximately 30% in recent months, materially enhancing the value of Implats’ strategic inventory position and amplifying free cash flow generation capacity.

The 6E Metric Explained: Why It Matters for Investors

The 6E production metric deserves particular attention because it is frequently misunderstood by investors accustomed to single-metal mining narratives. Unlike gold or copper mining, where a single commodity dominates value, PGM operations simultaneously produce six commercially valuable elements with meaningfully different price profiles.

Rhodium, for example, has historically been the highest-value element in the basket on a per-ounce basis, while platinum and palladium provide volume-weighted price support. The 6E metric therefore represents a blended measure of value creation that is more reflective of actual cash generation than any single-metal equivalent. Producers with higher rhodium grades within their 6E basket typically generate superior margins relative to headline production volumes.

Refining Operations and the Inventory Monetisation Story

Impala Refining Services: A Strategic Asset in a Tight Market

Impala Refining Services (IRS) functions as both a value-chain integrator and a revenue diversification mechanism. Its capacity to process third-party PGM concentrates means that Implats benefits from refining margin on material it does not mine directly.

For the nine-month period, third-party 6E receipts at IRS grew 27% to 52,000 ounces, while refined 6E production rose 19% to 851,000 ounces. These figures signal that processing efficiency has improved and that the third-party pipeline is growing, both structurally positive developments.

A further operational milestone was recorded in mid-April with the successful first matte production at the Furnace 4 rebuild. Smelting furnace availability is a critical bottleneck in PGM processing; the completion of this rebuild removes a constraint and enhances processing capacity heading into the final quarter of the financial year.

Converting Stockpiled Metal to Realised Cash Flow

The period closed with 320,000 6E ounces of excess inventory, a figure that represents significant optionality. In a rising price environment, the timing and sequencing of inventory drawdown becomes a strategic decision rather than a purely operational one.

The period closed with 320,000 6E ounces of excess inventory, down from prior levels, as accelerated sales volumes and refining throughput gains progressively convert stockpiled metal into realised cash flow.

The progressive monetisation of this inventory at elevated prices has material implications for free cash flow generation capacity in the near term. Investors assessing the earnings trajectory of the business should consider the embedded value of this stockpile as a pricing optionality asset rather than simply a balance sheet line item.

Financial Resilience: Net Cash, Shareholder Returns, and Guidance Confidence

A Balance Sheet Built for Uncertainty

Implats holds a net cash position of R8.1 billion, a financial foundation that provides genuine operational flexibility at a time of elevated geopolitical risk and input cost volatility. This liquidity position means the business is not reliant on capital markets to fund ongoing operations or respond to unexpected disruptions.

Shareholder returns of R3.7 billion reflect management’s confidence in the sustainability of current earnings and pricing conditions. Capital returns of this scale, delivered against a backdrop of global uncertainty, represent a meaningful signal of conviction in the forward outlook.

Guidance Reaffirmation as a Market Signal

Management has reaffirmed full-year guidance across production volumes, unit costs, and capital expenditure. In a commodity environment characterised by volatility and execution uncertainty, guidance reaffirmation carries asymmetric informational value. It tells the market not merely that current performance is on track, but that the operational and financial visibility required to make such a commitment with confidence is present.

Management’s explicit reaffirmation of full-year guidance across production volumes, unit costs, and capital expenditure in the context of sustained beneficial pricing represents a meaningful confidence signal for institutional investors assessing PGM sector exposure.

Rising customer demand expectations for the year ahead provide an additional constructive indicator. Where demand is being pulled forward by buyers anticipating tighter supply conditions, the pricing benefits for producers are likely to compound through the remainder of the calendar year.

Operational Deep Dive: Asset Performance Across the Portfolio

Managed Operations: Tonnes Milled Up 10%

At managed operations, tonnes milled increased 10% to 6.49 million tonnes on a milled grade of 3.75 grams per tonne. This grade profile is consistent with mining across the Bushveld Complex, where Merensky Reef grades typically range between 3.5 and 6 g/t 6E depending on reef type and geological continuity.

