The US and European private credit markets have been one of the significant success stories of asset management over the last decade.

Originally a source of financing for mid-market companies that could not raise funds elsewhere, private credit has grown into a serious and credible competitor to both traditional bank debt and the liquid markets (ie. broadly syndicated loans and high yield corporate bonds) – something seemingly fanciful just a few years ago. Now, private credit players are regularly financing entire multi-billion-dollar debt structures1.

The most recent wave of macro challenges – inflationary pressure and war in Ukraine – have been no exception to the trend. As liquid market activity fell significantly, private credit was able to step up and step in. The combination of locked-up capital and experienced managers able to discern the appropriate credit opportunities, has meant private credit is taking even more share from banks and the liquid markets3.

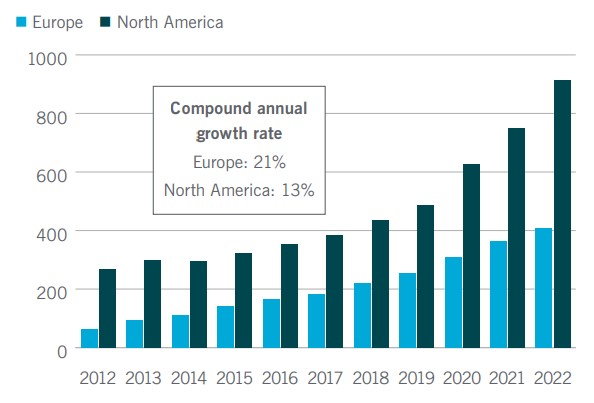

Private credit AUM growth ($bn)

Managing strong growth

Even as private credit enters a new phase of “liquid market substitution”, we believe the risk/return profile of the asset class in the US and Europe remains attractive4. Private credit managers tend to extract better terms and pricing with more diligence in this new environment than their liquid market counterparties.

The scaled, established managers in both regions seem best-placed to benefit from these trends. To be a counterparty to top-tier private equity, a private credit manager needs an established track record of providing finance combined with significant fund sizes.

As a result, we see the mid-to-upper end of the private credit market as the most attractive place to be – it typically gives access to high-quality investment opportunities with reduced competition.

Undoubtedly, the industry faces challenges. While some macro worries have subsided, the global economy is not ‘out of the woods’ yet. Notably, it is clear that interest rates may remain elevated for at least another year or two, putting stress on borrowers whose interest costs are suddenly ballooning. There will certainly be difficult conversations between lenders and borrowers as to how the capital structure can be made sustainable.

Ultimately, the quality of the underlying credit will determine fund performance – capital structure issues are easier to fix when business performance is strong. We take comfort that private credit is exposed to more defensive industries than the market at large, has stronger structural protections than the liquid markets5, and its managers can often take action more decisively than a large club of disparate lenders ever can.

Tackling US and European market dynamics

While the US and European markets share a large number of similarities, structure and outlook, differences do remain. There is the multi-jurisdictional nature of Europe, for example, compared with the more homogeneous US legal system.

Yet we believe there are several reasons why private credit is well placed to overcome the challenges that both the US and European economies will face:

- Direct lenders continue to grow and take market share from banks. Relative market share of banks now accounts for less than 25% of all financing across U.S. and Europe. Private credit can offer reliability and flexibility when banks may retrench from lending activities or when liquid fixed income markets may be restricted from offering new financing solutions – particularly in periods of market volatility.

- The evolution of the private credit market favors the largest managers. Over the last 10 years, the top-5 fund managers in both the U.S. and Europe raised more than 25% of private credit capital6. Larger fund sizes may allow access to better, larger deals with top-tier sponsors.

- Deal volumes are benefiting from a structural change in the direct lending and liquid markets. Private credit deal volumes are on an upward trajectory while liquid market primary issuance has been variable.

- There is material runway for growth in private credit in the years to come. We believe private credit is well positioned to take a material share of the $370bn of liquid market issuance that will be seeking refinance over the next several years7.

- Private credit has delivered attractive returns over the long term. On a risk-adjusted basis, direct lending is a particular stand-out performer, with materially lower risk and higher returns than its liquid market counterparts.

Attractive investment characteristics fuelling growth

The growth of private credit as an asset class has been largely driven by the increased demand by borrowers for the reliability and flexibility that private credit offers. This is particularly true in periods of market volatility, when banks continue to retrench from their lending activities and the liquid fixed income markets are highly restricted in their ability to offer new financing solutions.

Similarly, investors have continued to increase allocations to private credit. They are attracted by the premium absolute returns the asset class can generate versus the liquid markets, as well as by the typically lower risk profile due to less cyclical underlying businesses, often better structural and legal protections, and the lower volatility of long-term debt structures.

Put simply, private credit has proven its resilience through difficult economic environments, is of a size and scale where it represents a meaningful and attractive financing alternative to the liquid markets. We believe the asset class will continue to demonstrate strong growth for many years to come.

To learn more about Nuveen’s private capital platform, please click here.

Sources

1 – Platt, E and Clarfelt, H 2023, ‘Private credit funds step in for companies facing mountains of debt’, Financial Times, 13 Oct 2023, https://www.ft.com/content/7c4a994b-024e-4e6e-992c-7409de8943ed

2 – Deloitte Alternative Lender Deal Tracker Q4 2022.

3 – LCD Quarterly European Leveraged Lending Review: Q1 2023

4 – Q1-23 Cliffwater Report on US Direct Lending.

5 – Leveraged Loan: LCD Research – S&P Global Market Intelligence, S&P European Leveraged Loan Index components as of September 2023 – sector categorisation through Arcmont internal analysis; Direct Lending: Deloitte Alternative Lender Deal Tracker – Spring 2023 (deals during 2022).

6 – Data source: Preqin, September 2023.

7 – Data source: PitchBook LCD, as of Q1 2022.

Important Information

Past performance is not a guide to future performance. Investment involves risk, including loss of principal. The value of investments and the income from them can fall as well as rise and is not guaranteed.

Private equity and private debt investments, like alternative investments are not suitable for all investors given they are speculative, subject to substantial risks including the risks associated with limited liquidity, the potential use of leverage, potential short sales, concentrated investments and may involve complex tax structures and investment strategies.

This information does not constitute investment research as defined under MiFID.

Nuveen, LLC provides investment solutions through its investment specialists.

GAR-3300293PF-O1223W

¬ Haymarket Media Limited. All rights reserved.