Processing Content

- Key insights: Banks are making pragmatic pivots with blockchain, but is that enough?

- What’s at stake: There is a persistent narrative around stablecoin payments that overstates its impact and scale.

- Forward look: Stablecoins will continue to further try to embed themselves within the payments ecosystem, and without guardrails (like technical standards and clear insight into payment details), new inefficiencies and dubious payment practices will follow.

Banks may be putting their historically paramount role in payments at risk if they don’t take more proactive steps to show leadership in the transition to on-chain finance.

Blockchain-based fintechs have already gained a foothold in trading and institutional investing and have their eyes on payments. While the role of digital assets in payments is less rooted, there is a persistent narrative around stablecoin payments that

Payment volumes referenced are often not fully reflective of

Momentum from banks is mixed, and ongoing uncertainty remains, fueled by cybersecurity and run risks, alongside regulatory shifts surrounding the implementation of the

Banks should consider taking more of a leadership role in the stablecoin narrative in two immediate ways:

- Establish Trusted Ledger Frameworks: By turning their own deposits into tokens, serving as custodians, and defining the rules of the road for others, banks ensure the integrity of payment transfer and maintain the “checks and balances.” This prevents the fragmentation of the money supply and ensures that digital payments are backed by regulated, liquid reserves.

- Spearhead Cross-Industry Technical & Compliance Standards: By setting the guardrails for how payment details are shared across blockchains, banks can play an active role in standard-setting groups (e.g., ISO, X9, and NIST) that will determine how payments and stablecoins develop, but also how, and if, they interoperate. As architects of the payment systems, banks should help develop unified interoperability protocols that bridge traditional cores with an on-chain environment.

Where banks are today

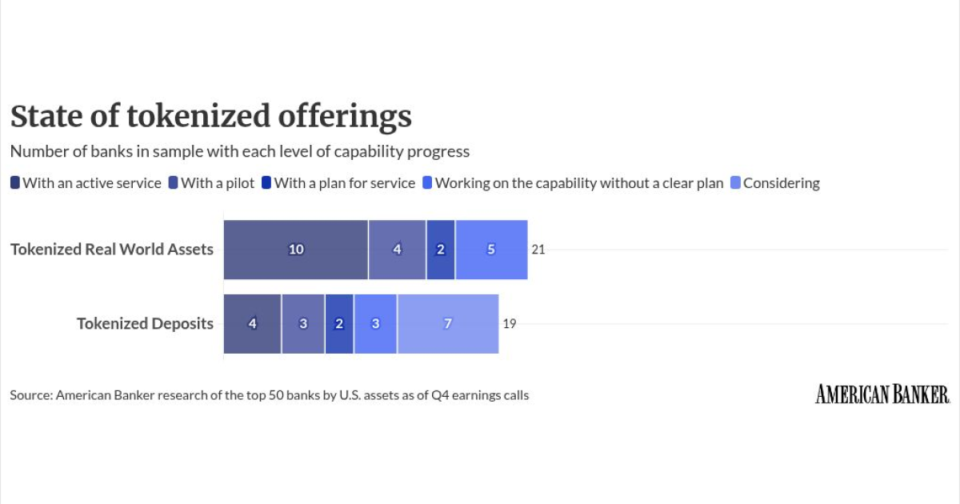

The largest financial institutions are prioritizing blockchain-based products that can be applied under traditional frameworks, like tokenization and custodianship of digital assets, according to American Banker’s recent analysis of the public statements and filings in the last two quarters of 2025.

Tokenized deposits and real world assets can be federally insured and yield interest,

The gap between bank interest and bank action is most visible in the stablecoin issuance market. The number of banks considering a public stablecoin jumped from two to eight in Q4, a fourfold increase, yet only one bank reported an active service. While questions around interoperability and usage volume remain, if banks continue to linger on the sidelines waiting for resolution, nonbank stablecoin issuers will determine how the market takes shape

It’s possible that one of the incumbent stablecoins will become the dominant coin for payment transactions. The safety, security, and soundness of the U.S. payment system could falter if the dominant coin does not reflect those attributes. While Circle’s USDC has made strides to be compliant and risk-averse, Tether remains a black box in many ways, and has faced a slew of challenges around lax safeguards, illicit finance, sanction violations, money laundering, and opaque business practices. If western markets, for whatever reason, did increasingly hold deposits and move money using Tether, it can lead to negative consequences to the U.S. payment system, unless banks are proactive now to be leaders, or at least actively engaged, in the space.

Quarter over quarter we saw less movement by banks in payment specific use cases. Banks implementing blockchain technology into existing processes plateaued in the last two quarters of 2025. Actual implementation for many of these capabilities remains in a holding pattern. Wholesale payment services, which have the highest numbers, remained flat throughout the latter half of 2025. Seven banks have active wholesale payments using blockchain tech, namely to support internal intrabank transfer of funds. Mentions of active cross-border DLT services saw virtually no growth quarter over quarter.

We’ve seen large banks leverage blockchain for wholesale payments and cross-border payments as a way to build volume within a bank’s network while testing the operational feasibility of the blockchain. A notable example includes JP Morgan’s partnership with Kinexys, which used a blockchain system as a payment rail and deposit account ledger, allowing clients to move the deposits held at JP Morgan. It’s a way to address frictions associated with cross-border and wholesale payments by supporting same day and 24/7/365 payments, but still utilizes traditional legacy systems and customer accounts that are subject to JP Morgan’s oversight.

By leveraging their position as the trusted ledger, banks have a unique opportunity to provide the stability that decentralized ecosystems currently lack, and lead how this tech is integrated. Banks are uniquely positioned to shape how these technologies develop into traditional payments, in a way that limits risk, fragmentation, and disruption to clients and the end-user experience.

To do or not to do: a brief evaluation of consequences

Banks are deeply entrenched in the global financial ecosystem; they have scale, access to payment rails, technical standards implemented, regulatory oversight, and name recognition. They are integral in the movement of money, and support a U.S. payment system that is efficient, reliable, and resilient. While stablecoins play a very specific and currently limited role, the decision banks need to make now is how they’ll be involved in how that future develops. Not being involved risks unregulated entities determining how these spaces develop, grow, and become utilized by consumers. There is value in ensuring proper checks and balances are met when it comes to stablecoin payments.

As nonbank stablecoins continue to gain traction and seek access to Federal Reserve infrastructure, the distinction between traditional and on-chain finance will continue to blur. Banks possess the unique combination of scale, regulatory expertise, and consumer trust necessary to bridge these two worlds. Innovation without trust is a wasting asset, and banks can either help design the new payment landscape or potentially be forced to settle for rules and protocols they had no say in.