Introduction

The Government has announced the FY2026/27 Land Sale List (“the List”) with nine residential sites capable of supplying over 6,500 flats. Three of these sites are bundled with deliberate policy to seed an “industry‑oriented” Northern Metropolis (NM) within the Pilot Area in the Hung Shui Kiu/Ha Tsuen (HSK/HT) New Development Area as one Large scale Land Disposal tender, meaning that in effect only seven residential tenders are likely to appear in the pipeline this financial year — a historically lean year for direct disposals by the Government. Budget guidance for the land revenues by the government is about HK$18 billion for FY26/27 (including all other receipts from private treaty grants and lease modifications in addition to land sales), as compared to an estimated HK$17.5 billion for FY25/26, points to a more market‑realistic stance. The signal is that the government will orderly supply land with more reasonable pricing expectations.

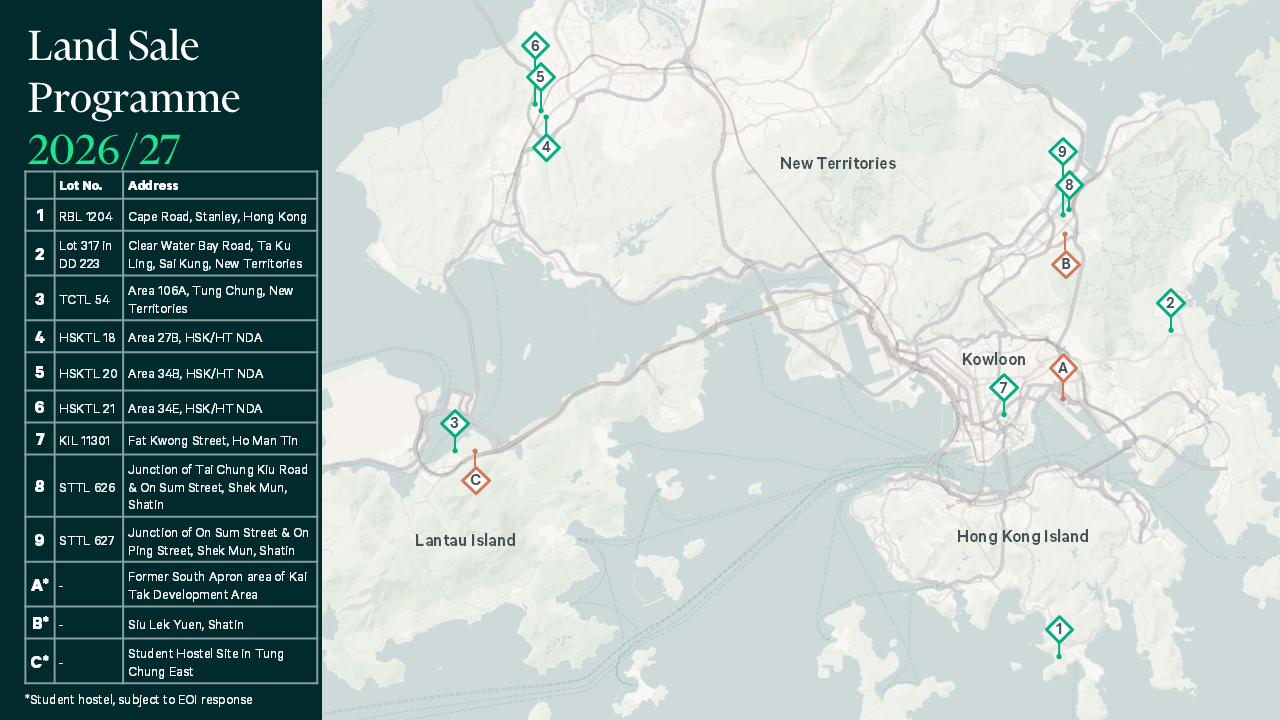

The tender sites at a glance

Based on the Government’s announcement and press briefing, the nine sites comprise as listed in the table below.