Notwithstanding the improvement in mined and milled volumes, 6E production at managed operations retraced 3% to 588,000 ounces, while JV production rose to a 1% higher 122,000 ounces. The volume increase without a corresponding proportional uplift in output reflects grade variability and processing yield factors that are characteristic of reef mining environments.

Impala Canada: Understanding the North American Divergence

The North American operation delivered results that diverged from the southern African performance trajectory. Key metrics for the period included:

- Milled throughput down 4% to 680,000 tonnes

- Milled head grade declined 9% to 2.85 g/t

- 6E concentrate production fell 13% to 52,000 ounces

The head grade decline is a particularly important indicator. In hard rock mining, head grade reflects the average concentration of payable metal in ore delivered to the mill. A 9% decline in head grade at Impala Canada suggests the operation is accessing lower-grade zones within its current mining sequence, a geological rather than purely operational dynamic. This has flow-through consequences for concentrate production that cannot be fully offset by increasing throughput alone.

| Production Category | Volume (9 Months to March 31) | Year-on-Year Change |

|---|---|---|

| Total 6E Group Production | 2.56 million oz | Stable |

| Managed Operations | ~2.00 million oz | Largely unchanged |

| Joint Venture Production | 395,000 oz | -2% |

| Third-Party Receipts | 167,000 oz | +16% |

| 6E Sales Volumes | 847,000 oz | +9% |

The next major ASX story will hit our subscribers first

Geopolitical Risk Management and Supply Chain Resilience

Middle East Tensions and Critical Consumables Exposure

South African PGM producers face a distinctive geopolitical risk profile. While their ore bodies and primary processing infrastructure are domestically located, certain critical consumables and spare parts required for smelting and refining operations have supply chains that extend through global logistics networks exposed to geopolitical disruption.

In response to elevated tensions in the Middle East, Implats has taken proactive steps to buffer the availability of critical consumables and spares at its operations. This forward-looking inventory management approach is designed to maintain operational continuity even if supply chain disruptions extend beyond initial expectations. However, the mining energy transition also introduces new dependencies on global supply chains that producers must actively manage.

| Scenario | Probability Assessment | Likely PGM Price Impact |

|---|---|---|

| Continued Middle East tension, no supply disruption | High | Mildly supportive |

| Supply chain disruption to critical consumables | Moderate | Negative short-term cost pressure |

| Broader commodity market risk-off event | Low-moderate | Mixed (safe-haven demand vs. industrial slowdown) |

| Resolution of tensions, demand normalisation | Moderate | Consolidation at current pricing levels |

Safety Performance: Governance, Metrics, and the Human Reality

Injury Frequency Rate Improvements Signal Operational Discipline

Safety performance metrics have become integrated into ESG assessments of mining companies, with injury frequency rate improvements functioning as leading indicators of operational governance quality. For the nine-month period, Implats recorded meaningful improvements across both primary safety metrics:

- Lost-time injury frequency rate improved 27% to 2.83 per million person-hours worked, down from 3.89

- Total injury frequency rate improved 37% to 5.68 per million person-hours worked

These are statistically significant improvements, not incremental gains. A 37% reduction in total injury frequency reflects genuine operational culture change rather than statistical variation. Furthermore, the broader mining sustainability transformation underway across the sector reinforces why safety and governance metrics are increasingly central to institutional investment decisions.

Fatalities at Impala Rustenburg: Acknowledging the Human Cost

Despite the measurable improvement in aggregate safety statistics, the period was marked by the tragic loss of two workers at Impala Rustenburg. This human reality sits alongside the operational and financial narrative as an unequivocal reminder of the inherent risks that define underground mining.

