Global equities moved higher for the week amid optimism around a potential second round of US-Iran talks and a 10‑day ceasefire between Israel and Lebanon. Earnings season began strongly, with a few major US banks reporting solid Q1 results. US PPI for March came in at 0.5% versus 1.1% expected. Eurozone inflation for March was revised up to 2.6%, due to surging energy prices caused by the Middle East conflict. UK industrial production beat expectations, rising 0.5% on strength in mining and quarrying. In China, Q1 GDP grew 5% year on year, supported by strong exports of electrical and mechanical goods.

Looking ahead to this week, investors will be keeping a close eye on negotiations between the US and Iran. Earnings season continues, with Amazon & Tesla among the names reporting. US retail sales data is due out, with investors watching for signs that weak consumer sentiment is translating into softer spending. In Europe, preliminary April PMIs will be released. The UK will publish inflation and labour market figures. In Asia, Japan’s inflation data will be released, and the People’s Bank of China is expected to keep interest rates unchanged.

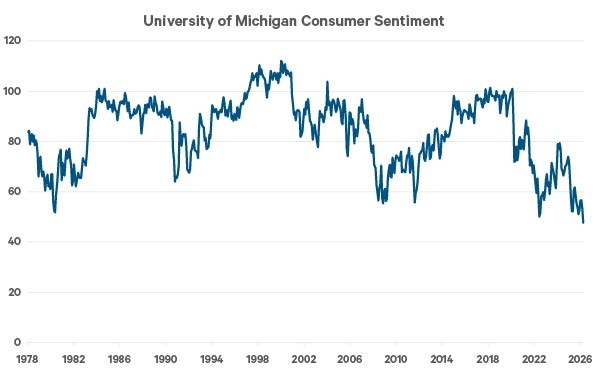

Chart of the moment – The only way is up?

Source: Bloomberg as of 17/04/2026.

- US consumer sentiment decreased by more than 11% in early April, according to the University of Michigan Survey of Consumers, dropping to a 76-year low, below levels seen in the Great Financial Crisis and the COVID-19 pandemic.

- The decrease is attributed to almost solely to the war in Iran, which has reignited inflation fears among consumers amid surging energy costs.

- Memories of the affordability crisis in 2022 are likely exacerbating the concerns of Americans, as year-ahead inflation expectations in the survey rose from 3.8% to 4.8%.