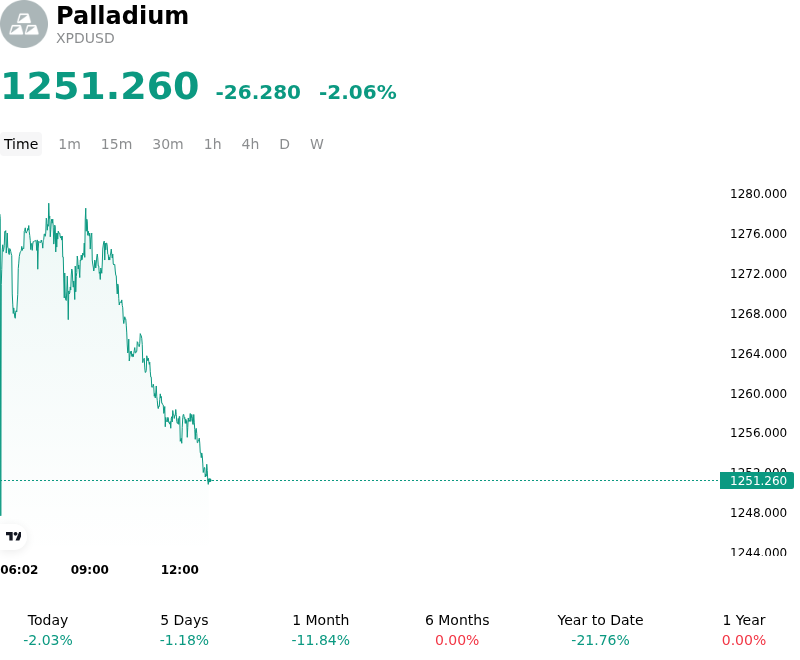

Palladium (XPDUSD) is down 2.06% at Jun 19 01:00(ET), now at $1251.26, with a 7-day down of 2.41%.

The recent downward pressure on palladium is primarily driven by a significant hawkish shift in macroeconomic policy expectations and an easing of geopolitical risk premiums, which have collectively altered near-term demand and investor positioning.

The primary catalyst behind the selloff is the Federal Reserve’s updated monetary policy guidance. Although the Federal Open Market Committee kept interest rates steady, its newly released Summary of Economic Projections and updated dot plot delivered a hawkish surprise. A majority of policymakers now signal at least one more rate hike before the end of the year, alongside upward revisions to inflation expectations. This indicates that monetary policy will remain restrictive for longer. The resulting appreciation of the US dollar and rise in global bond yields have significantly diminished the appeal of non-yielding precious metals, sparking broad liquidations across the complex.

On the geopolitical front, a cooling of international tensions has further stripped away the risk premium supporting palladium. The signing of a preliminary peace agreement between the United States and Iran aimed at stabilizing the Middle East and reopening the Strait of Hormuz has successfully mitigated supply disruption fears. While the normalization of global shipping routes is fundamentally positive for industrial supply chains, the actualization of this peace agreement prompted a swift unwinding of defensive safe-haven holdings, triggering capital outflows from metals.

From a demand perspective, the metal continues to face structural headwinds, particularly within the automotive sector, which accounts for the vast majority of global palladium consumption. Ongoing shifts toward alternative powertrain technologies and the substitution of palladium with more cost-effective platinum in catalytic converters have capped long-term demand expectations. Although lower energy prices and resolved shipping bottlenecks could support broader automotive manufacturing volumes in the long run, the immediate risk-off sentiment and rising borrowing costs are currently curbing industrial purchasing activity and keeping physical buying muted.

Ultimately, the combination of a strengthening US dollar, elevated interest rate expectations, and a declining geopolitical risk premium has prompted a repricing of the palladium market. Investors continue to monitor global manufacturing purchasing managers’ indexes and central bank rhetoric to gauge whether this weakness reflects a temporary correction or a deeper acceleration of structural surpluses.

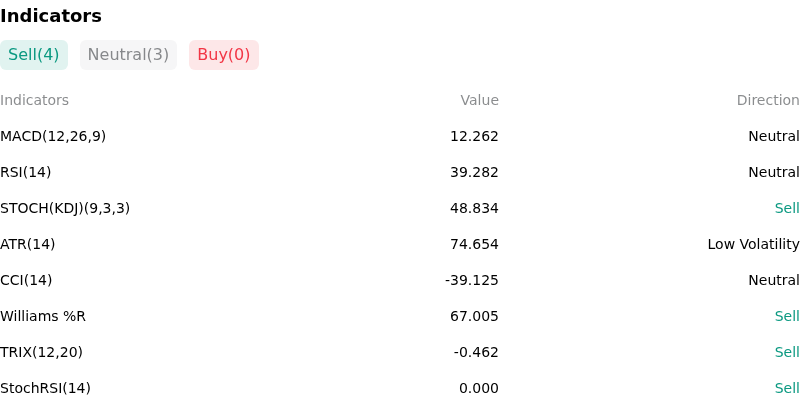

Technically, Palladium (XPDUSD) shows a MACD (12,26,9) value of 12.262, indicating a neutral signal. The RSI at 39.282 suggests neutral condition and the Williams %R at 67.005 suggests sell condition. Please monitor closely.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.