|

# |

Location |

Lot No. |

Use |

Est. No. of Units |

Remarks |

|

1 |

Clear Water Bay Road, Ta Ku Ling, Sai Kung |

Lot 317 in DD 223 |

Private Residential |

330 |

Rolled Over from FY2025-26 |

|

2 |

Cape Road, Stanley |

RBL 1204 |

Private Residential |

640 |

Rolled Over from FY2025-26 |

|

3 |

Area 106A, Tung Chung |

TCTL 54 |

Private Residential |

990 |

Rolled Over from FY2025-26 |

|

4 |

Area 27B, HSK/HT NDA |

HSKTL 18 |

Private Residential |

1,584 |

Tender in Progress |

|

5 |

Area 34B (East), HSK/HT NDA |

HSKTL 20 |

Private Residential |

606 |

Tender in Progress |

|

6 |

Area 34E (North), HSK/HT NDA |

HSKTL 21 |

Private Residential |

931 |

Tender in Progress |

|

7 |

Fat Kwong Street, Ho Man Tin |

KIL 11301 |

Private Residential |

250 |

OZP Amendment in Progress |

|

8 |

Junction of Tai Chung Kiu Road and On Sum Street, Shek Mun, Shatin |

STTL 626 |

Private Residential |

870 |

Rezoning in Progress |

|

9 |

Junction of On Sum Street and On Ping Street, Shek Mun, Shatin |

STTL 627 |

Private Residential |

450 |

Rezoning in Progress |

Figure 1: Hong Kong’s FY2026/27 Land Sale List

Figure 2: Location Map

Source: Lands Department, CBRE

(1) Long running rollover

Clear Water Bay Road, Ta Ku Ling, Sai Kung; a large, low rise context residential site with lots of development challenges

The Ta Ku Ling site on Clear Water Bay Road (Lot 317 in DD223) remains one of the longest standing rollover cases on the List, having reappeared in every programme since 2023 after rezoning from “Green Belt” to “Residential (Group C)7” without progressing to tender. Its repeated deferral is rooted in a combination of planning complexity, site specific constraints, and development obligations that make it markedly more challenging than conventional urban residential plots. It spans a substantial 2.55 ha of land area and sits within a hillside squatter area with low rise, semi-rural context, 30% of which is designated as a non-building area (NBA) under the Outline Zoning Plan (OZP). The OZP divides the site into two portions: Area A, which permits residential development subject to a height restriction of 7 storeys (24m) but also requires social welfare facilities, including a GFA-exempted Residential Care Home for the Elderly cum Day care Unit; and Area B, designated strictly as NBA where no development is allowed except for the provision and future maintenance of new access roads connection with Clear Water Bay Road, and pedestrian related facilities at the developer’s own expense.

These development conditions significantly constrain the project’s design flexibility, heighten the construction costs, extend development timelines, increase capital risk and thus negatively influence the financial feasibility. The surrounding built form, dominated by bungalow style villa clusters such as Las Pinadas, Green Villa and Celestial Villa, further reinforces the area’s low density suburban character, suggesting that any eventual scheme would likely skew toward larger units rather than high yield mass-market residential, which again lowers the investment appetite and narrows the potential bidder pool.

Given these factors, market interest is expected to remain highly selective, with bidders adopting a long-dated pricing horizon consistent with the area’s positioning as a suburban lifestyle enclave rather than a mainstream urban product. The site will continue to be price sensitive, and its tender viability will hinge on property cycle timing, cost of capital levels, and developers’ appetite for risk exposure to complex project planning and infrastructure commitments. Until these variables align, the Ta Ku Ling site is likely to continue appearing as a rollover item — a well-located suburban plot close to HKUST campus but commercially intricate opportunity awaiting the right window for disposal.

(2) Rolled over site with withdrawal history

Cape Road, Stanley; a large luxury residential site, previously withdrawn by the Government when tender bids failed to meet the reserved price back in January 2023 with an early signal of developers’ luxury risk aversion

With the stamp duty on ≥HK$100m luxury units raised recently, and amid today’s record construction costs and still elevated financing costs, we expect lukewarm participation and disciplined pricing by those developers with stronger cashflows and committed to long-term capital investment if the site is launched in 1H2026 — even though large Stanley sites are intrinsically scarce.

(3) Rolled over site with market tested appetite

Area 106A, Tung Chung; a harbourfront residential site expected to be released in the first quarter of the financial year, providing around 990 flats, and benefiting from the future Tung Chung East Station, scheduled for completion by end 2029

Confidence in bringing this site forward has been strengthened by the successful tender of Area 106B nearby, awarded to Sun Hung Kai Properties in February 2025 for HK$602 million, equating to an accommodation value of HK$1,501 per sq.ft. This transaction provided a good price benchmark and demonstrated that developers remain willing to pursue well located, mid-sized projects in Tung Chung.