Implats has expressed its determination to eliminate fatalities and life-changing injuries, and the company has acknowledged the losses directly. For investors assessing ESG credentials, the transparent reporting of fatalities alongside safety improvement metrics represents appropriate governance disclosure rather than selective presentation.

Frequently Asked Questions: PGM Markets and Implats Performance

What is driving robust PGM demand in 2026?

The combination of stable autocatalyst consumption, revised BEV adoption timelines reducing substitution fears, growing jewellery demand, and steady industrial applications has created a structurally supportive demand environment. Constrained new mine supply amplifies the pricing impact of these demand factors, and Implats robust PGM demand and pricing signals confirm this structural shift is well underway.

What does the 6E production metric include?

The 6E metric captures six platinum group elements: platinum, palladium, rhodium, ruthenium, iridium, and gold. It provides a comprehensive measure of total PGM output value rather than isolating a single metal, and is the standard reporting metric used by South African PGM producers.

How does declining BEV adoption affect platinum demand forecasts?

Lower-than-expected BEV penetration means internal combustion engine vehicles continue to require catalytic converters containing platinum and palladium for longer than previously modelled. This has removed a significant bearish headwind from platinum demand forecasts and contributed to upward price revisions.

What is Impala Refining Services and why is it strategically important?

IRS processes both Implats-mined material and third-party concentrates, generating refining margin on volumes the company does not mine directly. It diversifies revenue, increases throughput utilisation, and enhances the value chain integration of Implats’ operations.

What are the key risks to continued PGM price strength?

Primary risks include a global economic slowdown reducing industrial and automotive demand, an acceleration in BEV adoption beyond current revised forecasts, supply chain disruptions increasing input costs without corresponding price offsets, and geopolitical developments creating broader commodity market risk-off sentiment.

Key Performance Indicators: Structural Strength in Summary

| Key Performance Indicator | Result | Strategic Significance |

|---|---|---|

| Platinum price appreciation | ~30% recent gain | Amplifies inventory and cash flow value |

| 6E sales volume growth | +9% to 847,000 oz | Demand pull confirmed |

| Net cash position | R8.1 billion | Balance sheet resilience |

| Shareholder payout | R3.7 billion | Confidence in sustained earnings |

| Lost-time injury rate improvement | -27% to 2.83 | Operational governance strength |

| Refined 6E production | +19% to 851,000 oz | Processing efficiency gains |

The convergence of Implats robust PGM demand and pricing conditions with a structurally constrained supply environment creates an unusual alignment of fundamental factors. Rising prices, expanding sales volumes, a strong net cash position, improving refining throughput, and reaffirmed guidance collectively support the case that the current period of PGM market strength reflects genuine structural change rather than cyclical noise.

For investors considering exposure to PGM markets, the combination of supply constraints, demand durability, and inventory optionality embedded in the sector’s leading producers represents a framework that warrants serious analytical attention. As Business Day’s coverage of the third-quarter results highlights, strong PGM demand is increasingly being recognised as a structural rather than cyclical phenomenon.

Disclaimer: This article is intended for informational purposes only and does not constitute financial advice. Commodity markets are subject to significant volatility and uncertainty. All forecasts, price projections, and scenario analyses referenced herein are speculative in nature. Past performance and current pricing trends do not guarantee future outcomes. Readers should conduct independent research and consult qualified financial advisors before making investment decisions.

Further Exploration: Readers seeking additional context on platinum group metals market dynamics and the broader South African mining sector can explore related industry coverage available through Mining Weekly at miningweekly.com. This resource provides ongoing reporting across PGM production, pricing trends, and operational developments across the sector.

Want to Stay Ahead of the Next Major ASX Mineral Discovery?

Discovery Alert’s proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly converting complex data across 30+ commodities into clear, actionable investment insights for both short-term traders and long-term investors. Explore Discovery Alert’s dedicated discoveries page to see how historic mineral discoveries have generated substantial returns, and begin your 14-day free trial today to secure a market-leading edge before the broader market catches on.