Leveraging this improved market signal after calibrations from previous tender failure in September 2023, the Government is now front loading another right sized, harbourfront plot that aligns with prevailing market appetite. The move also fits neatly within the broader Tung Chung New Town Extension narrative, as well as the established practice of opening the year with absorbable, mass market residential sites that can attract healthy participation under current conditions.

(4,5,6) Northern Metropolis Agenda driven

Pilot Area in the HSK/HT NDA; 3 residential sites within the 10 hectare pilot area tender package that also includes three Enterprise & Technology Park (E&TP) sites

These three residential sites will be disposed as a single tender together with the E&TP sites. This is the first Large scale Land Disposal in a new development area under a two envelope tender evaluation which gives as high as 70% weighting to non-premium (technical) proposal focused on industry/E&TP development, and 30% weighting to premium (financial) proposal, with facilitative terms (e.g. staged premium payment, independent land leases, 7 year building covenant). This is not just a land sale — it’s a policy instrument to anchor strategic industries and accelerate Northern Metropolis delivery through integrated development. But the investment reality is higher capital and technical thresholds, for which most local mass residential players will likely seek industry partners to cover E&TP obligations and reduce project risk. Capable bidders will be limited.

(7,8,9) Rezoning and late in year candidates

Ho Man Tin & Shek Mun; 3 newly added residential sites subject to statutory planning procedures

Among the list, the Fat Kwong Street site in Ho Man Tin and the two Shek Mun sites in Sha Tin stand out as the key urban conversion opportunities still undergoing statutory planning procedures, making them unlikely to be tender ready until the latter part of the financial year. However, these urban sites are more risk-balancing in scale and complexity which help anchor recovering market sentiment and absorption.

For the Fat Kwong Street site, the Town Planning Board completed its rezoning to Residential (Group B)4 in late 2025. Planning documents indicate a mid-density scheme of around 250 units, along with Government required GIC provisions including a neighbourhood elderly centre and an integrated community centre for mental wellness, and the floor space for these facilities may be exempted or disregarded when calculating the maximum plot ratio. Situated within a mature and well served urban neighbourhood, the site possesses strong fundamentals and broad mass market residential appeal once the remaining planning amendments are finalised and tender is out.

Meanwhile, the two Shek Mun sites in Sha Tin continue to advance through their respective rezoning steps, shifting from Commercial (1) zoning to residential use—potentially Residential (Group A) as proposed by the Government. With reference to nearby residential zones applying a 6.0x plot ratio, the sites are expected to yield approximately 775,000 sq.ft. of GFA and about 1,320 units. Previously highlighted in land sale commentaries as strategic urban infill opportunities, these sites benefit from the area’s established infrastructure and transparent land value benchmarks, both of which should underpin healthy developer interest when they ultimately reach the market.

Supply flow and pacing: “Volume stable, market paced” in action

The Government is explicitly keeping supply stable while pacing disposals to market. The message from the List sits alongside Budget guidance that no general commercial sites will be sold this year (given still high vacancy rates) and that total private housing land supply could reach ~22,580 flats in 2026/27 when MTR/URA/private sources are included. This is consistent with a “volume stable, market paced” stance we have advocated.

Our view remains: stick to a transparent, quarterly cadence, even when sentiment is soft. That is how to avoid a structural undersupply later and to give developers clearer capital planning visibility.

Market Commentary

The Government’s latest Land Sale Programme presents a strategy that, in many ways, mirrors the market realities we have been observing on the ground. With sentiment still cautious — particularly in the luxury segment — the administration’s emphasis on mid-sized, urban located, and more absorbable sites reflects a pragmatic reading of developers’ current risk appetite. Mass-market residential remains where liquidity is. The decision to potentially launch the year with a well-located, waterfront site in Tung Chung New Town Extension (Area 106A) exemplifies this approach: a mass market, transit linked project that aligns with more resilient end user demand and the sector’s preference for manageable development sizes. This is fully consistent with the Government’s stated intent to pace supply in line with market absorption capacity.

At the same time, the three residential sites within the tender package of Hung Shui Kiu/Ha Tsuen (HSK/HT) Pilot Area clearly signal the Government’s imperative agenda in the new development areas. The bundled two envelope structure — weighting 70% of the assessment on non-premium proposal tied to innovation and industry development — positions the Northern Metropolis not just as another major source of housing supply, but as a new strategic economic engine. While this strategy is ambitious, the tender package was calibrated based on market feedback after previous invitation for expression of interest (EOI) by the Government (i.e. removing an obligation of extensive road work by the bidder and allowing one more residential site in the package).

This arrangement however still challenges that only a limited pool of local developers possess the capital capacity, technical readiness, and industry partnerships needed to credibly respond to the Enterprise & Technology Park requirements. This pilot is therefore a deliberate test bed: the Government is using land disposal to push industry oriented urban development, while providing maximum visibility of infrastructural works and certain new facilitative measures such as allowing the offsetting of land premium by surrendering land in the NM to be resumed by the Government, staged payment of land premium and independent land leases for tender sites to show a commitment to bringing private sector expertise into the region’s transformation. Yet, the value realisation hinges on infrastructure delivery, population intake, and formation of an industry ecosystem — i.e. long‑horizon strategies rather than short‑cycle development trades.

On the other hand, the mass-market residential players should partner early with credible industry operators to strengthen the 70% non‑premium envelope for potentially a good bargain of large-scale valuable lands in the evolving new development areas in the Northern Metropolis, with entry land values substantially below core urban districts and more importantly backed by the government policy and uplift potential due to commission of MTR Hung Shui Kiu Station (expected 2030) when the units come to market around the early 2030s.

Developers face a different financial landscape today compared with the last land cycle: borrowing costs remain elevated, construction and labour costs are at record highs, and for luxury projects, the increase of stamp duty for properties above HK$100 million has added a new layer of transactional friction. The implications are clearest in the case of the Stanley (Cape Road) luxury site, which had already been withdrawn in 2023 after all bids failed to reach the Government’s reserved price. In such an environment, it is unlikely that luxury focused tender sites will regain broad participation in the near term, notwithstanding the site’s rare supply characteristics. The contrast between mass market resilience and luxury caution has not been this obvious in years.

These realities underscore why a transparent, quarterly release rhythm is more critical than ever. In cycles where capital planning has become more conservative — especially among mid sized developers. This disciplined cadence helps prevent the kind of supply gaps that could resurface as structural shortages years later; it also signals that the Government is committed to orderly land administration rather than revenue maximisation. The Budget’s framing, which downplays the importance of headline land revenues and re emphasises stable supply as the core objective, reinforces this shift. The approach recognises the volatility of land revenue and instead prioritises long term planning outcomes over short term fiscal gains.

Moreover, the List’s disposal mix makes sense for its risk balancing. The inclusion of Ho Man Tin and Shek Mun sites offers the market two urban, lower beta development opportunities that are likely to attract broad participation once ready. These sites, with mature surroundings and transparent land value benchmarks, help anchor sentiment and offset the inherently higher uncertainty associated with the large-scale new town projects or the long rolled over rural plot. Such diversification is essential to maintaining competitive bidding terrain across economic cycles.

In parallel, the Government’s experience with overly large tender sites — including MTR projects that struggled before being relaunched in more manageable formats — has reinforced an important lesson: scale must match the cycle. Where projects have been right sized (as seen in the MTR Tung Chung East Station Package One revisions), keen participation has recovered. This cycle sensitive pragmatism is reflected again in the 2026/27 programme’s emphasis toward medium scale, better-located, mass-market opportunities.

Taken together, the Government’s strategy and the market’s behaviour are converging on an implicit consensus: the focus this year is not on volume, nor on pushing high risk projects into a hesitant market. Instead, the goal is orderly progression, structural alignment with long term planning priorities such as the Northern Metropolis, and the preservation of a functional, competitive land market. Developers, for their part, are responding accordingly — pursuing mass market opportunities, partnering more selectively on complex industry oriented pilots, and approaching luxury bids with heightened caution. In this sense, the FY2026/27 Land Sale List is less a departure from past practice and more a calibrated version: one designed to match Hong Kong’s current bottomed property cycle while setting the foundations for its next phase of growth.